Conclusion: Recent changes to China’s convoluted system of capital controls are structurally bullish for the Chiense yuan and may serve to provide some reprieve for washed-out Chinese financials. Moreover, Thailand’s decision to implement a rice price-fixing scheme later in the year is yet another inflationary headwind for the region.

Positions in Asia: Long Chinese equities (CAF); Short Japanese equities (EWJ).

China’s Ever-Relaxing Capital Controls

Overnight, Chinese officials announced three measures to spur cross-border yuan investment. Though not wholly original or earth-shattering, the cumulative impact of each additional measure inches the Chinese yuan one step closer to becoming a dominant currency in the international FX market. The measures include: a Hong Kong equity ETF vehicle for mainland investors, a $3.1B extension of the Qualified Foreign Institutional Investor Program (QFII), and a general relaxation of controls in the dim-sum bond market.

The ETF vehicle is designed to give mainland investors access to stocks listed in Hong Kong. The scheme resembles to the 2007 “through train” plan, which would’ve allowed investors direct access to Hong Kong equities (scrapped for a less aggressive plan in Jan ’10). Back then, the announcement combined with a global love interest with all things “Chinerr” help push the Hang Seng Index to a record high. We don’t see a similar effect occurring this time around, as the gap in valuation between the traditionally cheaper Hang Seng stocks and Shanghai Composite stocks is rather minimal today (1.1x) vs. a 2007 peak of (17.9x), limiting the cross-border appeal based on the potential for arbitrage.

The QFII extension grants foreign institutional investors a quota of up to 20B yuan ($3.1B) to make initial investments in mainland Chinese securities. The program was initially introduced in 2002 as a way to grant foreign institutional investors greater access to Chinese domestic stock markets in a bid to secure funds amid a major recapitalization of the Chinese banking system. Should Chinese banks ultimately require recapitalization within the backdrop of property market worries and local government financing vehicle debt, this makes the process a bit more liquid in our opinion. We expect demand for Chinese bank assets to grow from current trough levels as the liabilities associated with BAC, U.S. Housing Headwinds, and Europe’s Sovereign Debt Dichotomy come home to roost.

Lastly, China’s decision to expand the scope of mainland corporations’ offshore yuan-denominated debt (“dim-sum bonds”) issuance is another method by which foreign investors can gain incremental access to China’s closed capital structure. Moreover, we see it as another avenue by which Chinese banks could tap previously limited pools of capital. For instance, the 554B yuan ($85.3B) in Hong Kong based yuan deposits has been limited to collecting negative real deposit rates (nominal short-term rates are roughly 25bps on average) due to limits on cross-border yuan transactions. Now, foreign investors can take increasing advantage of dim-sum bond issuance, like today’s Ministry of Finance 20B yuan issue – the third-largest offering on record. As more and more companies issue debt in this market, we expect cross-border yield differentials to converge from distorted spreads like the current 157bps gap on 10yr Chinese sovereign debt.

Net-net, we continue to see structural upward pressure on the Chinese yuan as China continues to open up its capital markets. While our belief that the Chinese yuan will eventually take major share of global FX reserves has many years to run its course, we do like such incremental efforts, as they remind us that China is indeed committed to strengthening its currency over the long term. Though Chuck Schumer (D-NY) may not be around long enough to see this play out, we can assure you that it’s better for the global economy he doesn’t have his way too quickly. The +14% YoY rate of U.S. import price growth is a painful reminder that China accounts for 10.1% of global exports – i.e. the faster the yuan appreciates vs. the USD, the more U.S. consumers and corporations have to take The Inflation in the margin over the short-to-intermediate term.

All told, we strongly maintain our bullish bias for countries that maintain a strong “handshake” via policies that support currency strength, as opposed to the debt, deficit, and devaluation strategies currently being implemented from Washington D.C. to Brussels.

