Notable macro data points, news items, and price action pertaining to the restaurant space.

MACRO

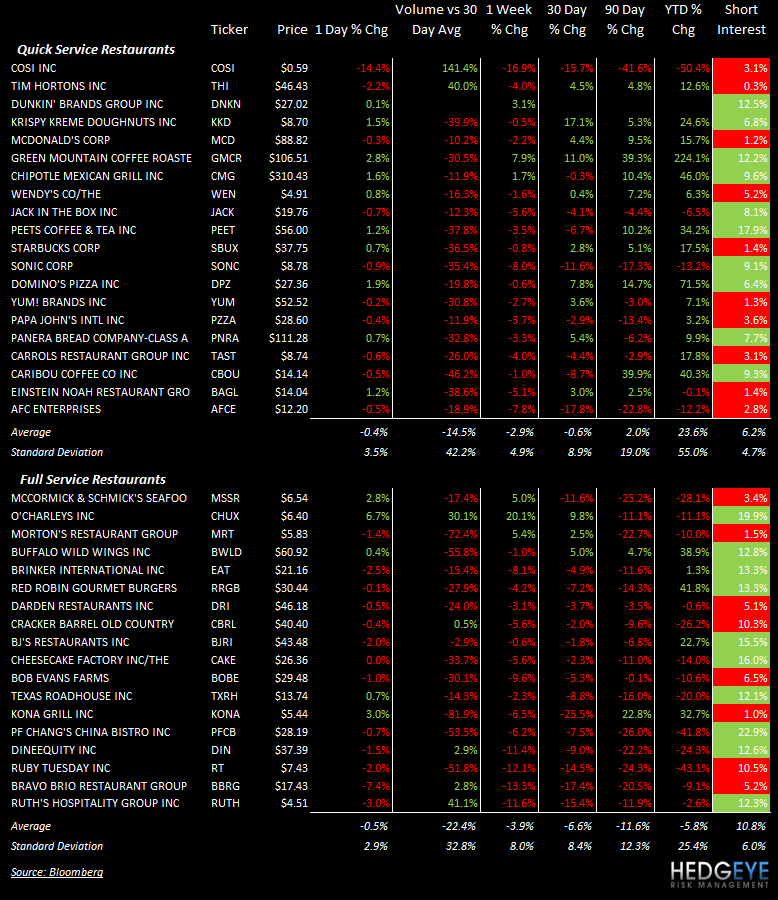

Subsectors

Food Retail is has outperformed over the last day, week, and two weeks as Food Processors continue to lag peer food, beverage, and restaurant spaces.

QUICK SERVICE

- MCD Canada is to spend $1 billion to renovate all of its locations in Canada in effort to take market share. Testing has already proven a success with traffic in reimaged restaurants growing close to double-digits.

- SONC was cut to “Market Perform” at William Blair.

- CMG’s second London location is now open on Baker Street in the Marylebone district.

CASUAL DINING

- DRI preannounced 1QFY12 EPS at $0.78 versus $0.87 consensus but reaffirmed FY12 EPS guidance of 12-15% EPS growth. Sales trends were disappointing at Olive Garden in June, July and August (prelim. August number). See our post from this morning for more details.

- DRI was cut to “Outperform” from Raymond James versus “Strong Buy”. The price target was cut to $52 from $62.

Howard Penney

Managing Director

Rory Green

Analyst