Coffee prices led the way over the last week, gaining 4.5% along with Soybeans, Wings, Rice and Corn which all gained roughly 4% over the same period. Cheese prices gained week-over-week but have declined rapidly from the elevated prices seen for most of the year and are now only marginally above the 2010 peak. Gas prices gained week-over-week as demand picked up, per the Mastercard data, ahead of Hurricane Irene hitting the East Coast.

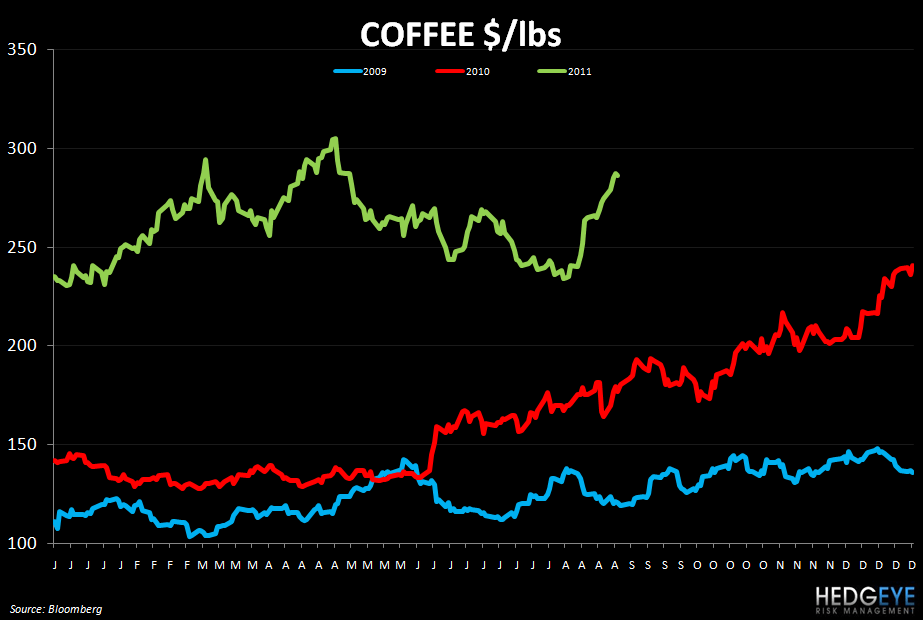

Coffee

Coffee prices gained 4.5% week-over-week, reaching a three-month high in the process, as concerns mounted that global production will fall short of demand. Inventories of Arabica coffee monitored by ICE Futures U.S. have fallen 4.4% this month and 27% in the past year, according to exchange data cited by Bloomberg. Coffee has broken the downward trend that was prevailing for May, June, and July with a strong move to the upside. Prices are now only 6.6% below the YTD high.

Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls.

PEET (8/2/11): “As we indicated, in our first quarter call, we had to buy a small amount of our calendar 2011 coffee beans at significantly higher prices and this coffee will roll into our P&L during the third and fourth quarter.”

“Higher priced coffee resulted in gross margins this quarter being 290 basis points below prior year. In our first quarter conference call, we indicated that in addition to the overall higher price coffee market, we had to buy a small amount of coffee this year at significantly higher prices. And as a result, we expected our coffee cost to be 40% higher in fiscal 2011.”

HEDGEYE: Peet’s is a company with a very competent management team that manages coffee costs extremely well. Its higher-end, loyal customer base makes the price elasticity of demand more inelastic than for other coffee concepts’ products.

SBUX (7/28/11): “As I mentioned earlier, are absolutely a headwind for us in the full business and that's most acutely impactful on margins in CPG as it's a much more coffee intensive cost structure, as you know. I can tell you that the decline as I spoke about it earlier from about 30% operating margin in CPG this year down to the target 25% next year is really all explained by commodities. Absent commodity inflation we'd be at or improving our margin in the coming year.”

“As we had anticipated, in recent weeks, coffee prices have retreated significantly from a high of more than $3 per pound just a couple of months ago to levels now near $2.40 per pound. As prices have been falling we continue locking up our needs for fiscal '12 and now have virtually the full year price protected.”

