“That the earth would give way beneath his feet was a grim irony for Mickey Mantle.”

-Jane Leavy in “The Last Boy”

The end of Summer 2011 is approaching. I’m packing up my family for Thunder Bay. And I’m smack in the middle of a Twittersphere debate about arrogance, confidence, and success.

Some people think confidence and success is fleeting because, for them, it really is. Winning is hard – but great teams find a way to make it both achievable and repeatable. I wake up every morning not only accepting the Uncertainty associated with being right in this business, but swallowing the adversity that each market day and competitor brings.

Tired old processes that refuse to evolve are threatened by us. We get it. I’ve seen my fair share of Grim Irony in the arena of life. Whether accountability was my being punched square in the face in a Canadian Junior hockey barn or reality was being fired 5 days before the birth of my 1st son, I get it. No one owes me anything in life and there’s plenty of earth to give way beneath me yet.

Back to the Global Macro Grind…

Mickey Mantle was the son of a lead miner. His Dad, Mutt Mantle, died young. Before his death, as a Yankee rookie The Mick had already blown out his knee and faced plenty of adversity both on the field and from tiring veteran teammates (DiMaggio). The lesson learned from Mutt though was simple – out of sight, our of mind - play the game that’s in front of you.

And so we will this morning…

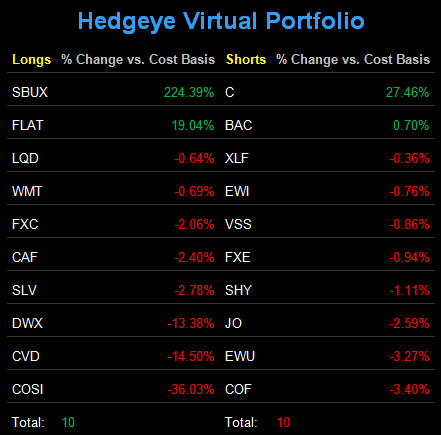

I took down my Cash position yesterday from 70% to 64% as there were some asset classes on sale that I continue to like – Corporate Bonds (LQD) and Precious Metals (SLV).

The Hedgeye Asset Allocation Model positioning is currently as follows:

- Cash = 64%

- Fixed Income = 21% (Long-term Treasuries, US Treasury Flattener, Corporate Bonds – TLT, FLAT, and LQD)

- International Currency = 6% (Canadian Dollar – FXC)

- International Equities = 6% (China and S&P Dividend ETF – CAF and DWX)

- Commodities = 3% (Silver – SLV)

- US Equities = 0%

I didn’t buy Gold yesterday (I might today – immediate-term TRADE support = $1705/oz and I’d like to see that critical risk management line of support hold before I try to play hero – for our Gold levels, see the Chart of The Day by Darius Dale attached). Instead, I bought back the Silver position that I sold on August 19th at $41.37 (SLV).

Being able to buy something that you sold higher is a wonderful feeling. A lot of people in this business call that “market timing.” And a lot of those same people say that “you can’t time markets.” Trust them on that – most of them can’t.

But if you could hit a baseball 734 feet (Mantle on May 22, 1963 at Yankee Stadium) or you could revolutionize the way people consume Apples (personal computing), why wouldn’t you try? While everyone else is whining, why wouldn’t you try it confidently?

Confidence breeds success. Success breeds confidence.

I’m certainly not suggesting Hedgeye is Mantle or Steve Jobs. But I am explicitly saying that Hedgeye is the greatest investment team I have ever had the pleasure and privilege to play on. We’re young. We’re evolving. And we have just as good an opportunity as any great Wall Street firm that has come before us to change the way this game is played. That’s exciting.

Until yesterday I had a ZERO percent asset allocation in the Hedgeye Asset Allocation Model to both US and European stocks and the entire Commodities complex. On one of those two things (Commodities), that was a good thing. On another (Stocks), it wasn’t – until China closed up big overnight (up +2.9% - we’re long Chinese Stocks) and US stock market futures are indicated down, again.

Again is as again does.

Over and over and over again, the Perma-Bulls have been buying stocks and changing their thesis as to why as they go. At the end of 2007 (the SP500 is still down -24.8% since then, fyi), it was because “stocks were cheap” and corporate America was “awash with liquidity.” Today, I guess their portfolios are still awash with US Equity exposure and stocks are getting cheaper.

But what does all of their storytelling and finger pointing really do for this country? People don’t trust this economic system or the people who manage it. If calling opacity out on the carpet is “arrogant”, I’ll happily be transparency’s child. America trusts winning and the Grim Irony of all of this back and forth about who is “perma” this and “perma” that is that very few have been Perma Right.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $81.24-89.23, and 1108-1191, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer