Overall direct play slowing. So much for eliminating the middle man.

Hidden in the explosive growth in VIP and Mass revenues, direct VIP play growth has been slowing. Even the direct play king - Sands China - realizes it. Junkets aren't going away. In fact, they are growing in power. Junket VIP remains the fastest growing Macau revenue source. We've put together the data and here are some of our observations:

- Direct play growth has slowed down considerably in the 1H of 2011, growing 23% YoY compared to junket RC growing 51% over the same period.

- In 1Q11, direct play grew 24% YoY compared to junket RC growth of 55%. In 2Q11, direct RC grew 22% YoY vs. junket RC growth of 48% over the same period in the prior year

- LVS direct play volume growth went negative in 2Q11, falling 8% YoY. 1Q 2011 showed 8% growth while 2010 grew 93% YoY. LVS has made it clear that they will be making a big push with the junkets in 2012 finally putting a nail in the coffin of their strategy to eliminate the junket middle man.

- MGM also experienced a marked deceleration in direct play growth with 1H11 growing only 4% YoY compared to 32% in 2010 and 114% in 2009. This is no surprise since Mr. Kwong’s strategy was to grow the junket business which has contributed to the strong growth at the property since he joined last year.

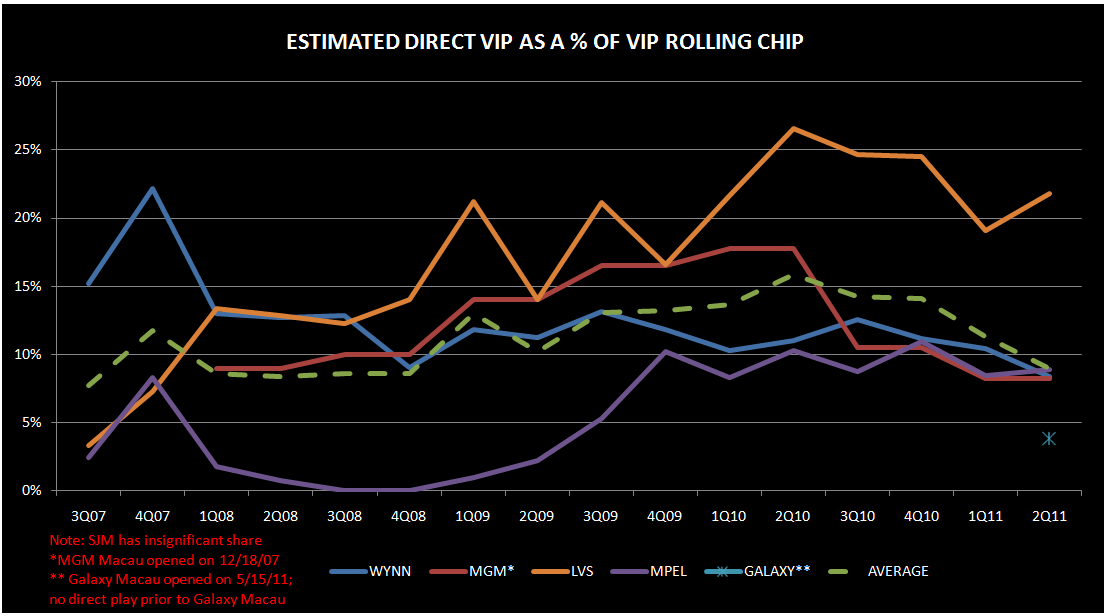

- As the chart below shows, direct play as a % of VIP RC for the five operators fell to 10% in 1H11 compared to 15% in 2010 and 12.5% in 2009

- In 2Q11, every operator experienced a decline of direct play as a % of total VIP RC

- MGM direct play % dropped 10% in 1H10 to just 8.2% from 17.8% in 1H10

- LVS’s direct play % dropped 6% in 2Q11 to 22% from an all-time high of 27% in 2Q10

- Wynn’s direct play % dropped 3% in 2Q11 to just 8.4% - an all-time low for the property

- MPEL’s direct play dropped 1% in 2Q11 to 9% from 10% in 2Q10

- In 2Q 2011, Galaxy Macau’s direct play as a % of VIP RC was 3.8%.