With all eyes on the consumer, there’s definitely a disconnect between weak consumer confidence and strong same store sales. Here are some stats showing that we need a BIG sequential comp ramp to offset recent Confidence numbers – just as yy compares are getting tough.

As a backdrop, let’s keep in mind the size of the major data points in question -- PCE vs. retail sales vs. chain store sales (SSS)

PCE = $11 trillion – about 72% of our economy

Retail Sales = $3.1 trillion. In other words, only 28% of consumers’ total expenditures take place in a retail store or online.

Chain Store Sales = about $300 billion per year. (That’s Billion – with a ‘B’). These are the data points that come out the first Thursday of each month. They account for only 10% of Retail Sales, and only 2.7% of what actually comes out of consumers’ wallets. And yes, they become less meaningful by the day as the major retailers opt out of reporting numbers.

We’d argue that Consumer Confidence should most closely track Retail Sales – which is 10x the size of the data points we get on SSS day and includes far more relevant categories. PCE is tougher to use as a benchmark, as it also includes housing, medical, and other expenditures that happen regardless of the consumer’s confidence level.

Even though Retail Sales SHOULD be the key number to watch, the fact of the matter is that it’s reported on a 2-month lag. The most real-time measure is consumer confidence, and (albeit incrementally not meaningful to the consumer) chain store sales.

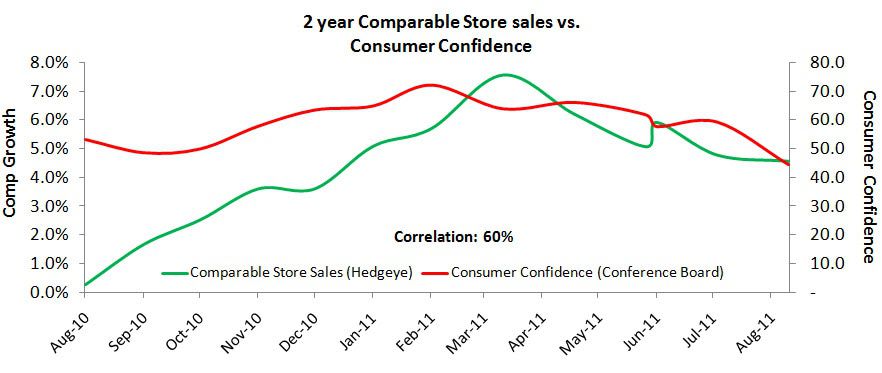

As for some analysis…

1) Over the past year, chain store sales growth has only been about 30% correlated with consumer confidence; 2-year chain store sales have been ~60% correlated with consumer confidence over the past 12-months.

2) BUT, if we lag consumer confidence by a month – which makes mathematical and logical sense, and then compare that to an underlying run-rate for comps (2-year SSS) we get to a correlation closer to 88%.

3) On that lag, if we look at the sales numbers we’d need to see in order to maintain a) the underlying 2-yr sales growth rate and b) the .88 correlation, it would suggest a -8.5% comp decline (i.e. what we should be looking at this month, all else equal). If anything, there are more reasons for the industry to come in on the lower side of ‘all else equal’(storms, power outages on east coast and CA, etc…).