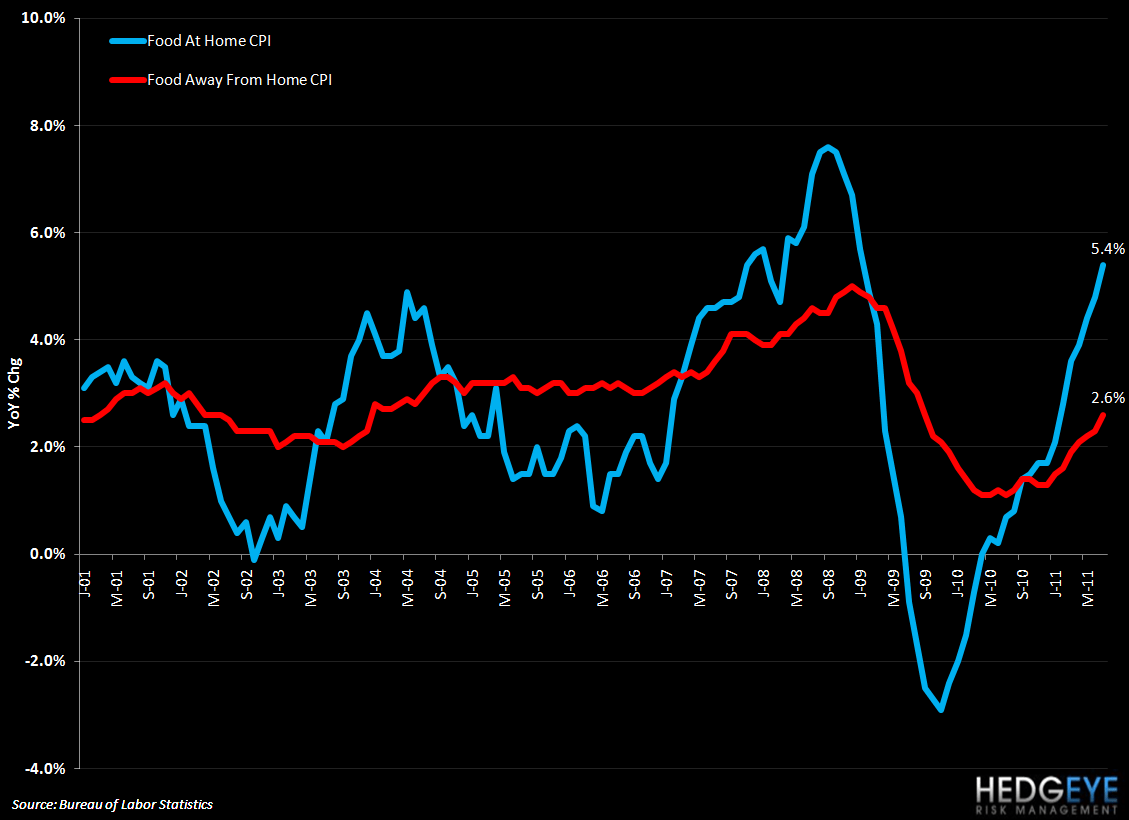

Inflation in the grocery aisle continues to outstrip price increases at restaurants, the latest CPI data for July indicates. It seems logical that restaurants may be gaining some benefit in terms of traffic as grocers have moved first (and aggressively) in hiking prices to protect margins.

From WMT’s commentary during its 8/16 earnings call, it seems that grocers’ customers are managing their checks quite closely: “While we saw an increase in grocery inflation of approximately 3.5% during the quarter, customers remain under continued pressure and are trading down to lower price points and smaller pack sizes, as well as opting out of discretionary purchases. As a result, we're seeing minimal pass-through of inflation to sales. Food inflation has replaced gasoline price as the most important household expense concern.” Food inflation, according to WMT, has become the most important household expense concern.

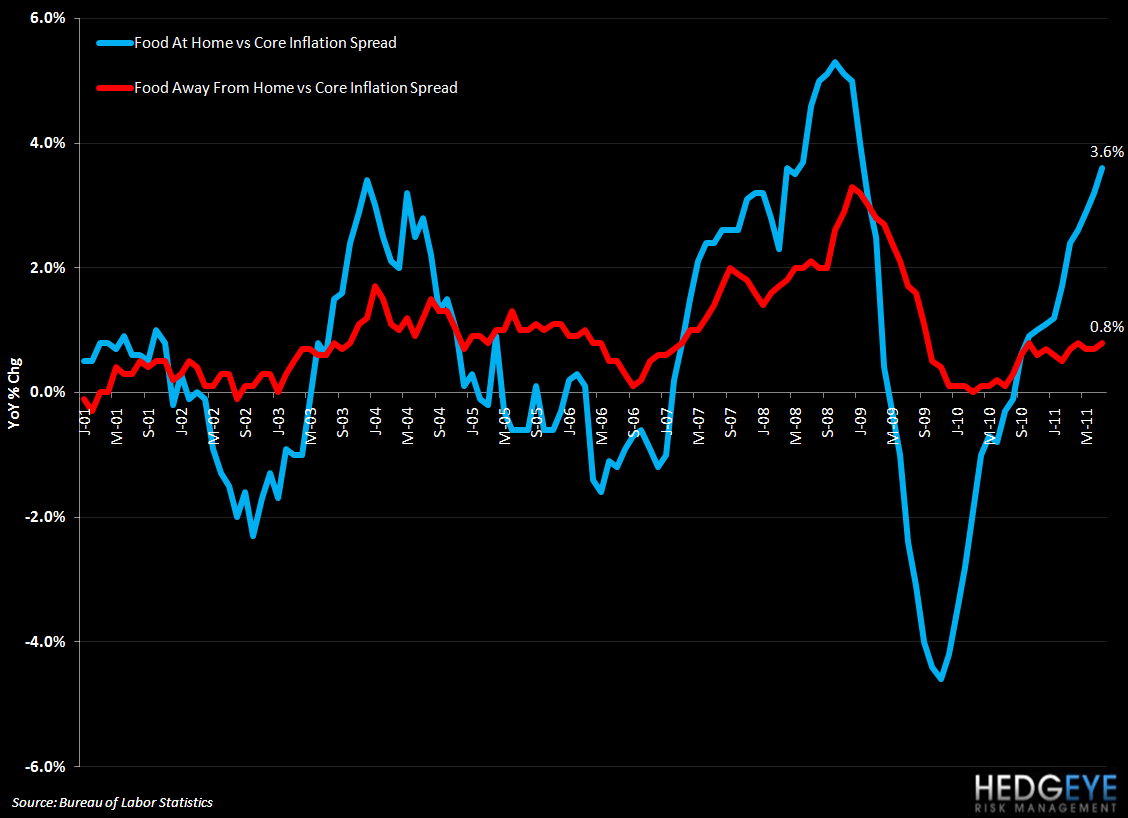

The first chart below shows the significant difference between Food at Home CPI and Food Away From Home CPI. The second chart shows the difference between the year-over-year growth of these respective indices and Core CPI growth. The spread between Food Away From Home CPI growth and Core CPI growth has been fairly constant over the last few months. The spread between Food at Home CPI growth and Core CPI growth, however, has been widening as suppliers and, in turn, grocers react to margin pressure.

Howard Penney

Managing Director

Rory Green

Analyst