This note was originally published at 8am on August 30, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Feeling good about a judgment is a prerequisite to acting upon it.”

-Dan Gardner (Future Babble, 2010)

I moved the Hedgeye Portfolio to net short (more shorts than longs) for the first time since June 23rd yesterday.

Did I feel good about it? Did I feel as good as I felt about running net short in June of 2011? How good did I feel moving to one of my most net long positions (more longs than shorts) on August 8th, 2011?

The answers to these questions are uncertain. I never feel good about any position until it’s working. And there is usually a huge difference between what I am feeling versus what I am actually doing with my longs and shorts.

“Confirmation bias” is a term that was coined by cognitive psychologist and Master Chess player, Peter Wason, in the 1960s. Per Wikipedia, the simple definition of confirmation bias is the “tendency for people to favor information that confirms their preconceptions or hypotheses regardless of whether the information is true.”

Confirmation bias, as Dan Gardner astutely calls out on page 84 of “Future Babble – Why Expert Predictions Fail and Why We Believe Them Anyway”, “is as simple as it is dangerous.” As Global Macro Risk Managers, we need to be thinking long and hard about that.

“In Peter Wason’s seminal experiment, he provided people with feedback so that when they sought out confirming evidence and came to a false conclusion, they were told clearly and unmistakably, that it was incorrect. Then they were asked to try again. Incredibly, half of those who had been told their belief was false continued to search for confirmation that it was right.” (Future Babble, page 85)

Can you imagine if Wason’s sample study was today’s short-term performance chasing hedge fund community? Never mind half – that number would be a lot higher than 50%. After all, we hedge fund people were born on this good earth to be able to judge sales, margins, and “valuations” light-years beyond our contemporaries who are still caged up in the Bronx Zoo.

Back to the Global Macro Grind…

While I was right in my call for a “Short Covering Opportunity” (time stamped 10:47AM August 8th, 2011) in early August, I was wrong last week in suggesting that the SP500 could breakdown to lower-YTD-lows.

Being wrong happens. Most people just don’t like to admit it does. The key in this profession is being right a lot more than you are wrong. And not being really wrong when you aren’t right.

When I decided to move the Hedgeye Portfolio to net short yesterday, it was a conscious decision based on my multi-factor, multi-duration, Global Macro Model – not solely on what the SP500 was doing.

That’s not to say what the SP500 is doing doesn’t matter. What it has been doing does too (SP500 returns):

- DOWN -22.7% from its October 2007 top

- DOWN -11.2% from its lower-long-term high established in April 2011

- UP +8.1% from its higher-immediate-term low established in August 2011

Now a Perma-Bull will quickly snort … but but but, “we’re up huge from the 2009 low.” And we all get where that is coming from – what the bull means is that the US stock market is up +78% from the 2009 low. His client’s money isn’t.

Math doesn’t uphold the principles of storytelling or confirmation bias:

- The SP500 lost 57% from October 2007 to March of 2009

- In order to “break even” on that loss, your buy-the-dip bull would need to be up +131% off the bottom

- That, of course, assumes he nailed every move along the way (for 3 years)

So when the manic media is hammering you with “Greek stocks are having their best day ever” yesterday (they did on a percentage basis), remember that on Friday Greek stocks had crashed (down -48% since February 2011) and they’d need to “rally” +92% “off the lows” to get you back to break even versus only 6 months ago.

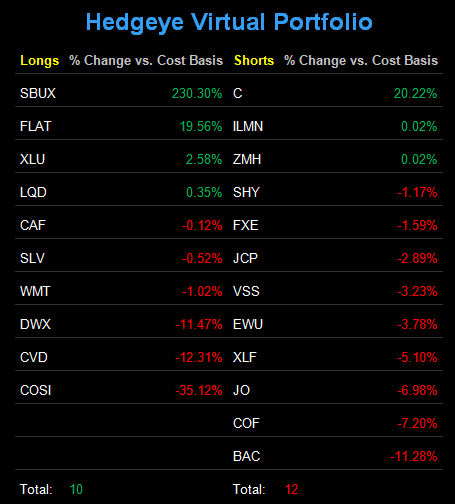

Or how about Bank of America? How good am I “feeling” about shorting that stock again yesterday in the Hedgeye Portfolio?

- Early September 2010 when we were shorting BAC, the stock was at $13.21

- By August 23, 2011, BAC had lost 52% of its “value” in less than a year

- BAC needs to rally +110% “off the lows” to get back to a 1 year break even return

I didn’t feel good about shorting BAC yesterday. I felt as uncertain as I should feel when a short position is -11.28% against me. While our Financials Managing Director, Josh Steiner, and I have shorted this stock 10x since 2010 (and been right 10x), that and a case of Molson Canadians will maybe make us prolific horseshoe players down at the lake tonight – nothing more.

If I was being paid what I used to be overpaid working at hedge funds and I said that in a morning meeting, everyone who wanted me to fail would be whispering “uh, it doesn’t sound like Keith has conviction anymore does it”…

That’s Wall Street. They want everyone to be “Feeling Good” about their “best ideas”, all of the time.

My immediate-term TRADE ranges of support and resistance for Gold, Oil, and the SP500 are now $1733-1817, $85.03-88.62, and 1163-1219, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer