TODAY’S S&P 500 SET-UP - September 1, 2011

After global equities got pulverized in August and we got another low-volume month end rally out of the way, we’re back to Global Macro fundamentals driving markets this morning.

GLOBAL GROWTH – what’s scariest about Germany’s crash is that its economy is in much better shape than most of the majors (including the USA); while it’s nice to see everyone in the US claiming to have nailed calling all bottoms in August, that doesn’t change the fact that Q2 US GDP was revised down another -31% in the last month to 0.98% (Germany’s Q2 was +2.8%)

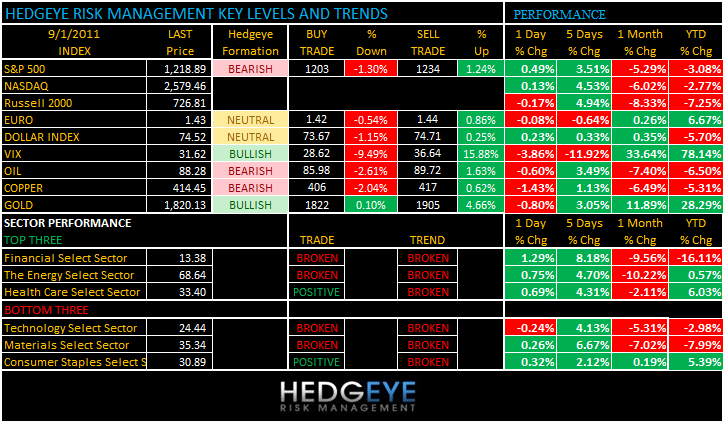

As we look at today’s set up for the S&P 500, the range is 31 points or -1.30% downside to 1203 and 1.24% upside to 1234.

US Equities should be fine as long as 1203 holds (SP500). If/when it doesn’t, I guess they’ll call that risk “on” (its always on) … until the media begs for the next Keynesian experiment (Obama delayed his bag of goodies to next Thursday).

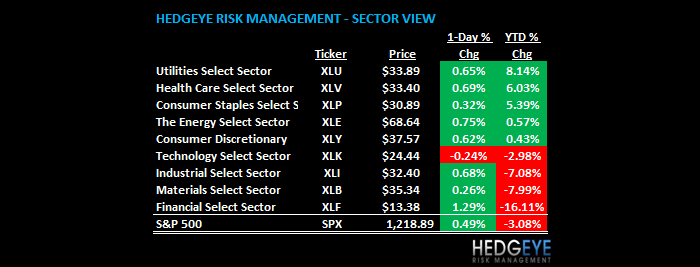

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +901 (+139)

- VOLUME: NYSE 1265.13 (+24.13%)

- VIX: 31.62 -3.86% YTD PERFORMANCE: +78.14%

- SPX PUT/CALL RATIO: 1.40 from 1.84 +23.60%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 31.71

- 3-MONTH T-BILL YIELD: 0.02% +0.01%

- 10-Year: 2.22 from 2.19

- YIELD CURVE: 2.03 from 1.99

MACRO DATA POINTS (Bloomberg Estimates):

- U.S. auto sales may have failed to rebound in August, running at a 12.1m rate, analysts est., down from 12.5m rate in 1H 2011

- August retail sales were likely curtailed after Hurricane Irene pushed back-to-school purchases into September. Retail Metrics index est. up 5% vs 3.6% Y/y

- President Obama agreed to move his speech on economy, jobs to Sept. 8 after House Speaker Boehner protested; note NFL season opener at 8:30 p.m. that day

- Competitors will not unequivocally benefit if Justice prevents AT&T's takeover of T-Mobile USA - WSJ

WHAT TO WATCH:

- 8:30 a.m.: Net export sales, commods

- 8:30 a.m.: Jobless claims, est. 410k, prior 417k

- 9:45 a.m.: Bloomberg consumer comfort, prior (-47.0)

- 10 a.m.: Construction spending, est. 0.2%, prior 0.2%

- 10 a.m.: ISM Manufacturing, est. 48.5, est. 50.9

- 10:30 a.m.: EIA Natural Gas

- Noon: Fed’s Duke speaks at Fed conference in Washington

COMMODITY/GROWTH EXPECTATION

COPPER – after Charlie Evans vowed to debauch the US Dollar, most things inflation ripped for a few days, including Copper – but the ole Doctor failed at its TREND line (4.21/lb) this morn and leads commodities on the downside (-1.4%).

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Silver Poised for ‘Golden Cross’ Rise to $50: Technical Analysis

- Baltic Container Jump Dulls Hamburg’s Euro Pain: Freight Markets

- Copper Drops for First Day in Seven on China Growth Concern

- Gold Drops for Second Day as Equities Rally Amid Fed Speculation

- Glencore Proposes $1.2 Billion Takeover of Optimum Coal

- Oil Advances on Manufacturing Reports; Cushing Supplies Decline

- Carnivores Will Choose Cheap Pork Over Beef: Chart of the Day

- Barclays Declines to Comment on Report of Warehouse Purchase

- Cheap Gas Joins EPA to Prompt Switch From Coal: Energy Markets

- Aluminum Fee to Japan Cut as Slowing Recovery Curbs Demand

- Crude Declines in New York on Signs of Slowing Recovery in U.S.

