Gaming, lodging, and cruise stocks have taken a beating. A walk down memory lane suggests they could go a lot lower.

With fears of double dip percolating in the investment community, or potentially even worse - stagflation as predicted by our Hedgeye Macro team - we thought we’d take a trip down memory lane. So think back to the dark, dark period of March 2009 – specifically March 9th– when the world was about to fall apart. March 9th, of course, represented the low of the market (since 1997) and the stocks in my universe.

In this note, we take a look at where multiples were at that time and where they are now. The conclusion is that most stocks can fall significantly and still not reach previous low multiples, although there are some stocks that are fairly close to those lows. We’re not saying these stocks are going to go back to trough multiples but we also would caution those who are making claims of “limited downside”. Investors always seem to forget how low stocks can go.

Gaming Supply

Along with cruise lines, the gaming supply companies appear have the to the least downside. This is not surprising given the low financial leverage and relatively low fixed cost leverage of these businesses. WMS is actually trading slightly below the trough valuation. Investor expectations have turned WMS into a mature company from a pure growth company to the point where the stock is on its back. This may be one stock where we can say there is “limited downside”.

Major Market Gaming Operators

The big operators appear to have the most downside to their valuation lows. Part of the explanation here is that there were a couple of near bankruptcies – MGM and LVS – and MPEL had to pull off a refinancing. Not surprisingly, the equity of MGM would go to zero at the March multiple. The company was very close to bankruptcy and estimates were way too high back then. The stocks of WYNN and LVS could fall over 40% back to the trough multiple. MPEL has the least downside to trough and that is before considering that current estimates for NTM are 10-15% too low, in our opinion.

Regional Gaming Operators

Regional gaming companies have been decimated in the past month or so. PNK and ASCA are only 7-8% above their trough multiples. However, due to significant financial leverage, the stocks would fall 18% and 28%, respectively, to reach those trough multiples. Aside from the higher absolute leverage, ASCA may be the safer play since they are in aggressive deleveraging mode while PNK is still expending cash. From this analysis, PENN seems to have the most downside. Surprisingly, the company’s EV/NTM EBITDA was a full turn below the other stocks in the group in March of 2009. However, even if one assumes that 5x was an anomaly, PENN’s multiple could still fall 26% and not be below 6x. The stock has about 50% downside to reach the 5x multiple.

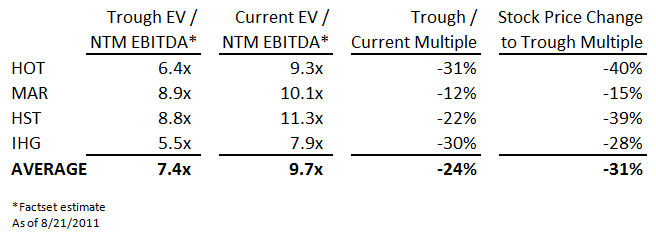

Hotels

Another sector that’s been crushed as of late is lodging but stocks still seem to have a long way to fall. The exception is MAR. Relative investment sentiment for MAR was considerably worse before the recent stock market correction. We think it is somewhat unwarranted and that MAR’s defensive business model leaves it less vulnerable to a downturn. We project only 15% downside in the stock to reach the trough valuation versus 31% for the entire group.

Cruisers

What’s interesting about the cruise lines is how cheap these stocks were at the trough on a P/E basis. RCL and CCL traded at only 5.5x and 8.0x, respectively, on NTM estimated EPS. Even if we use actual EPS over that time, P/E’s for both companies were only 0.5x higher. When it comes to market crashes, valuation clearly doesn’t matter for the cruise line stocks. People will sell this discretionary sector at ridiculously low multiples.