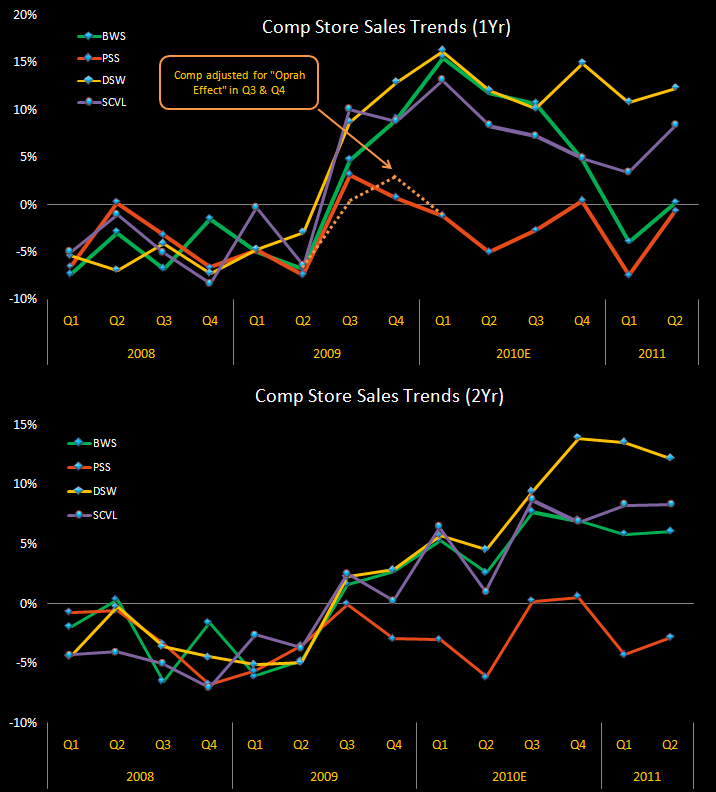

Solid number out of DSW capping off results out of the family footwear space. But looking forward, the key issue for us here is that this is a company that we think is average quality at best that is growing into more expensive real estate. And even though it is getting better property deals given the current environment, it still needs to comp at 2-3x the rate of its peers to leverage SG&A (this is the Dick’s Sporting Goods of shoes). It has been comping better than 10%+ for seven quarters now. Was DSW lucky, or was it good? Probably a little of both. But what we know is that another quarter out DSW definitely HAS TO be good. VERY good. We’re not willing to give this one the benefit of the doubt. The business model is simply too complex and inefficient, and too many things are going its way right now.

Here are a few additional callouts from the quarter:

- The driver here continues to be comps coming in up +12.3% coupled with gross margin expansion. With comps up LDD in the 1H of F11, the company’s updated outlook for full-year comps up MSD implies a sharp 2H deceleration with 2-year comps coming in 400-500bps.

- DSW was the only company in the family footwear space to post gross margin expansion (+240bps) in Q2 despite LDD product cost increases across the space. We suspect these results were driven by continued success in growing accessories and private brands.

- Inventory growth was modest up +3% on +15% sales growth resulting in a positive sales/inventory spread for the first time in the last five quarters despite higher costs. In fact, DSW is the only company in the space in the upper right quadrant with PSS, BWS, and SCVL all currently in the bottom right.

- The company updated its outlook for the full-year taking EPS guidance up only $0.05 to $2.70-$2.85 despite a $0.11 beat suggesting softer 2H expectations. It will be interesting to hear how the company is planning for the 2H as the leader of the family footwear pack.