The math says RevPAR growth should reaccelerate. Adopting a positive stance about the lodging sector is new to us this year so we hope people recognize the pivot.

Of course the economy matters for the hotel industry. It is cyclical after all. Our point is that the recent RevPAR slowdown was not macro economically driven. Rather, the math suggests that the comparisons in May, June, July, and the first half of August are much more difficult than the rest of the year. We’ve articulated our view in the past that there was significant pent up demand in those months last year where business people caught up on travel that had been postponed from the prior 12-18 months.

But we’re not talking about % growth last year as the comparison as every other analyst does. We are talking about dollar RevPAR seasonally adjusted viewed on a sequential basis. There has been too much volatility for three years now to look at YoY % comps. So sequentially last year (again, seasonally adjusted), dollar RevPAR accelerated beginning in May through the first half of August and then normalized in the 2nd half. This is why RevPAR growth should reaccelerate in the 2nd half of August this year through the end of the year, likely peaking in November.

The chart below shows the math we are talking about. Note the slight pick-up in August followed by strong RevPAR growth in each remaining month of the year. With three weeks in, August is almost in the bag. In fact, we saw the first week of reacceleration last week with Upper Upscale RevPAR climbing 8% versus 4% for the first 2 weeks. So far, our math is proving correct.

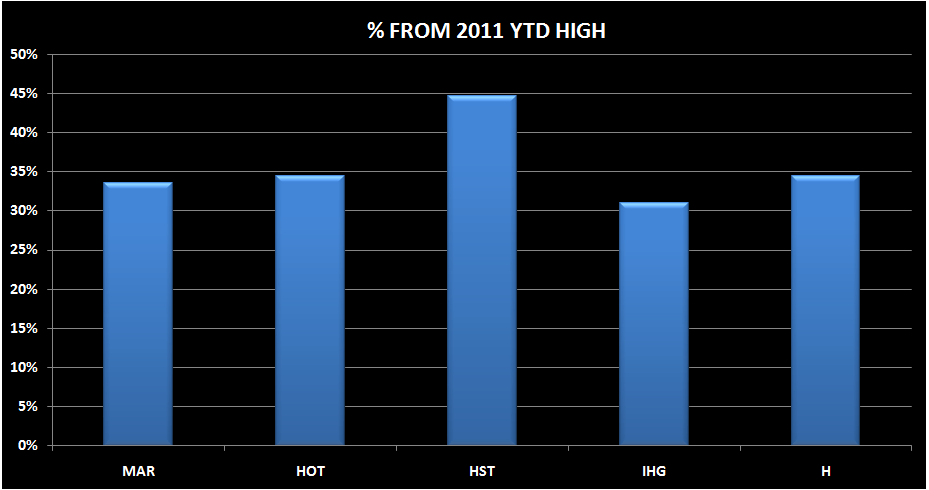

The slowdown in RevPAR growth coincided with the poor economic data, worsening investor sentiment, and a stock market correction so we can forgive people for making the correlation. However, we saw this coming even in a stronger economy and likewise, we see the reacceleration coming even in a weakening economy. Of course, the uptick will be short-lived should we enter a double dip – this is a cyclical industry after all. However, this industry has been battered and bruised by investors. Look at the recent stock price performance of some of the lodging stocks we follow:

We think the reacceleration of RevPAR will provide a much needed boost to sentiment which should inflate multiples over the near term. Lodging stocks look much better positioned than say gaming or cruise lines because of this math. Within lodging, MAR seems most interesting to us because of the historically low relative and absolute valuation. We haven’t seen relative sentiment this low on MAR in a long time. We also think the Street is underestimating MAR’s free cash flow and propensity to buy back stock. Finally, we think the time share spin-off is a strategically smart reallocation of capital that will return MAR’s timeshare fee business to one of growth.

We always worry about the economy and the Hedgeye Macro team is not the most bullish on the economy. Should the economy continue to struggle, MAR would clearly be one of the most defensive plays in the sector due to its soon to be close to 100% fee based business model. In fact, as noted in our 08/25/11 post “HOW LOW CAN WE GO”, MAR has the least downside to its March 2009 trough valuation. More on MAR in some upcoming posts.