Crusher number. But hindsight matters not. Things are turning down for the high end consumer in 4Q.

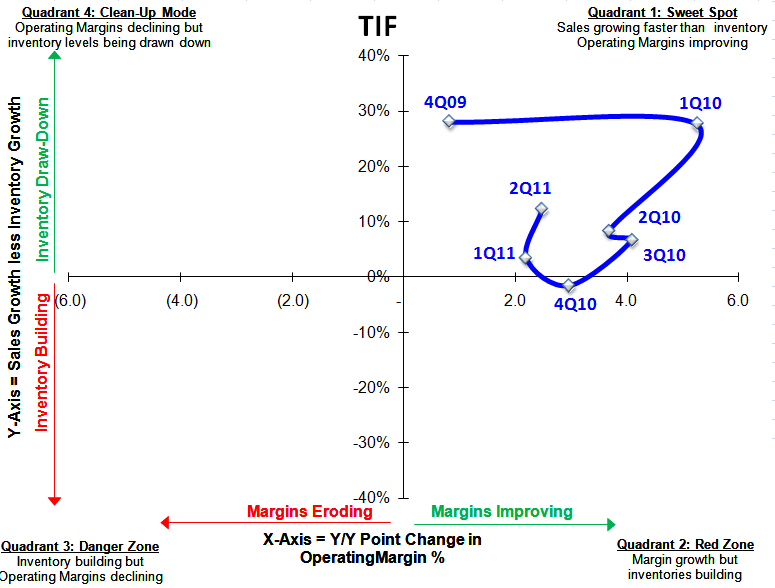

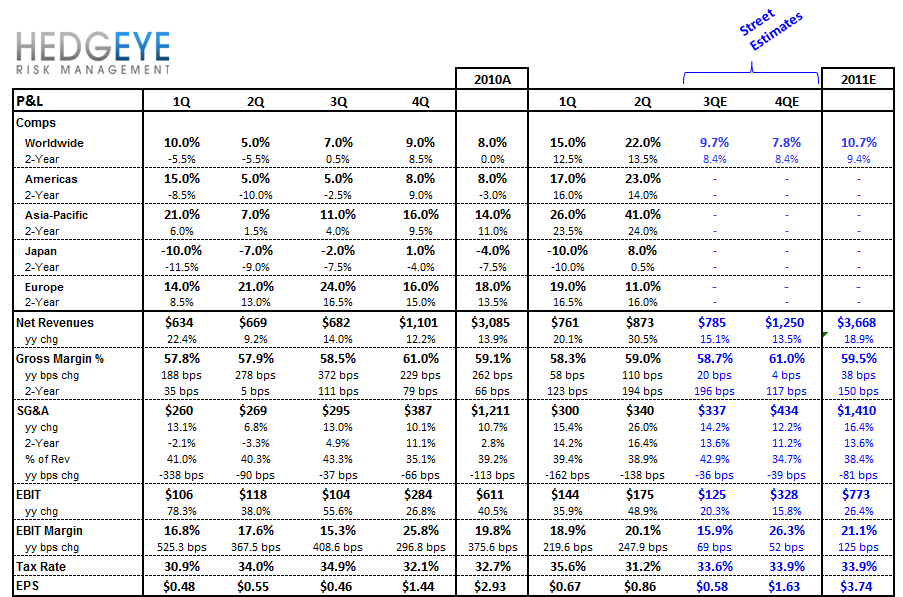

Big number from TIF, even though we think a cleaner number is $0.04 below the ‘adjusted’ print of $0.86 (a truer number is $0.70 due to $0.16 of HQ costs – but that was stripped out of expectations). The driver here was clearly in comps, which were up sequentially in every region sans Europe (where they still printed a healthy 11%. 2-year comps remain healthy, and accelerated meaningfully in Japan, which was the biggest surprise. The SIGMA chart swung to the upper right, which marks one of the few companies to do so this quarter. All-in, it looks quite healthy at face value.

BUT, and there’s a big but, this is all backward looking. We feel strongly that we’ve not only seen a meaningful slowdown in high end spending in August, but have also seen inventory of diamonds and gold backing up in the supply chain. Maybe TIF is strong enough to delay this for quarters past their competition, but all it can do is kick the can down the road. The inevitable will come it’s way.

It should be an interesting call.

We’ll be back w any relevant info after the 8:30 call.