THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - August 23, 2011

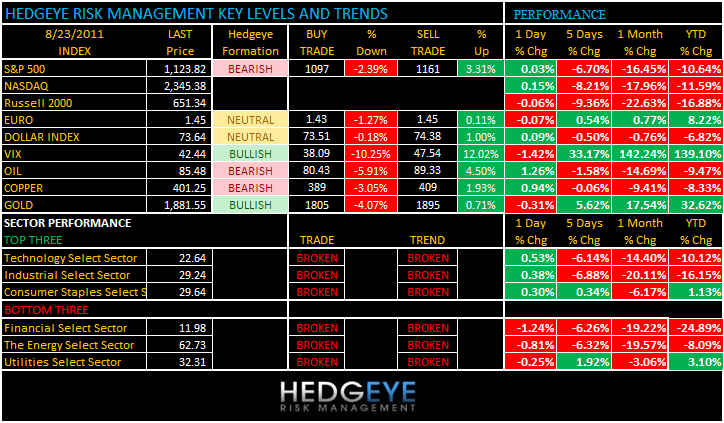

Bottoms are processes, not points – and, globally, that’s going to take some time as long as the economic data and market prices continue to lean bearish. As we look at today’s set up for the S&P 500, the range is 64 points or -2.39% downside to 1097 and 3.31% upside to 1161.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -356 (+1217)

- VOLUME: NYSE 1191.57 (-21.03%)

- VIX: 42.44 -1.42% YTD PERFORMANCE: +139.10%

- SPX PUT/CALL RATIO: 2.01 from 1.67 +20.01%

CREDIT/ECONOMIC MARKET LOOK:

UST YIELDS – The Hedgeye downside target in the 10-year was hit right on the nose on Friday (2.06%) and now you’re seeing the proactively predictable bounce in bond yields that is inversely correlated with Gold/Silver; remember Gold/Silver really outperforms when real-rates-of return on bonds are negative; the immediate-term TRADE range for 10s is now 2.01%-2.19%; manage risk around that range.

- TED SPREAD: 30.84

- 3-MONTH T-BILL YIELD: 0.01% -0.01%

- 10-Year: 2.10 from 2.07

- YIELD CURVE: 1.88 from 1.87

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45 a.m.: ICSC weekly sales

- 8:45 a.m.: Alan Greenspan Q&A at Washington Convention Center

- 8:55 a.m.: Johnson/Redbook weekly sales

- 10 a.m.: July new home sales, est. 310k, prior 312k

- 10 a.m.: Aug. Richmond Fed manufacturing, est. -5, prior -1

- 11:30 a.m.: U.S. to auction $35b 4-wk bills, $25b 52-wk bills

- 1 p.m.: U.S. to auction $35b 2-year notes

- 4:30 p.m.: API inventories, prior crude build 1.75m bbl

WHAT TO WATCH:

- New homes sales in the US due out this morning should be another bearish data point for both Americans and the financial stocks.

- Newmont Mining (NEM); Plans new underground exploration in New Zealand, may extend gold, silver mining to 2020 and beyond

- Hurricane Irene strengthens to category 2 storm, threatening U.S. coast

- McGraw-Hill has “underperformed its potential” and should break into 4 parts, shareholders Jana Partners, Ontario Teachers’ Pension Plan proposed

COMMODITY/GROWTH EXPECTATION

- STAGFLATION – begging for the Bernank to QE3 us is keeping a lid on any USD recovery and that’s a problem for Sticky Stagflation – yesterday the CRB Index was up 2pts on the day and this morning commodities are in many cases outpacing equity market gains. We will get less bearish on Equities, globally, when Oil is at $72.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Gold Tops $1,910 for First Time as Platinum Reaches 3-Year High

- Silver `Neckline' Break May Signal 15% Rally: Technical Analysis

- Oil Gains a Second Day on U.S. Fuel Demand, Libya Supply Outlook

- Australia May Ship Most Wheat Since 2004: Freight Markets

- Oil Supplies Gain in Survey on Reserve Release: Energy Markets

- Copper Rises on Improving Chinese Demand, U.S. Stimulus Outlook

- Shanghai Gold Exchange Raises Margin Requirement to 12%

- Irene Strengthens to Category 2 Storm, Threatening U.S. Coast

- ‘Saudi Arabia’ of Copper Fails to Lift Output: Chart of the Day

- Corn Advances to 10-Week High as U.S. Crop Condition Worsens

- King Says Commodity Price Drop to Ease Income Squeeze Sooner

- Palm Oil Gains as Dry Weather Threatens Soybean Crop Prospects

- Gold Extends Rally Above $1,900 as Economic Concerns Lift Demand

CURRENCIES

EUROPEAN MARKETS

- EUROPE – PMI numbers across the board for August are plain bearish, but markets have been pricing that in so we’re seeing another low-volume, low-conviction, rally in everything that’s been going down (other than Greece, which is down again this morn and down -45% since FEB); most interesting number was France dropping below the 50 line on PMI; GDP expectations in France (and their AAA rating) need to come down.

- EuroZone Aug preliminary Manufacturing PMI 49.7 vs consensus 49.5 and prior 50.4

- EuroZone Aug preliminary Services PMI 51.5 vs consensus 50.9 and prior 51.6

- EuroZone Aug preliminary Composite PMI 51.1 vs consensus 50.1 and prior 51.1

- German Aug ZEW current conditions 53.5 vs consensus 87.0; economic sentiment (37.6) vs con (25.0)

ASIAN MARKETS

- ASIA: China put up a better than bad number last night and stocks stopped going down +1.5% overnight; Korea stopped crashing, which is nice.

- HSBC Flash Manufacturing PMI for China beat expectations and came in higher m/m, still indicated a contraction.

MIDDLE EAST

Howard Penney

Managing Director