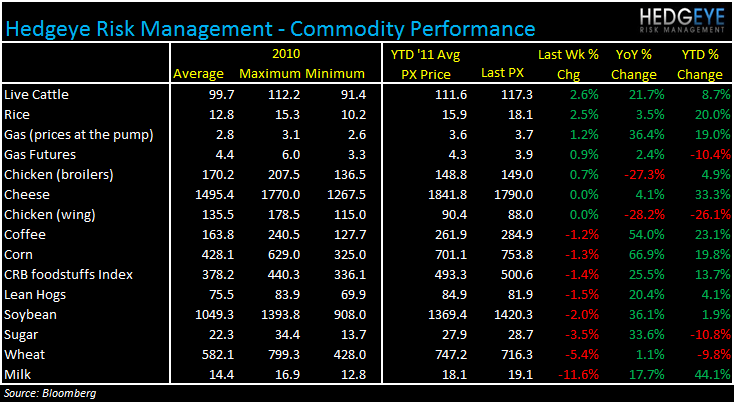

A weekly look at commodity trends pertaining to our space. Over the last week, dollar strength and concerns surrounding economic growth have helped drive overall commodity prices lower.

SUMMARY

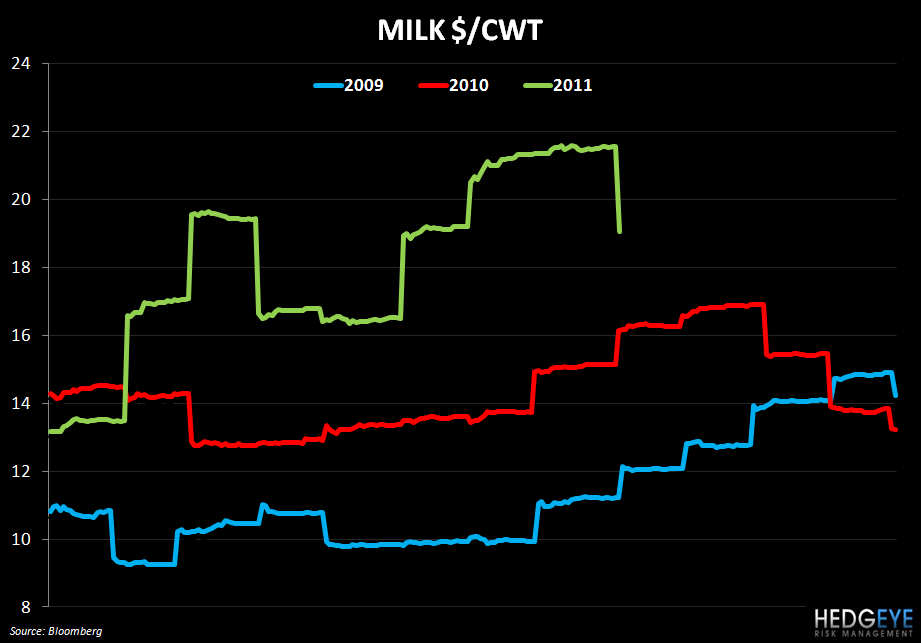

Beef prices led the way over the past week, gaining 2.6% along with rice and chicken in what was a muted week for the gainers. To the downside, Milk led the way with a -12% move and grains, soybeans, sugar, and coffee also declined week-over-week.

DAIRY

Cheese prices stayed flat week-over-week but have declined -17% since August 1st. Prices have been extremely volatile this year but, for companies that have exposure to cheese prices (like DPZ, PZZA, TXRH, YUM and others), the recent leg down in dairy prices is encouraging.

Below is a selection of comments from management teams pertaining to cheese prices from recent earnings calls.

DPZ (7.26.11): “Given higher than originally anticipated cheese prices, we currently expect our overall market basket for 2011 will increase by 4.5% to 6% over 2010 levels. This was up from our previously communicated range of 3% to 5%.”

HEDGEYE: We recently highlighted the fact that DPZ’s last earnings call took place during a trough in cheese prices and we expected a change in tone from the commentary in early May. It remains to be seen if cheese prices will remain above 2010 levels for the remainder of the year but CAKE’s guidance for inflation in 2011 recently became much more realistic, although not a sure thing.

TXHR (5.2.11): “We've also got a lot of flow in the dairy markets, in cheese, so there's other things beyond produce that do move around throughout the year.”

HEDGEYE: In 1Q09, TXRH called out favorable beef and cheese prices as being primary drivers of cost of sales being down 126 bps in the quarter. Cheese was a contributor to a cost of sales increase in 2Q11, as we predicted. For the remainder of the year, barring another (possible) spike in prices, TXRH could see some margin relief from lower dairy costs.

CMG (4.20.11): “As we move into 2011, we're expanding our use of cheese and sour cream made with milk from cows that are raised on open pastures rather than spending much of their time in confinement, as most dairy cattle do.”

HEDGEYE: For CMG, the lower levels of dairy costs, if they persist, will offer some food costs relief on the company’s P&L.

