“Make it less random to make it feel more random.”

-Steve Jobs

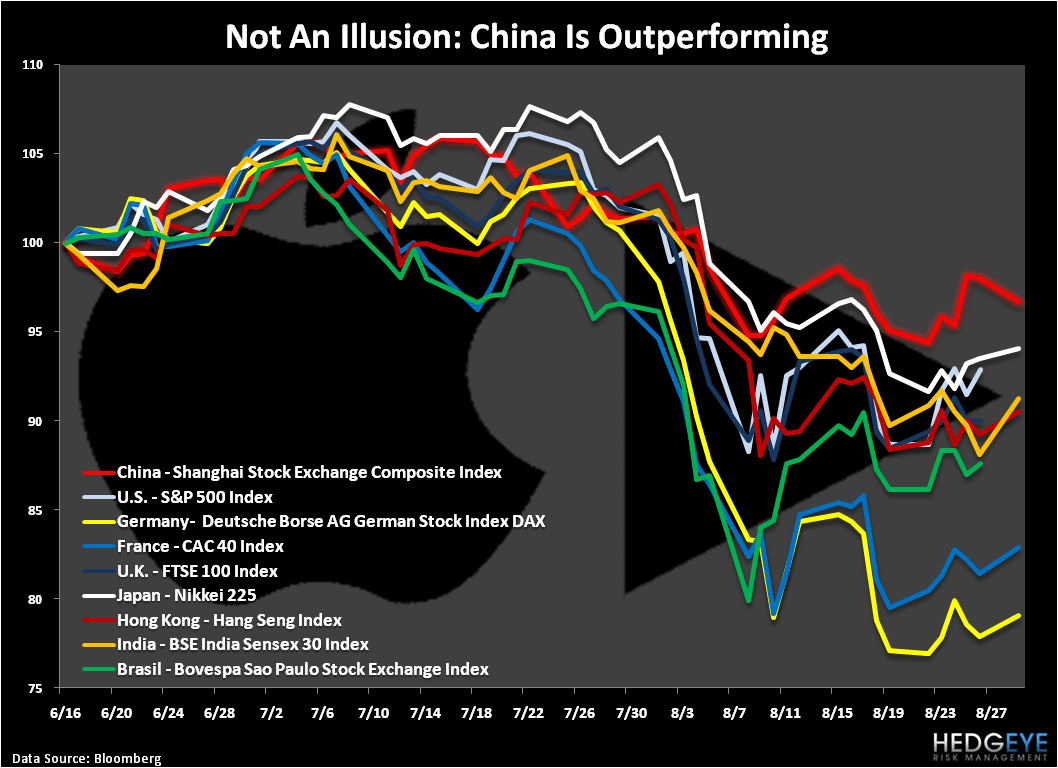

That’s not a quote to explain why Greek stocks can move up +10.2% this morning (after having crashed -48% since February). That’s what Steve Jobs said about getting the “shuffle” feature right for your iPod.

Dan Gardner (author of “Future Babble – Why Expert Predictions Fail and Why We Believe Them Anyway”) used this Apple analogy to hammer home his point about what psychologists call “the illusion of control.”

“People are particularly disinclined to see randomness as the explanation for an outcome when their own actions are involved. Gamblers rolling dice tend to concentrate and throw harder for higher numbers, softer for lower.” (Future Babble, page 75)

This, of course, is ridiculous. But only the ridiculous can explain much of the “expert” storytelling in our profession.

Last week, I kicked off Monday’s Early Look with a note titled “Uncertainty and Non-Linearity” and I had a tremendous amount of feedback from clients (thank you) on the concept of embracing Uncertainty in both our lives and risk management processes. This morning the process has not changed. My positioning has.

With plenty of asset classes on sale throughout different parts of the week, I was able to put 9% of our 70% Cash position to work by buying Corporate Bonds (LQD), Silver (SLV), and taking up our US Equity exposure from 0% to 3%.

I know, call me a wild and horned up bull.

Here’s how the Hedgeye Asset Allocation Model looks this morning (8 positions):

- Cash = 61% (down from 70% last Monday)

- Fixed Income = 21% (Corporate Bonds, Long-term Treasuries, and a US Treasury Flattener – LQD, TLT, FLAT)

- International Equities = 6% (China and S&P International Dividend ETF – CAF and DWX)

- International Currencies = 6% (Canadian Dollar – FXC)

- Commodities = 3% (Silver – SLV)

- US Equities = 3% (Utilities – XLU)

People always ask me what would get me to change my “market view.” I then have to ask them what market they are asking about. I am a Global Macro man who works with a 40 person team across countries, currencies, commodities, etc, so the answer isn’t as random as where the Dow is going next.