- Corn, Wheat Drop on Speculation Demand for U.S. Crops May Slow

- U.S. Mint American Eagle Gold Coin Sales Are Most Since January

- OPEC Output Climbs to Highest Level Since 2008, Survey Shows

- China Appeals WTO Ruling on Raw Material Export Controls

- Joy Global Sees ‘Strong’ Metals, Coal Demand Led by China, India

CURRENCIES

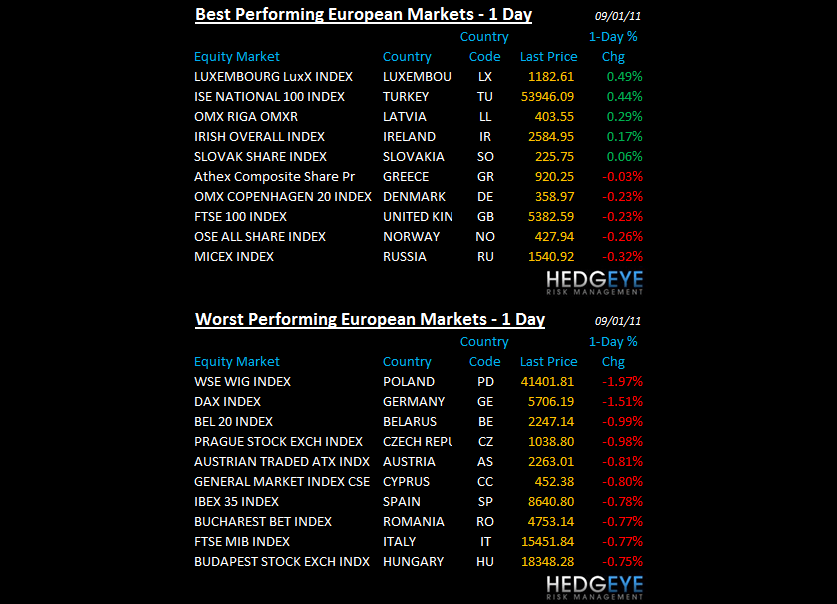

EUROPEAN MARKETS

- EUROPE: just a bloody mess; Germany leads to the downside this morn, down -2% (down -19% in AUG) and down -24.7% since May as PMI data falls

- GREECE: which the manic media was celebrating as rescue me 4 days ago has since dropped 11% in a straight line - long live the Fiat Fools

- EuroZone Aug final Manufacturing PMI 49.0 vs preliminary 49.7 and prior 50.4

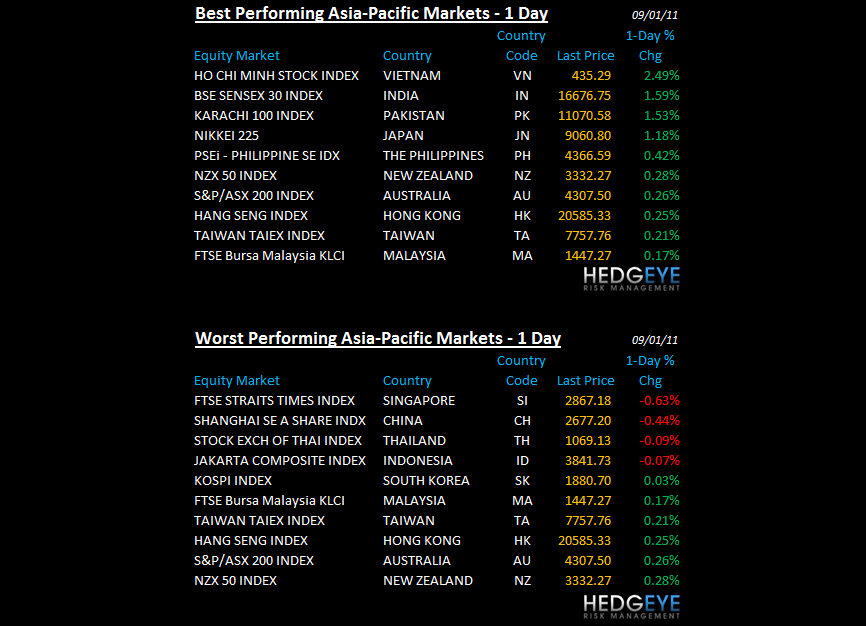

ASIAN MARKETS

- ASIA: mixed again overnight with China down -0.44% and Philippines up +0.42%; Korea's KOSPI remains bearish/broken as Tech orders.. NVLS told us this last night.

MIDDLE EAST

Howard Penney

Managing Director