The policy of inflation, and the stagflation that results, is weighing on confidence in the United States.

As the August 12th edition of the Early Look stated, “If the similarities between 2011 and 2008 are bad, the differences are almost worse.” The University of Michigan Confidence number for August was the worst reading for that metric since 1980. Today’s Conference Board number is the lowest level for more than two years and its seventh lowest level on record.

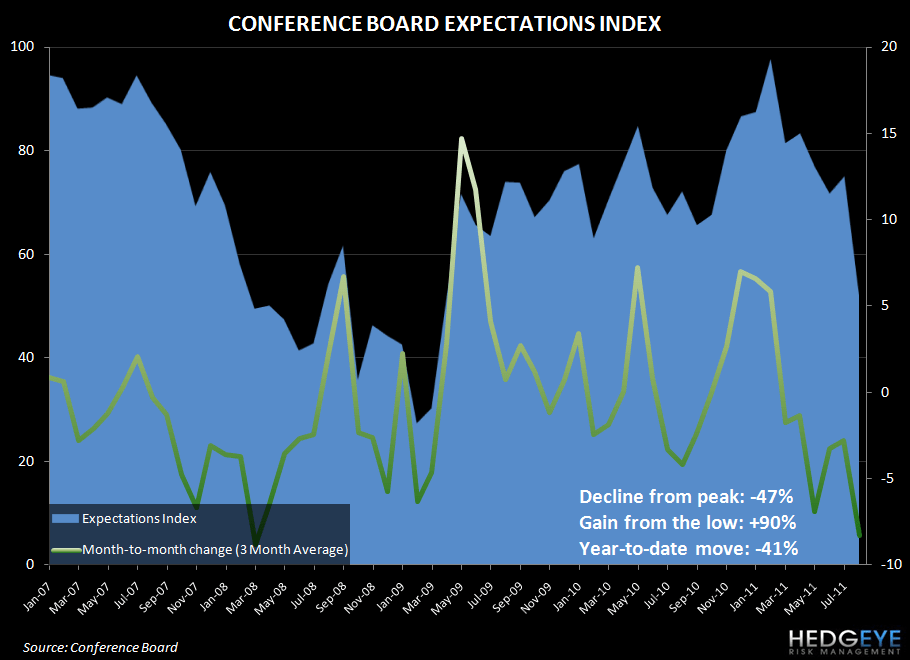

Today’s Conference Board Consumer Sentiment Index print confirmed what we already knew: inflation as a policy, and the stagflation that has resulted, is weighing on confidence. Confidence in August came in at 44.5 versus expectations of 52. The sequential drop from the revised July figure of 59.2 was the largest point drop since October 2008. On August 12th, following the release of the University of Michigan Consumer Confidence number for August also missed expectations by a wide margin. For an economy that relies on consumption for roughly 70% of its GDP, this is a worrying trend. As the chart immediately below illustrates, the confidence print has missed expectations on three-of-the-last-four Conference Board releases.

The improvement in consumer sentiment over the past couple of years has been almost entirely driven by the expectation that future conditions were to improve while consumer perceptions of the present situation have been flat (at a historically low level) with some marginal uptick. We have dubbed this growing spread “The Optimism Spread”. As the chart below illustrates, this spread has collapsed in recent months as Washington’s incompetence has been under the spotlight as outlook for employment soured and volatility in financial markets increased greatly.

All in all, despite gasoline prices coming down from their May peak, and declining during the month of August, confidence has cratered in the United States. Jobless Stagflation is not something the Hedgeye Macro team has been highlighting for some time and we believe the impact of a broken monetary policy is being underscored by these ugly economic data points.

Howard Penney

Managing Director