This note was originally published August 25, 2011 at 10:26 in Financials

Past as Prelude?

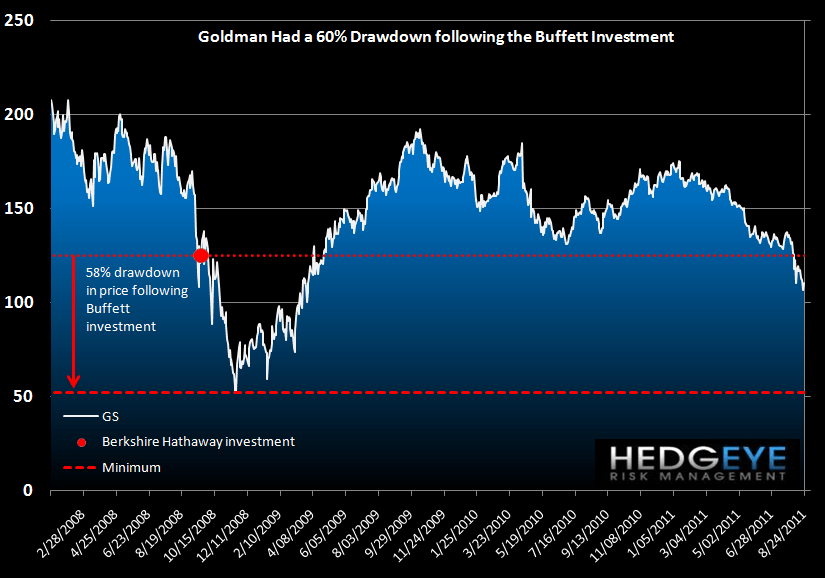

Warren Buffett announced a $5 billion investment in Bank of America this morning. Goldman Sachs was a nearly identical investment for Buffet back on September 24, 2008. How did he fare on that one? The chart below shows Goldman's stock price following the investment. He invested $5 billion in 10% preferred with warrants struck at $115 when Goldman was trading at $125. Following the investment in Goldman, the stock closed 6% higher, but, importantly, went on to lose 58% over the next two months. Ultimately he made a solid return on the investment, but how many investors would be as comfortable as Buffett riding out a 58% drawdown?

Remember that Preferred is Senior to Common

Interestingly, we're not opposed to the idea of being invested at a level senior to the common equity. We share Buffett's sentiment that Bank of America is too big to fail. Remember that his original thesis for investing in Goldman was that the US Government wouldn't let them fail. Ultimately he was right. What's interesting is that his attachment point with the preferred puts him senior to the common holder and enables him to sidestep further dilution that may arise. While that dilution wouldn't be good for his 700 million common warrants at $7.14, he wouldn't lose any capital and he'd still earn his 6% return even if BAC ultimately has to raise an enormous amount of additional equity capital. This is a relatively risk free trade for Buffett and we applaud him for being creative in the midst of fear. That said, Buffett's investment doesn't create a risk-free trade for everyone else - investors who don't have access to the preferred shares. Don't make the mistake of thinking that a straight up investment in the common is comparable to what Buffett has just architected.

Bank of America Has Just Taken a Step in the Right Direction

We're not BAC curmudgeons over here. We try to evaluate the data for what it is. We acknowledge that this investment moves Bank of America forward in two important regards. First, they now have $5 billion more in capital than they had before. Considering the market was clamoring for them to sell China Construction in full so as to monetize roughly $7 billion in additional capital, this gets them almost as far along. Second, Buffett's "seal of approval" has significant intangible value, we get that. Nevertheless, as we stated yesterday, there are significant macro factors outside of Bank of America's control (and Buffett's for that matter) that the bank will continue to face in the next 6-12 months. Namely, the European banking crisis, a US growth slowdown, mortgage putback uncertainty and the conjunction of huge NIM pressure and ending reserve release. For reference, our firm's view on the US growth outlook is very different from Buffett's, and for Bank of America's outlook that difference matters.

The Quantitative Setup

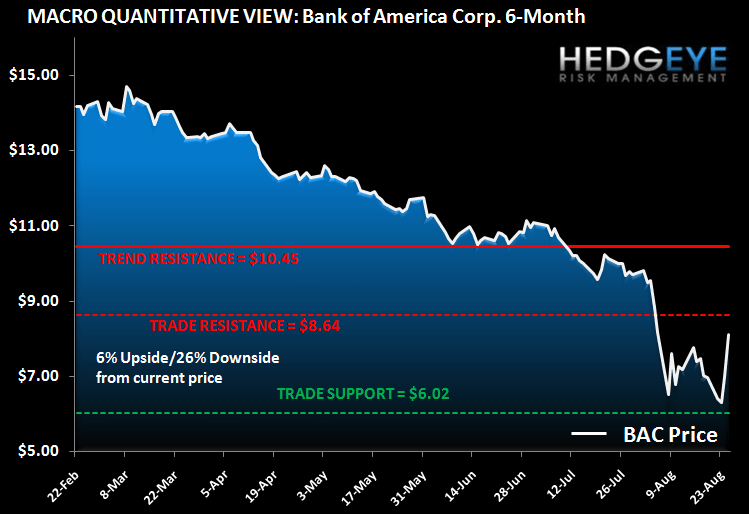

The chart below incorporates this morning's squeeze into our quantitative model. The heightened volatility this morning has widened the range in our model and we now see TRADE support at $6.02 and TRADE resistance at $8.64. This implies upside of 6% and downside of 26%. We are sticking with our short position based on that asymmetry. The chart below summarizes the setup.

Joshua Steiner, CFA

Allison Kaptur