The data is in.

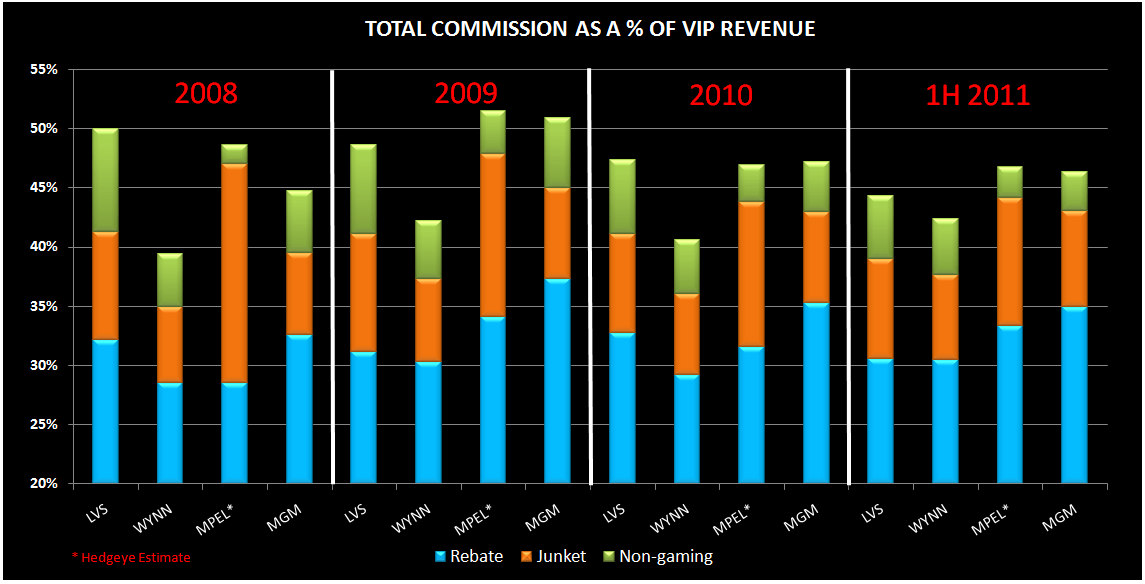

Despite the rhetoric, total commissions have not been rising in Macau. Maybe they will if LVS turns aggressive next year (see our 08/29/11 note “LVS: SHOWING AGGRESSION”), but overall commission rates were down in 1H of 2011 both on a percentage of revenue and rolling chip basis. The following chart shows the junket commission trends. Note that hold percentage was below normal in 2009 which caused the spike in the blue line in that year since the junkets structured on a percentage of rolling chip still get paid the same amount regardless of hold.

The charts below show the composition, by company, of all-in commissions between the straight junket commission, the rebate that goes back to the player, and non-gaming giveaways. The first analyzes the dynamics on a revenue share basis, the second as a percentage of rolling chip. Two main takeaways: Wynn remains the least aggressive – no surprise here – and higher commissions have not been the driver of the strong growth we’ve seen at City of Dreams.

Here are our observations:

- Wynn maintained the most profitable VIP business on the Street by the least to acquire it

- Rebate rate of 85bps of RC or 30.5% of win in 1H11 (88bps/29.3% in 2010)

- Junket commission of 20bps of RC or 7.1% of win in 1H11 (20bps/6.8% in 2010)

- All-in rate including comps of 118bps of RC or 42.35% in 1H11 (122bps/40.6% in 2010)

- MPEL and MGM were tied in 1H11 for paying the most for their VIP business. MGM had the highest on a RC basis, while MPEL got the top prize on a % of win basis.

- MGM paid the highest rebate rate of 106bps of RC or 35% of win in 1H11. MGM has actually had the highest rebates since 2008 (103bps/35% in 2010)

- MPEL paid the highest junket commission of 30bps of RC or 10.8% of win in 1H11. MPEL has consistently had the highest junket commissions since 2008 (36bps/12.25% in 2010)

- MGM had the highest all-in rate including comps of 140bps of RC in 1H11 (137 in 2010) while MPEL has the highest all-in rate including comps as a % of win of 46.7% (46.9% in 2010)

- LVS hold the prize for deriving the largest % of its revenues from non-casino revenues, however, given the scope of their business they also have the largest non-gaming comps.

- LVS non-casino comps were 16bps of RC volume or 5.3% of win in 1H11 (18bps/6.2% in 2010). LVS has consistently been the highest non-casino comper since 2008, however, comps as a % of win and RC have been steadily declining since 2008.

- MPEL’s non-casino promotional expenses as a % of RC and win are the lowest on the street

- Comps were 7bps of RC or 2.6% of win in 1H11 (9bp/3.1% in 2010)