TODAY’S S&P 500 SET-UP - September 9, 2011

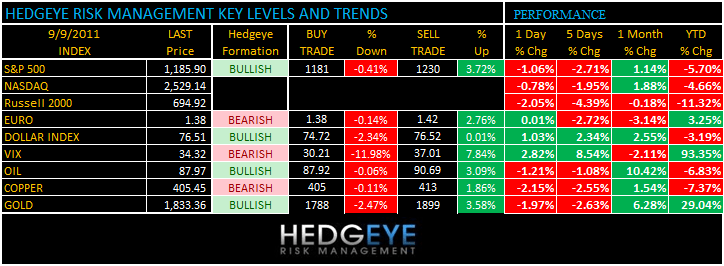

As we look at today’s set up for the S&P 500, the range is 49 points or -0.41% downside to 1181 and 3.72% upside to 1230.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1699 (2420)

- VOLUME: NYSE 946.67 (-0.8%)

- VIX: 34.32 +2.82% YTD PERFORMANCE: +93.35%

- SPX PUT/CALL RATIO: 1.23 from 1.99

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 32.66

- 3-MONTH T-BILL YIELD: 0.0102

- 10-Year: 2.00 from2.05

- YIELD CURVE: 1.81 from 1.84

MACRO DATA POINTS (Bloomberg Estimates):

- 10 a.m.: Wholesale inventories, est. 0.7%, prior 0.6%

- 11:45 a.m.: Fed’s Williams speaks at symposium in SF

- 1 p.m.: Baker Hughes rig count

WHAT TO WATCH:

- G-7 finance ministers and central bankers gather in Marseille, France, to discuss the European sovereign debt crisis and outlook for global growth

- Tropical Storm Nate expected to strengthen to hurricane today as it forces energy cos. to begin evacuating platforms in Gulf of Mexico; final track still in question

- NLRB holds hearings on Boeing 787 plant in South Carolina

- Dish Network may be headed for split with ESPN over increasing rights fees: N.Y. Post

- Amazon.com would drop quest to exempt itself from collecting sales taxes in Calif., state would forfeit ~$200m under pact lawmakers must act on today if it’s to be adopted

- FDA AdCom on safety of osteoporosis drugs

- Senate passed biggest change to U.S. patent law since at least 1952 yesterday, now heads to White House for Obama’s signature

- No IPOs expected to price today

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Oil Drops a Second Day as Rising Dollar Counters Storm Concerns

- Corn, Soy May Open Higher on Shrinking Crops; Wheat Seen Steady

- Soybeans Advance, Reducing Weekly Decline, on Yield Estimates

- Copper Erases Weekly Gain as Slowing Economies May Curb Demand

- Gold Drops in New York as Dollar’s Rise Prompts Investor Sales

- Coffee Falls on Demand Concerns Before Large Crops; Sugar Rises

- Fortress Commodity Fund Said to Beat BlueGold in August

- Wheat Supplies From India May Add to Surplus, Pressure Price

- Refiners in U.S. Most Dependent Ever on Exports: Energy Markets

- Copper May Decline 5.1% in Next Few Weeks: Technical Analysis

- Aluminum Usage in Cars Will Double in Four Years, Novelis Says

- Corn, Soybean Yields Cut on Adverse Weather, Goldman Says

- Libya Said to Ship First Oil From West as Production Resumes

- Africa’s New Friend China Finances $9.3 Billion of Hydropower

- U.S. Soybean, Wheat, Soyoil Exports Fell Last Week, Survey Shows

- Steelmakers Set to Curb Output as Costs Surge: Chart of the Day

- India’s Cotton Exports May Jump 21% Next Year, Group Says

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

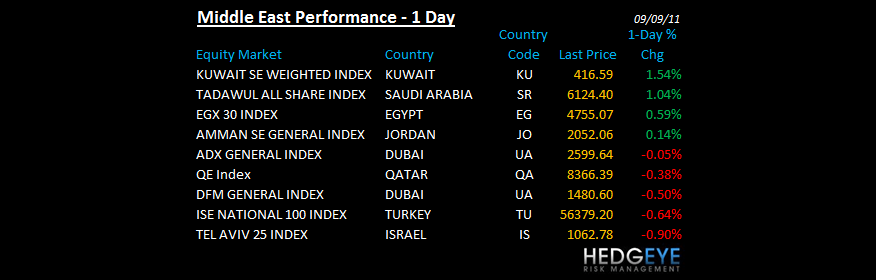

MIDDLE EAST

Howard Penney

Managing Director