Positions in Europe: Short UK (EWU); Covered EUR-USD (FXE) on 8/31 in the Hedgeye Portfolio

Below we call-out four charts of the day: European Manufacturing PMI; Eurozone Confidence; Italian/German government yield spread; and the CHF vs EUR and USD.

European Manufacturing PMI Sinks

Of the countries reporting Manufacturing PMI, there’s a clear downturn in the August numbers, a trend we’ve been following for the last six months. 8 of the 15 countries recorded figures below 50, which indicates contraction (see chart below). And short of the Czech Republic, Norway, and Denmark, the remaining countries are dancing on the 50 line. We’re convinced Eastern Europe’s growth outlook can’t improve before the core of Europe improves (due to heavy trade reliance), and we see the core dragged down by sovereign debt leverage of the periphery, banking risk, and slowing growth in the US over the intermediate to longer term durations.

Eurozone Confidence Crumbles

It follows that given sovereign debt contagion across the region confidence will erode. We continue to highlight the threat of a French credit rating downgrade, which we’ve monitored via rising CDS spreads (up +100bps since a low in April), for its impact on the EFSF. Confidence has trended down since February of this year. We see plenty of downside room to run from here with significant white space (= uncertainty) between now and the late September/early October decision on the terms of the EFSF, which don't include increasing its size from €750B. We think the facility needs to be expanded to at least €2T, a large order given Germany would back the lion’s share of it.

Bad Boy Berlusconi

Italy and Spain are two countries in Europe we’re closely watching because 1.) Their economies are far larger than Greece, Ireland and Portugal and present must greater risks from a sovereign and banking perspective, 2.) Should either country need “bailout” assistance the EFSF is underfunded and there’s no indication Trichet wants the ECB to directly take on "more" region-wide balance sheet exposure.

German yields have come in notably ytd (-79bps), and therefore the country still remains the region’s beacon of stability, while its equity market has been crushed (DAX down -19% in August alone). Given that Merkel is pumping up against two more State elections (in September) and floundering confidence even among her party, it’s far from a foregone conclusion that Germany will sign any and all blank checks to bailout or support its neighbors. Frankly, we’re worried that the once perceived stronger peer nations (of France and Italy) may be in no shape to contribute to bailing out the region if tipping points are achieved in those countries.

One kink in the chain came on Tuesday when Berlusconi announced that the country’s €45 Billion austerity package will be pruned. The new version removes the Solidarity tax , which placed an additional 5% tax on annual incomes above €90K, and the original proposal to cut €9B in funding to regional and local governments was trimmed by €2B. At a time when fat (debt) is expected to be reduced, pruning the austerity package heightens the risk of investor sentiment turning negative.

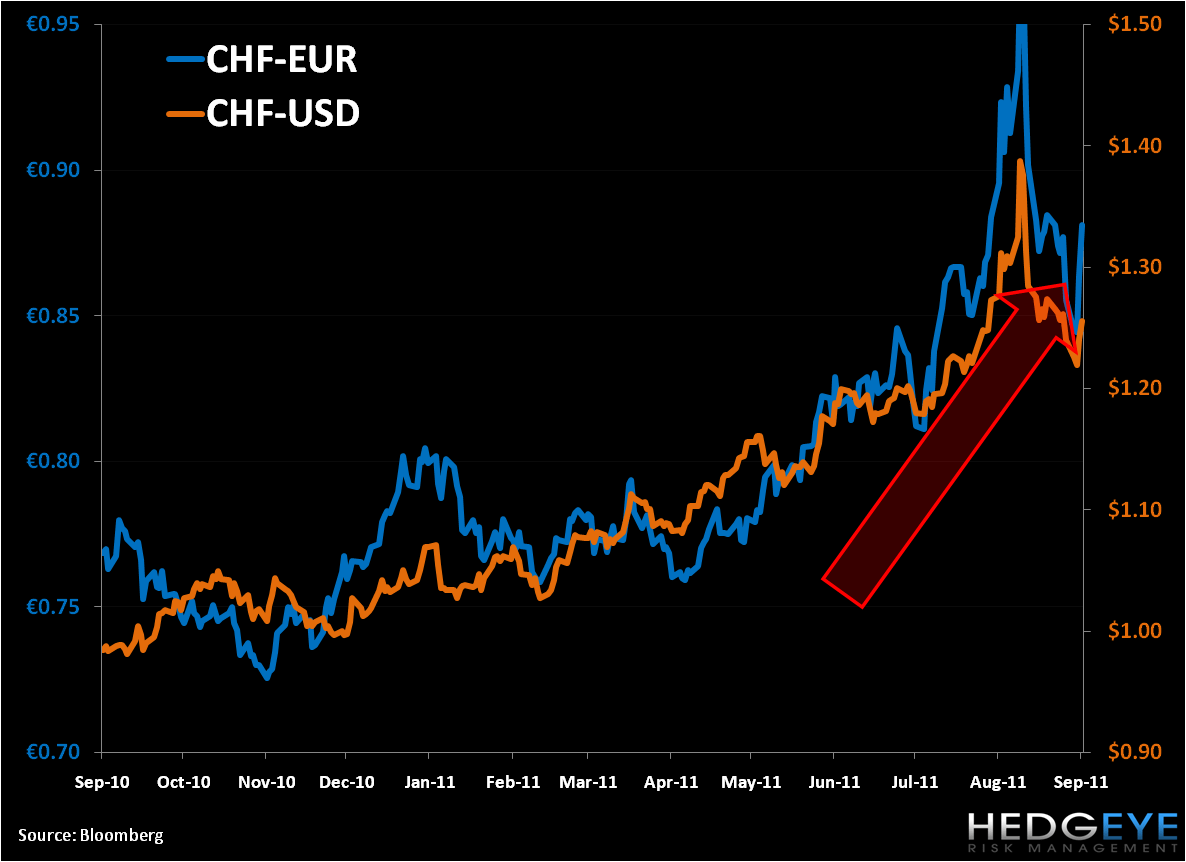

Swissy Back on the Juice

With the Swiss National Bank (SNB) refraining from announcing further steps to weaken the CHF versus major currencies and today's announcement by the government of an 870 million Franc ($1.1 Billion) economic stimulus package to support tourism and exports (still to be approved by parliament in September), there looks to be more room to run in the CHF vs the EUR and USD from here, especially as there’s no indication Europe has command of the run-away sovereign debt contagion threats that have plagued the region for the last 18 months.

It’s worth noting that there’s already much domestic consternation on the government’s stimulus package, which includes 500M CHF to protect jobs in all industry sectors, with most cash being used to extend the exiting shortened working hours scheme and 100M going to a fund that extends emergency assistance to the hotel industry. Push-back includes the ultimate size of the package, off the original 2B CHF proposed in August, and the government’s ability to properly allocate funds, meaning some enterprises will benefit while others will not receive assistance.

All in, we think the flight to the safety trade remains intact.

Matthew Hedrick

Senior Analyst