CORRECTION: The $85mm value of this morning’s deal was net of debt disposition, not gross that we previously implied. The difference is not immaterial though it does not change our call on LIZ, which is all about driving RNOA sharply higher as it sheds underperforming assets while driving EBIT higher and delevering along the way.

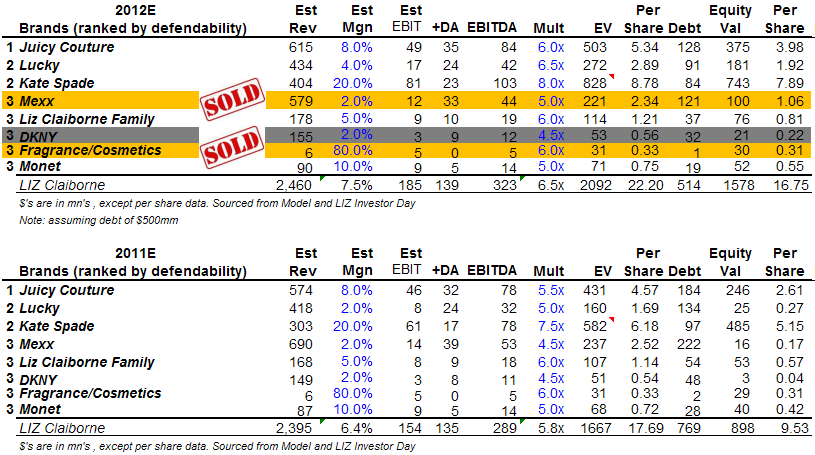

LIZ officially announced the sale of its Mexx business this morning removing one major drag and improving another other – its balance sheet. According to the terms of the deal, the company will receive $85mm in total cash consideration consisting of $25mm of cash in hand and $60mm of debt that will be assumed by the newly formed JV between The Gores Group (81.25% owner) and Liz (18.75%). The deal values Mexx’s ~$700mm in revenue at $105mm and marks the second asset sale in the past 30-days.

The terms are below what was rumored by the press last month, but keep in mind a few things… 1) while the market was melting down this deal was widely rumored to be falling apart, 2) The stock was off 37% during this period, and 3) at the same time, its net debt improved by almost 20% . Most importantly, the stock price is at the same level today – and the Enterprise Value 10% lower – than when the biggest pushback we got on our call was “this Board is inactive, management stinks, the balance sheet is too levered, and this company could go bankrupt.’ Anyone want to make sense of that for me?

Between this deal and the fragrance business they sold last month, the company is getting ~$83mm in cash and a $60mm reduction in debt providing added flexibility with which to manage leverage during Q3 before paying down a large portion of their debt in Q4. It’s also worth noting that this would get the company within ~$50mm of its goal of $578mm by year-end.

Looking out to next year (perhaps sooner), we suspect the company is likely to execute additional sales within its Partnered Brands business that could amount to another $100-$200mm that could be put towards deleveraging the business further.

So what’s left after these sales? We have the Partnered Brands business that we expect to generate nearly $20mm in EBIT next year and the three remaining Direct Brands (Kate, Juicy, and Lucky) that we expect to generate at least $80mm. With aggressive deleveraging underway, we are modeling approximately ~$15 in interest expense reduction generating earnings north of $0.45 next year assuming conservative operating improvement among the Direct Brands. We don’t have to drum up heroic assumptions to get earnings over $0.75.

With the company actively unlocking value through asset sales, it’s worth considering our sum-of-the-parts analysis below, which suggests a value of $12-$14 taking into account recent sales and a 10% breakup discount. That’s a double from current prices.

We think investors will get at least that on LIZ. This remains our favorite small-cap TAIL idea.

Casey Flavin

Director