The answer actually gets down to last price. Prices Rule in my multi-factor, multi-duration, Global Macro risk management model. To put that more simply – as prices, volumes, and volatilities change, I do.

A lot of people do not deal with managing risk that way. Some are absolutely certain that God endowed them with a super special ability to think about “valuation” better than you or I can. Some think that markets owe them a “rate of return above the risk free rate.” Some actually don’t put much thought into it at all and just buy all dips.

Across asset classes, here’s what my core 3 factor model (PRICE/VOLUME/VOLATILITY) said the market was saying week-over-week:

- US DOLLAR INDEX = DOWN -0.3% week-over-week and down for the 2nd consecutive week, reminding us that there is no strong US Dollar policy that the Globally Interconnected Marketplace actually believes. If I have written this 100x since 2007, I have written it 1000x - devaluation is not the best path to long-term economic prosperity. It perpetuates short-term inflations.

- CANADIAN DOLLAR = UP +2% week-over-week and proving itself where both US Congress and Les Eurocrats can’t (political solidarity). Canada is being led toward a majority that the Globally Interconnected Currency Market can attempt to trust.

- EURO = FLAT week-over-week as the Europeans do nothing to change the world’s view that they have no political union that can be believed in. The ever so important vote on the EFSF (European Financial Stability Facility) is up next (late September).

- COMMODITIES (CRB Index) = UP another +1.8% week-over-week and holding above both its long-term TAIL and immediate-term TRADE lines of support. This is the Stag in Stagflation that is associated with a debauched US Dollar policy.

- OIL = UP +3.8% week-over-week outperforming overall commodity inflation by more than a 2:1 ratio. Getting the stock market up by getting the energy stocks up also gets consumers a nice tax at the pump for Labor Day weekend.

- COPPER = UP +2.7% week-over-week to $4.11/lb but not enough to get Dr. Copper back above either its long-term TAIL or immediate-term TRADE lines of resistance (both are converging around $4.17/lb). Copper trading sustainably above $4.21/lb would be one of the key leading indicators that would change my Global Growth Slowing research view.

- GOLD = DOWN -3% week-over-week after making all-time weekly closing highs for almost every week of Q3 2011 before that. If you shorted Gold last week, you feel shame this morning. We are long Silver as we think it has less hedge fund risk right here and now than Gold does. Gold and Silver will continue to outperform when real-interest rates are negative.

- VOLATILITY (VIX) = DOWN -17% week-over-week and while it’s not conventionally considered an asset class, I don’t see why it shouldn’t be given that the Fed, ECB, and BOJ (Fiat Fools): A) shorten economic cycles and B) amplify market volatility.

- US TREASURIES = FLAT on the short end and DOWN on the long end last week as long-term Treasury bonds were immediate-term TRADE overbought in the week prior. Nothing has changed the Treasury Bond Market’s view from an absolute yield pricing perspective. For me to change, I’d need to see greater than 0.28% and 2.49% on 2-year and 10-year yields, respectively.

- US TREASURY YIELD SPREAD = UP 13 basis points week-over-week as the long-end of the Treasury curve rallied (10-year went from its YTD low of 2.06% to 2.19% by Friday). We continue to see the intermediate-term TREND of Yield Curve COMPRESSION as one of the most important leading indicators of both US Growth Slowing.

All the while, US stock market bulls had a wonderful week with the SP500 closing up +4.7% (up for its 1stweek in the last 5). But, Prices Rule, and while I moved off of the ZERO bound last week (asset allocation to US Equities = 3%), that certainly doesn’t make me a bull on either an intermediate-term TREND or long-term TAIL duration. I’d need to see an SP500 close above 1263 for that.

“For humans, inventing stories that make the world sensible and orderly is as natural as breathing. That capacity serves us well, for the most part, but when we are faced with something that isn’t sensible and orderly, it’s a problem” (Future Babble, page 81). That’s why I’ll stick with my own storytelling that both accepts Uncertainty and that the market’s last price makes perfect sense.

My immediate-term TRADE ranges of support and resistance for Gold, Oil, and the SP500 are now $1, $81.35-88.58, and 1154-1191, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer