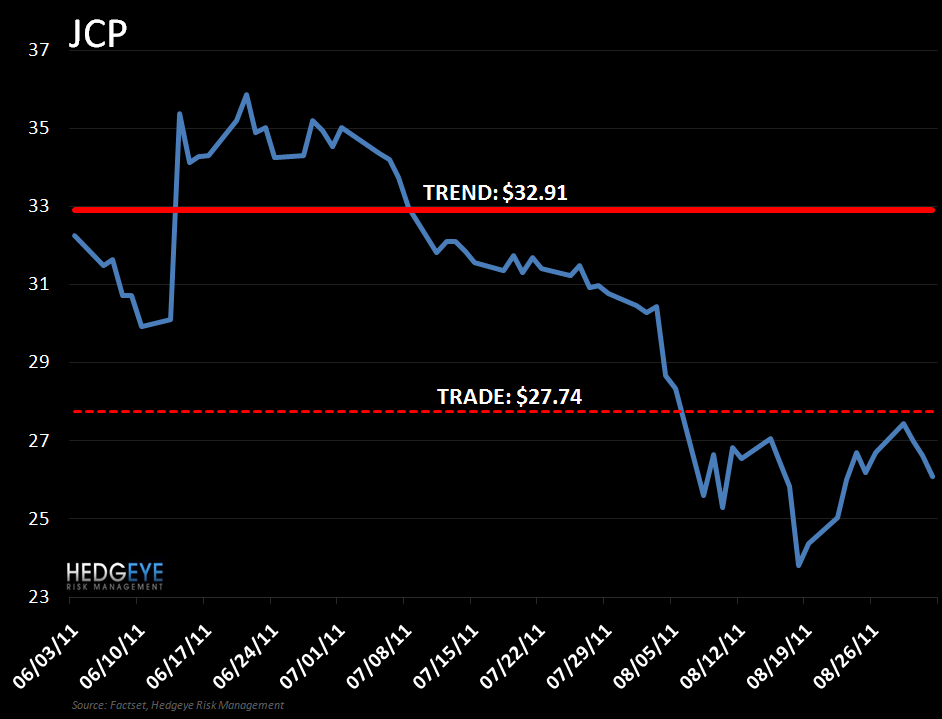

Keith is booking another gain covering JCP in the Hedgeye Virtual Portfolio with the stock immediate-term TRADE oversold according to his model. We remain bearish on the stock over the intermediate-term.

While still early in the quarter, August sales came in very light this morning -1.9% (vs. +1.7%E) supporting our below consensus numbers. The Street is currently expecting flat sales in the 2H on LSD comps. We’re modeling sales down -1% and -3% on comps of +1% and -1% in Q3 and Q4 respectively.

Keep in mind, the company had several new introductions last year in Q3 (LIZ excl, Mango, Modern Bride) that they have to lap in addition to catalog sales rolling off. We’re expecting sales from existing stores to be down -$180mm in addition to the negative drag from the catalog business to the tune of $200-$260mm coming out in the 2H. With pressure on growth from existing stores coupled with catalog sales coming off, JCP will be significantly challenged to meet the Street’s sales expectations over the intermediate-term.

As for the headline regarding the company selling outlet stores that just hit the tape - it's old news and inconsequential to the bigger call here.

At $1.60 for the year, we remain 10% below consensus and bearish on the stock over the intermediate-term.

For more info on our thesis, see our Black Book, “JCP: What Ackmanists Are Missing.”