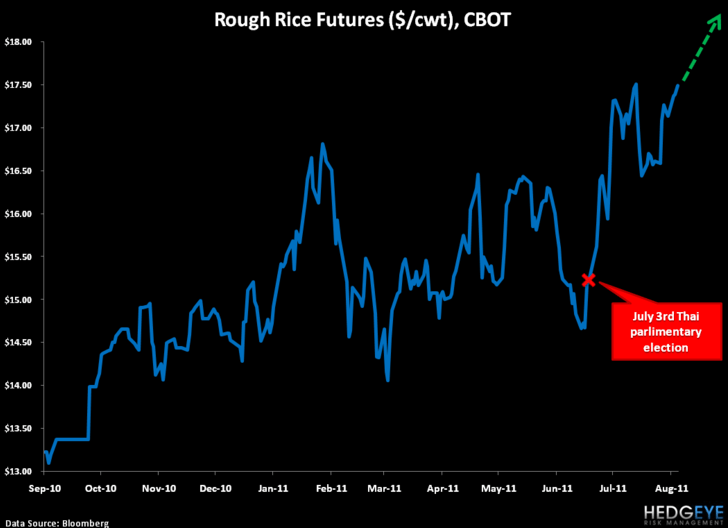

Thailand’s Going to Strong-Arm the Global Rice Market – Inflationary for the Region

Today, Thailand’s newly elected prime minister Yingluck Shinawatra confirmed that her government will fulfill a campaign promise to purchase (and hoard) unmilled rice at 15,000 ($502) baht per ton in the November harvest – an increase of +51.5% from the current market rate of 9,900 baht per ton.

The scheme is designed explicitly to sustainably push up global rice prices by reducing supply on the global rice market (per the USDA, Thailand is the world’s number one rice supplier at roughly 32.2% of total exports). This confirmed by recent comments out of Pheu Thai politician Pichai Naripthaphan, former deputy finance minister for Yingluck’s older brother, Thaksin Shinawatra – the former prime minister of Thailand: “It makes no sense that every agricultural product in the world has gone up except for rice… This is our key policy to win votes, not only this time but in every election.” The Pheu Thai party is indeed serious about buying votes from the agricultural base and there are many for sale in Thailand, with a total of 23.5 million farmers or 35% of the population, per Thailand’s Office of Agricultural Economics.

Asia, which accounts for roughly 87% of global rice consumption, is particularly at risk from a food inflation perspective. Initially, countries may elect to cancel Thai orders and curb exports of their own production, but seeing how rice is the staple of Asian diets, we don’t see much of a way around this over the long term – rice prices are going up as global supply is constrained as a result of the Thai government’s policy to first stockpile the grain and then negotiate export quantities on a country-by-country basis. It’s worth noting that food has an average weighting of over 30% of inflation indexes throughout Asia, with rice obviously being a large component of that (per Rabobank Groep NV).

Back in 2008, a similar scheme was introduced by Thaksin, which ultimately saw the purchase of 5.4 million tons of the grain by the Thai government from over 700,000 domestic farmers, leading to record domestic stockpiles (6.1 million tons) and record prices in Thailand's domestic and export markets (17,000 baht and $1,038 per ton, respectively). According to Thailand’s Rice Exporters Association, current Thai export prices are roughly $582 per ton (up +22% YoY), so an increase to levels reached under the previous scheme would imply a near doubling of export prices from today’s levels.

Such an occurrence would obviously have an inflationary impact across the region due to Thailand’s sheer weight in the global rice market. This is an incremental risk to Asian inflation readings as we look forward into 2012 and beyond, and may ultimately limit the amount of monetary easing Asian central banks can pursue in the event the current global economic slowdown takes a turn for the worse. Asian central banks have hiked rates 44 times since March of 2010 and Thai’s rice price-fixing scheme is likely to make it difficult, on the margin, for them to unwind these tightening measures when they perhaps need to.

Darius Dale

Analyst