Positions in Europe: Short EUR-USD (FXE); Short UK (EWU)

There’s been plenty of “pin-action” in European capital markets over the last weeks, including yesterday’s equity market rally (the Athex closed up +14.4%) on merger talks of Greece’s second and third largest banks (Eurobank & Alpha Bank), however little has changed in our outlook over the intermediate TREND to longer term TAIL. The fundamental data remains skewed to the negative (with slowing growth and inflation sticky; and declining confidence ) across much of the region and we see a huge political football ahead of us in the passing of the EFSF, including the ultimate size of the facility, which is not part of the terms, when the governments of Europe vote on its ratification in late September and early October.

Given this time frame, we think there’s plenty of more downside in the capital markets of not only the PIIGS, but also the core, as uncertainty breeds discontent. We were early to flag the negative inflection in German high-frequency data in early Q2 and contagion effects as Italy and Spain move into the sovereign debt spotlight. We’re currently short the EUR-USD with an immediate term TRADE range of $1.42 to $1.45 and remain short the UK’s sticky stagflation [CPI at +4.4% in July Y/Y and Q2 GDP at +0.7% Y/Y or +0.2% Q/Q].

Political Pandering

As we wait and watch for the European governments to vote on the terms of the EFSF, it’s worth calling out quotes from leaders in recent days. In short, their remarks demonstrate 1.) how uncertain the environment is, that is the health of sovereigns and European banks, 2.) political pandering for reelection purposes, and 3.) the lack of coherent go-forward policy (constitutional provision) to mandate fiscal consolidation; mechanisms to allow banks to fail; and assistance plans beyond mere bailout band-aids (Euro-bonds?). Here’s what stood out:

German Chancellor Angela Merkel: “Many are worried, but they don’t need to be because the currency is stable… It’s our aim to come out of this stronger than we went into it, as we did during the banking crisis. I said that in 2009, and look at where the economy is in 2011. This can be achieved again.” (8/29)

Polish Finance Minister Jacek Rostowski: "European elites, including German elites, must decide if they want the euro to survive - even at a high price - or not. If not, we should prepare for a controlled dismantling of the currency zone." (8/29)

IMF Head Christine Lagarde: Called for an “urgent” recapitalization of Europe’s weakest lenders, saying that shoring up the banking system was key to cutting “chains of contagion” across the region. (8/28)

ECB chief Jean-Claude Trichet: “There is no liquidity or collateral shortage for the European banking system." (in response to Lagarde on 8/29)

EU monetary affairs commissioner Olli Rehn: "EU banks are significantly better capitalized now than they were one year ago…This has been confirmed by the stress tests in July. In the run-up of the tests, European banks increased their capital by some €50 billion.” (8/29)

Calendar Catalysts

As we move forward, here are a few calendar catalysts to keep front and center:

German EFSF vote – the German parliament has moved back its schedule vote on the EFSF changes from Sept 23 to Sept 29 or Sept 30 due to the Pope’s visit to Berlin. Michael Meister, the senior finance and economy spokesman for Merkel’s Christian Democrats, said Merkel would be able to secure a majority of her coalition voting in favor of the changes. HE: This decision will be tight. As of now, it looks like the headlines may be a bit inflated—we think Merkel gets the vote passed, despite her and her party’s waning confidence. Remember, Germany is playing its cards with the largest voice in Europe. Germany doesn’t want to go about bailing out Europe on its own (even if it ultimately must) and will politic to get the terms it wants.

Germany’s constitutional court is scheduled to deliver its opinion on Germany’s participation in Eurozone bailouts on Sept 7. HE: We expect the court to rule in favor of the legality of the State’s right to bailout European neighbors. In any case, this will be an important sentiment gauge for the EFSF.

ECB meeting on Sept 8 - The ECB will be releasing new staff projections for inflation and growth. HE: Expect downward revisions!

Risk Monitor

Directly below is a chart of European 10YR bond yields across the PIIGS and 5YR CDS. A few callouts include:

1) While yields are off their mid-July highs (except for Greece), we expect the trend to remain up and to the right.