HEDGEYE: Starbucks is aligning itself with the right partners to gain more control of its coffee costs to provide investors with more certainty going forward and to protect its margins as global coffee demand continues to rise.

GMCR (7/27/2011): “However, what we've said is that should coffee prices or other material costs spike, we will certainly consider price increases as necessary. We certainly hope that we do not have to cover one again next year. But our objective long-term is attempting to maintain our gross margin as we would see input costs come along.”

HEDGEYE: GMCR hedges out 6-9 months in advance. Without a rising dollar and some stronger supply growth to counteract growing global demand, we expect sustained elevated prices.

Cheese

Cheese prices gained 0.6% week-over-week but have declined -17% since the end of July. Sustained higher corn prices should provide some support but prices have been extremely volatile this year.

Below is a selection of comments from management teams pertaining to cheese prices from recent earnings calls.

DPZ (7.26.11): “Given higher than originally anticipated cheese prices, we currently expect our overall market basket for 2011 will increase by 4.5% to 6% over 2010 levels. This was up from our previously communicated range of 3% to 5%.”

HEDGEYE: We recently highlighted the fact that DPZ’s last earnings call took place during a trough in cheese prices and we expected a change in tone from the commentary in early May. It remains to be seen if cheese prices will remain above 2010 levels for the remainder of the year but CAKE’s guidance for inflation in 2011 has suddenly become much more realistic, although not a sure thing.

TXHR (5.2.11): “We've also got a lot of flow in the dairy markets, in cheese, so there's other things beyond produce that do move around throughout the year.”

HEDGEYE: In 1Q09, TXRH called out favorable beef and cheese prices as being primary drivers of cost of sales being down 126 bps in the quarter. Cheese was a contributor to a cost of sales increase in 2Q11, as we predicted.

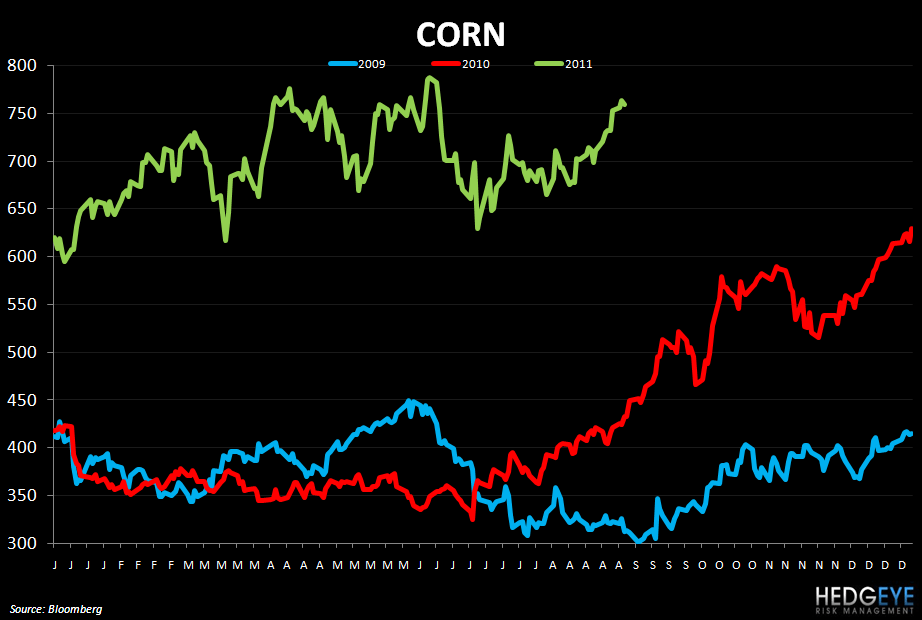

Corn

Corn prices have been moving higher for the past two months as adverse weather conditions have weighed on sentiment for the planting season after what was a poor growing season. Russia is increasing its grain exports as crop damage in the U.S. and Europe impacts supply. U.S. corn and soybeans ranked by the USDA as "good" or "excellent" fell to 54% and 57% respectively last week, down from 57% and 59% in the prior week.

Howard Penney

Managing Director

Rory Green

Analyst