GRAINS

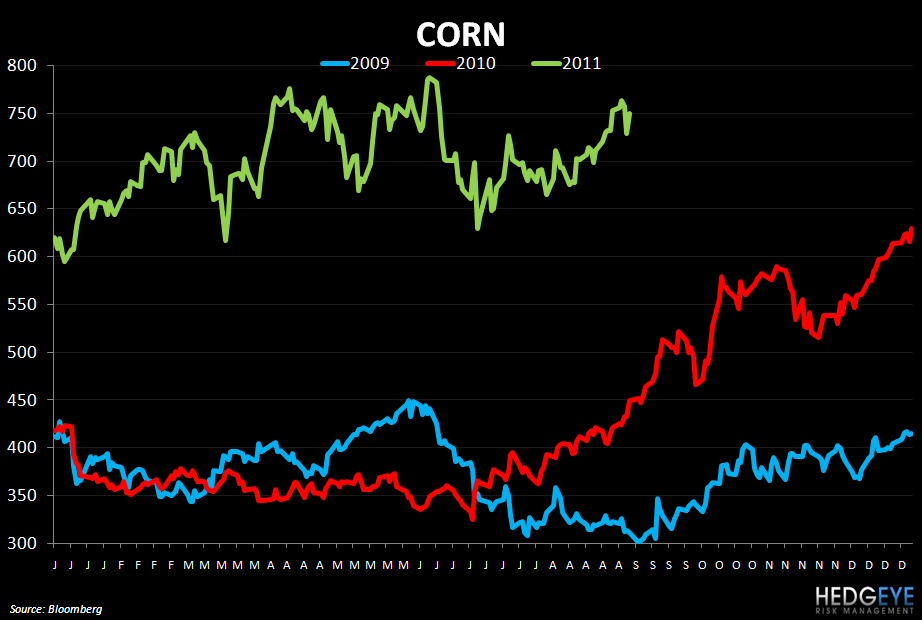

Corn and wheat prices have been moving higher over the past couple of months as adverse weather conditions depress sentiment surrounding the upcoming planting season. Russia increasing its grain exports is offering some relief as crops have been coming in worse-than-expected in the U.S. and Europe. Besides the strength in the dollar, decreased demand as global economic growth concerns stemming from the accelerating European sovereign-debt crisis is also weighing on grain prices.

One interesting article we read today highlighted that Cropcast, a well-known agricultural weather firm, projected U.S. farmers will harvest 4.3% less corn than last year due to poor weather. Cropcast cut its output forecast because it expects many acres planted with corn will not be harvested due to flooding around the Mississippi and Missouri rivers and a severe drought in Texas, said Don Keeney, senior agricultural meteorologist for Cropcast.

Below is a selection of comments from management teams pertaining to grain prices from recent earnings calls.

PNRA (7/27/11): “Just to note on the cost of wheat, in 2011 overall, the per-bushel cost will be about the same as 2010 due to our laddering purchasing strategy.”

“We are going to take price in the fourth quarter. This price will offset dollar for dollar the per-bushel inflation of wheat of approximately $3 a quarter that we're going to see in the fourth quarter of this year and then across next year”

“We do continue to expect significant inflationary pressures in 2012, 4% to 5% food inflation, $10 million of unfavorability on wheat costs, which means that we don't expect operating margin much better than flat to full-year 2011 in 2012.”

HEDGEYE: Wheat costs have come down but it remains unclear whether or not the current easing of grain prices will continue. Weak global demand and a stronger dollar are currently trumping the adverse impact on supply due to weather and fires in the U.S. Slowing demand may also mean lower sales for PNRA, so it remains to be seen if margins improve from this effect, even if high wheat costs come down.

DPZ (7/26/11): “We're fairly locked in on our chicken, locked in on our wheat into – partway into next year.”

PZZA (8/4/11): “We're actually covered through Q1 from a contract standpoint. So from a supply chain disruption or even significant price impact we don't anticipate anything between now and the end of the year.”

LIVE CATTLE

Beef prices gained by 2.6% week-over-week as unfavorable conditions persist for cattle farmers. The USDA has rated 90% of the pasture conditions in the Southern Great Plains as very poor. To make matters worse, as the website CattleNetwork states, most livestock water sources are drying up or have reached a point where water quality is a major concern. Beef producers are now being faced with a difficult proposition: liquidate the herd or maintain the herd until pastures are – hopefully – renewed in April or May of 2012 and take on the implied cost of feeding the herd with feed prices far higher than a year ago. The following link walks the reader through the logic of the decision facing producers. [herd liquidation story ]

Below is a selection of comments from management teams pertaining to beef prices from recent earnings calls.

RRGB (8/11/11): “We're still buying ground beef on the spot market… If you recall, we said 5% to 6% commodity inflation on the last call and we dropped that to 5 to 5.5. Again, that's mainly ground beef driving that.”

HEDGEYE: Live cattle prices are up 22% YoY and, we believe, will continue to be a negative for RRGB’s P&L going forward.

WEN (8/11/11): “That's one of the reasons why as we've talked about our margin guidance, we do not expect to see much relief on beef cost this year.”

Howard Penney

Managing Director

Rory Green

Analyst