2.) We’re focused on yields in Italy and Spain, two countries that present exponentially more sovereign debt risk than their peripheral peers. While yields have remained below the 5% level for a couple of weeks, this has been a function of the ECB’s SMP bond purchasing program. Trichet has indicated unwillingness for the SMP to be a significant program (in size or duration) meaning yields could well rebound should policy change.

3.) Greece is running away. Yields indicate Greece should be in default. The powers that be are doing all they possibly can to prevent this reality. As Keith says, gravity cannot be stopped.

4.) We are keeping a close eye on France, which is critical to the EFSF, and where swaps widened by 12 bps to 165 bps week-over-week. We believe the CDS market is currently pricing in decreased hedge effectiveness in addition to improvement in sentiment around sovereign solvency.

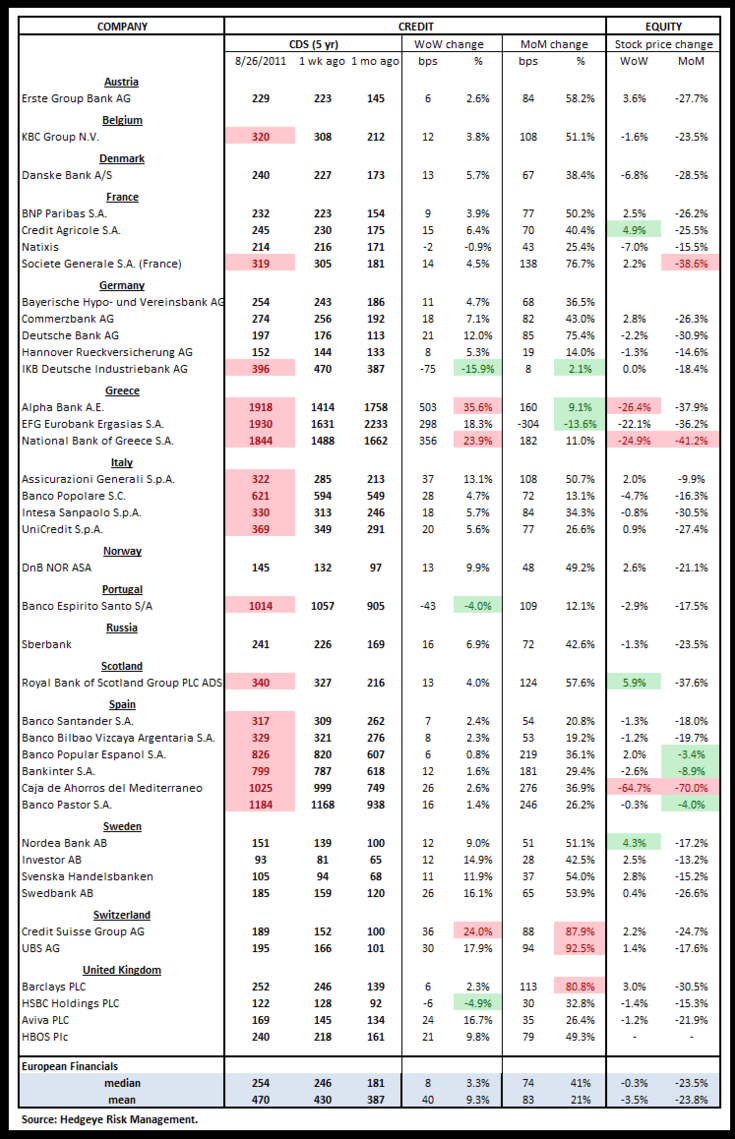

European Financials CDS Monitor – Bank swaps in Europe were wider last week (on a w/w basis from Friday’s close). 35 of the 39 swaps were wider and 4 tightened. The average widening was 10%, or 40 bps, and the median widening was 3%. The unanswered question remains the extent to which the EFSF could support failing banks. Stay tuned.

Matthew Hedrick

Senior Analyst