Looking at Greece and the Other Dominoes

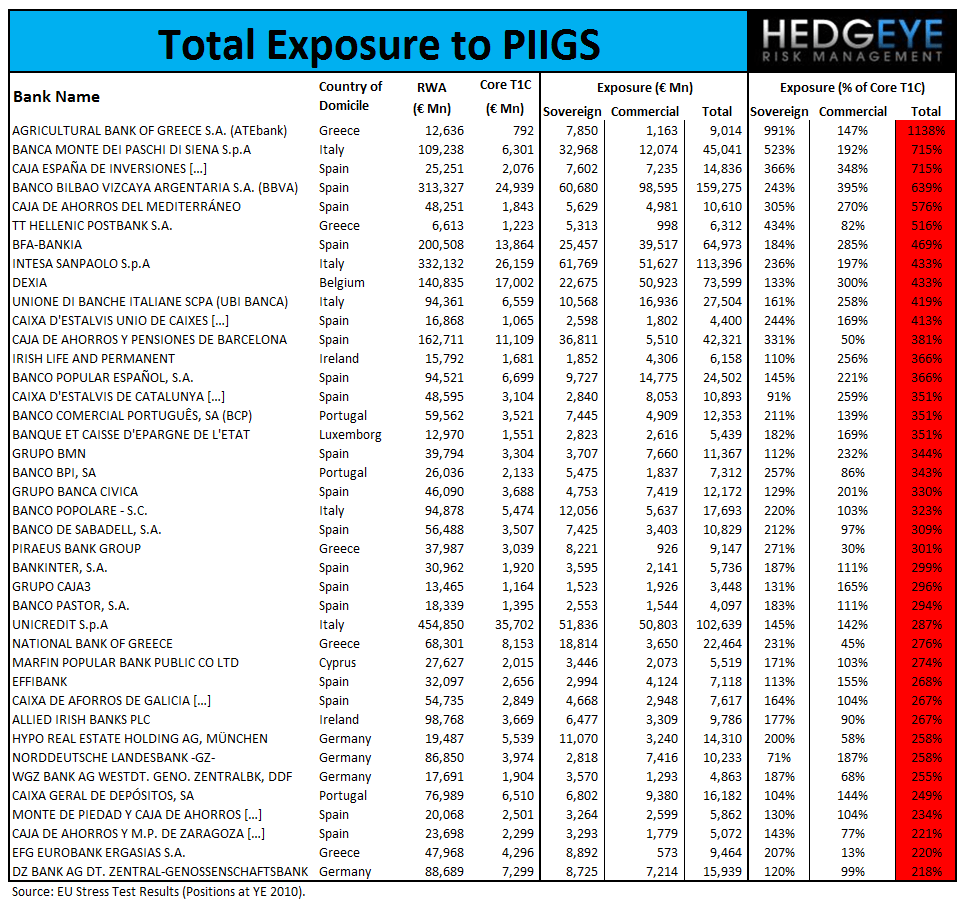

With the market now saying a Greek default is upon us, we're revisiting a post we first published on July 18 of this year called "European Debt: Where the Bodies are Buried". In that post we reverse engineered the EU stress tests and published the precise sovereign holdings and loan exposure by EU bank across each PIIGS country. We broke this out in a series of tables, which we are republishing below. Bear in mind that a limitation here is that we're looking at holdings as of year-end 2010.

By way of example, one area of market concern this morning is French bank downgrade risk. As the table below shows, both Soc Gen and BNP held approximately 10% of their Tier 1 Capital in Greek Sovereign Exposure as of YE2010, while Credit Agricole holds around 1%. Other highly exposed non-Greek EU banks as of YE10 were Banco Comercial Portugues (Portugal: 60 billion euros RWA) with 21% of its capital directly exposed to Greek sovereign debt, Dexia (Belgium: 140 billion euros RWA) with 20% of its capital directly exposed to Greek sovereign debt, and Commerzbank (Germany: 268 billion euros RWA) with 11% of its capital exposed.

Investors can consider these tables a reasonable starting point in assessing interconnected risk across the EU banking landscape.

Summary Conclusions: 13 of the Top 40 EU Banks Hold Over 200% of their Capital in PIIGS Exposure

We find that there are numerous European banks with over 100% of their Core Tier 1 Capital committed to either PIIGS commercial loans or PIIGS sovereign debt holdings. For example, we found that 18 of the 40 largest European banks held 100% or more of their Core Tier 1 Capital in PIIGS sovereign debt or commercial loans. In 14 of these cases, the banks held more than 200% of their Core Tier 1 Capital in PIIGS sovereign debt or commercial loans.

As a general rule we found that the Nordic banks are the least exposed to PIIGS debt, typically holding less than 20% of their Core Tier 1 Capital, putting them at considerably less risk than the group as a whole.

Joshua Steiner, CFA

Allison Kaptur