“Linearity isn’t the norm in the world around us, non-linearity is.”

-Dan Gardner

That’s another quote from the book I referenced last week that I am in the middle of reading – “Future Babble – Why Expert Predictions Fail and Why We Believe The Anyway.”

What’s interesting about both Chapter 2 (“The Unpredictable World”) and the book is that it’s really accessible for non-scientifically inclined readers. You don’t have to have a Ph.D. in fractal math or applied physics to grasp the deep simplicity of a few very important concepts – Uncertainty and Non-Linearity.

In Hedgeye’s Research and Risk Management Process, Uncertainty is critical to accept. Maybe that’s why our models have had very different signals than consensus during both the 2008 and 2011 Growth Slowdowns. Wall Street/Washington models tend to command some level of certainty in their baseline assumptions. Being absolutely certain about models that don’t work is a problem.

In the real-world of accountability, successful Buy-Side Risk Managers like Ray Dalio (Founder of $100B Bridgewater Associates) have embraced Uncertainty as a core component of what it is that they do. As Dalio says in John Cassidy’s New Yorker article (“Mastering The Machine”, July 25, 2011):

“I’m always trying to figure out my probability of knowing... Given that I am never sure, I don’t want to have any concentrated bets.”

I love that.

Defining Non-Linearity is a little more complex. But, essentially, that’s the point – and why we’ve built all of our models and processes on Complexity (or Chaos) Theory.

Clients often ask me for reading primers on Chaos Theory. Here are a few:

- “Complexity – The Emerging Science At The Edge of Order and Chaos”, by M. Mitchell Waldrop

- “Deep Simplicity – Bringing Order to Chaos and Complexity”, by John Gribbin

After having consumed both of these books, you’ll realize that neither contain any applied market models. And that, too, is the point. Accepting Uncertainty and Non-Linearity in your risk management process is something that you have to really come to embrace in principle before you apply it to what it is that you do.

In “Future Babble”, Gardner doesn’t do Chaos Theory like I do, per se, but he does simplify the difference between Linear and Non-Linear systems. “Gravity, for example, is linear in mass. Double the mass and you get twice the gravity” (page 39). “A common component of non-linear systems, feedback, involves some element of the system looping back on itself…” (page 40).

I like that explanation because it’s simple. To a degree, Non-Linearity also rhymes with what George Soros calls “reflexivity.” And, again, in principle, it takes a fundamental acceptance that this is what drives market prices, volumes, and volatilities before you can really apply it to what it is that you do.

Back to the Global Macro Grind…

What it is that the US stock market continues to do is go down. Last week, with the SP500 closing at 1123 (its lowest weekly-closing-low of 2011), across all 3 of our core risk management durations (TRADE, TREND, and TAIL), US stocks are bearish/broken:

- TRADE (3 weeks or less): resistance = 1166

- TREND (3 months or more): resistance = 1294

- TAIL (3 years or less) = resistance 1256

When Perma-Bulls call this a correction, I’m not quite sure what they mean.

- Since its 2007 bull market cycle-high of 1565, the SP500 is down -28.2%

- Since its 2011 bear-market rally to a lower-long-term high of 1363, the SP500 is down -17.6%

- For 2011 YTD, the SP500 is down -10.7% (the Russell 2000 is down -16.8%)

Now before the bulls get to point #3 they’ll be jumping out of their seat saying, ‘but, the SP500 is still up +66.1% from its March 2009 closing low.’ OK. It really would be ok if the Perma-Bulls were in 100% Cash at the 2009 low and bought everything for their clients right then and there – but I’m pretty sure that didn’t happen.

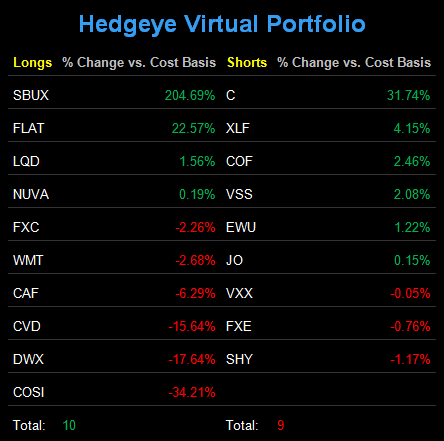

In Q3 of 2008, I took the Hedgeye Asset Allocation Model to 96% Cash.

In Q3 of 2011, I’ve now taken the Hedgeye Asset Allocation Model to 70% Cash (versus 64% at the beginning of last week).

I guess that makes me relatively bullish compared to 2008!

Into Friday’s straight up move in Gold and Silver, I took our Commodities allocation back down to 0% (I sold our entire Silver (SLV) position). There are no rules against buying that or a long position in Gold back. Long-term returns are cumulative and gains compound. The market doesn’t particularly care what I own on any particular day.

Making money starts with not losing money. And while I am painfully aware of how hard it is to actually execute on that strategy at the end of bear market rallies (2007 and 2011), I’m also very respectful that long-term returns in this business are both Non-Linear and Uncertain.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, 79.84-84.69, and 1108-1166, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer