THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - August 31, 2011

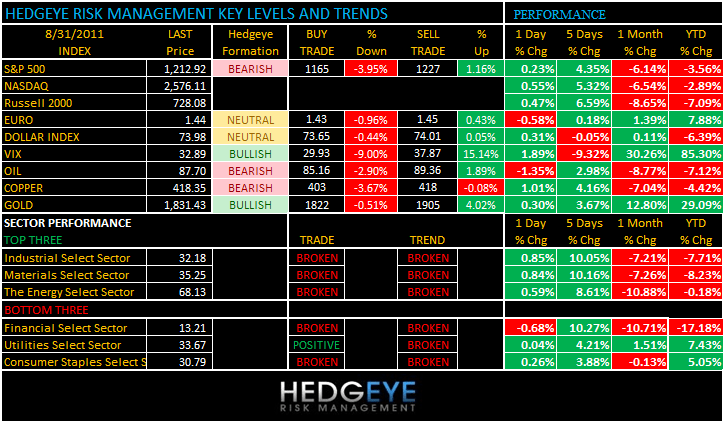

Despite a significant downturn in equity prices during August, the S&P 500 is now 10% “off the lows” into month-end. The market faces a difficult macro calendar in September including another attempt from the Obama administration to jump-start the economy. As we look at today’s set up for the S&P 500, the range is 62 points or -3.95% downside to 1165 and 1.16% upside to 1227.

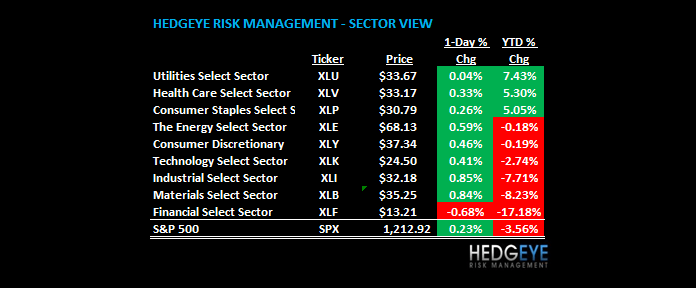

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +762 (-1722)

- VOLUME: NYSE 1017.24 (+11.51%)

- VIX: 32.89 +1.89% YTD PERFORMANCE: +85.30%

- SPX PUT/CALL RATIO: 1.84 from 2.26 -18.61%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 32.05

- 3-MONTH T-BILL YIELD: 0.01% -0.01%

- 10-Year: 2.19 from 2.28

- YIELD CURVE: 1.99 from 2.08

MACRO DATA POINTS (Bloomberg Estimates):

- 7 a.m.: MBA Mortgage Applications, prior (-2.4%)

- 7:30 a.m.: Challenger Job Cuts, prior 59.4%

- 8:15 a.m.: ADP Employment, est. 100k, prior 114k

- 9:45 a.m.: Chicago Purchasing, est. 53.3, prior 58.8

- 10 a.m.: Factory orders, est. 2%, prior (-0.8%)

- 10 a.m.: NAPM Milwaukee, est. 52.7, prior 57.6

- 10:30 a.m.: DoE inventories

- 12:30 p.m.: Fed’s Lockhart speaks on economy in Lafayette, La.

WHAT TO WATCH:

- Tropical Storm Katia may become hurricane later today, National Hurricane Center says; path uncertain

- Lions Gate (LGF): Carl Icahn agreed to sell his Lions Gate shares for $7 each to end battle for control over the studio. Parties agreed to end all litigation

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Containers Slump to 50-Year Low as Sales Slow: Freight Markets

- Mongolia Said to Plan Three-City IPO for Tolgoi Next Year

- Oil Heads for Monthly Decline as Slower Growth Curbs Demand

- Coal Discount Shrinking in Asia on Japan Rebound: Energy Markets

- Copper Set for First Monthly Drop in Three on Growth Concern

- Colombia Raises Gold Reserves by 2.3 Tons in July, IMF Data Show

- Oil at 4-Week High as Stimulus Speculation Counters Supply Gain

- Chan Exits Sino-Forest 22 Years After Tiananmen ‘Nightmare’

- Oil Rises to Highest Level in Almost Four Weeks as Fuels Climb

- Vietnam Coffee Said to Be Trading at Discount on Record Harvest

- U.S. Natural Gas Output Rises to Highest Since January 2005

- Gold Rises in New York on Expectations Fed Will Continue to Ease

- Sugar to Drop as Europe, India Boost Supplies, Kingsman Says

- Commodity Shipping Costs Fall as China Ore Stockpiles at Record

- Coffee Rallies as World Supply May Tighten; Cocoa, Sugar Decline

- Rubber Drops From Three-Week High on Concern Economy to Slow

- Wheat Drops on Speculation Demand for U.S. Exports May Shrink

- Copper Rises to Three-Week High on U.S. Economic-Growth Outlook.

CURRENCIES

EUROPEAN MARKETS

- Germany Jul retail sales (1.6%) y/y vs consensus (1.9%), prior revised (2.1%) from (1.0%)

- Germany Aug unemployment change (8K) vs consensus (10K), unemployment rate +7.0% vs consensus +7.0%

- Greece is burning down 4%

ASIAN MARKETS

- Most Asian markets traded higher this morning despite weak US consumer confidence; China’s performance was uninspiring +0.03%

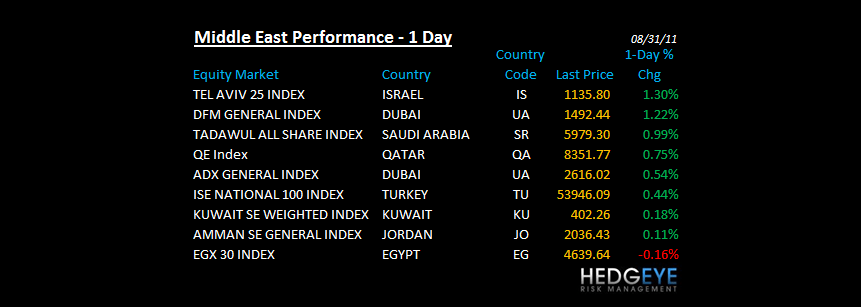

MIDDLE EAST

Howard Penney

Managing Director