Here’s a note from our Macro team on why any form of incremental easing – if it comes at all – will be a 2012 event.

Conclusion: As we anticipated, Chairman Bernanke did not provide an indication that incremental easing is coming in the short term today in his speech in Jackson Hole. Our view is that if it comes, it is likely a 2012 event.

The most focused-on stock market event of the week in Jackson Hole, Wyoming has turned out to be largely a non-event. The text of Chairman Bernanke’s speech was circulated prior to him giving the speech at 10am eastern this morning. We spent time parsing through his comments and there was really no change from his prior public comments. Specifically, Bernanke stated the following this morning about policy duration:

“In particular, in the statement following our meeting earlier this month, we indicated that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013. That is, in what the Committee judges to be the most likely scenarios for resource utilization and inflation in the medium term, the target for the federal funds rate would be held at its current low levels for at least two more years.”

Chairman Bernanke went on to say that while the Federal Reserve is willing to “employ its tools as appropriate to promote a stronger economic recovery in a context of price stability”, he stopped short of indicating what form incremental stimulus would take and on what time frame. Thus, the great QE3 waiting game continues.

Our view of incremental easing remains that the Federal Reserve will be in a proverbial box in terms of incremental easing until at least the end of 2011, if not well into 2012. The primary reason for this is simply that the data will not support further easing.

In the chart below, we graph all-items CPI going back three years and highlight when QE1 was announced and then implemented and also highlight when QE2 was hinted and then implemented. The key takeaway is that inflation was running at much lower levels, largely below 1%, when the first two rounds of quantitative easing were implemented. Currently, this measure of inflation is north of 3% and set to remain at that level through the next couple of quarters based our models.

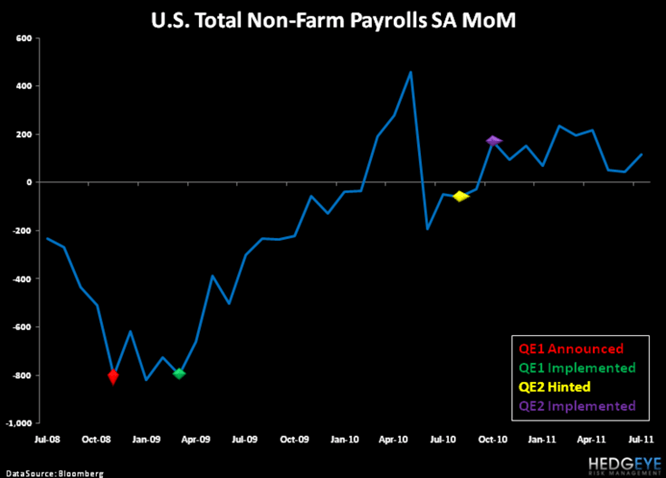

Just as pertinent to Fed decision making is employment data. As the chart below outlines, in the prior two periods of quantitative easing, monthly non-farm payrolls witnessed a substantial and sustained decline of at least three months. As of now, monthly non-farm payrolls are still positive, albeit marginally and the last three months, ending in July, have averaged additions of only 72K. This is a substantial decline from the prior three months, which averaged 215K additions. Nonetheless, history suggests that we would need to see negative payrolls for a sustained period prior to incremental easing being implemented.

Stepping back, the majority of Bernanke’s speech today related to the theme of the actual conference, which is the outlook for the longer term prospects for the U.S. economy. Bernanke spent a good portion of the speech addressing his perspective on both the positives and negatives relating to long term economic growth of the United States. The one area which he flagged as an impediment to the economic prospects was fiscal policy. To quote the Chairman:

“. . . the country would be well served by a better process for making fiscal decisions. The negotiations that took place over the summer disrupted financial markets and probably the economy as well, and similar events in the future could, over time, seriously jeopardize the willingness of investors around the world to hold U.S. financial assets or to make direct investments in job-creating U.S. businesses.”

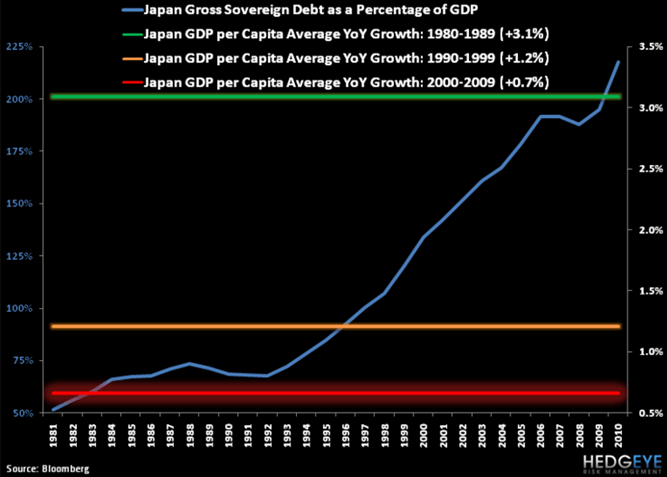

In part, the negotiations around the debt ceiling have been an issue, but, if anything, they characterize a short term impediment. Longer term is the actual issue of structural deficits and debt. While we aren’t necessarily surprised, it would have been valuable to have Bernanke address these issues head on for what they are: long term impediments to U.S. growth. We have oft quoted Reinhart and Rogoff’s data from, “This Time is Different”, which clearly shows that as nation’s debt-to-GDP accelerates beyond 90%, its future growth slows. In the last chart below, we show this graphically for the Japanese economy.

My colleague Darius Dale wrote a note earlier today discussing monetary policy of Australia. In the note, he quoted Bank of Australia Governor Glenn Stevens who recently noted:

“In terms of macroeconomic ammunition, there would be not that many countries who could say they had more than us in the event of a really big episode.”

We are obviously not big fans of government intervention, but one key risk to consider in a more dire economic scenario, is that the Federal Reserve, unlike Australian counterpart, is largely out of ammo.

Daryl G. Jones

Director of Research