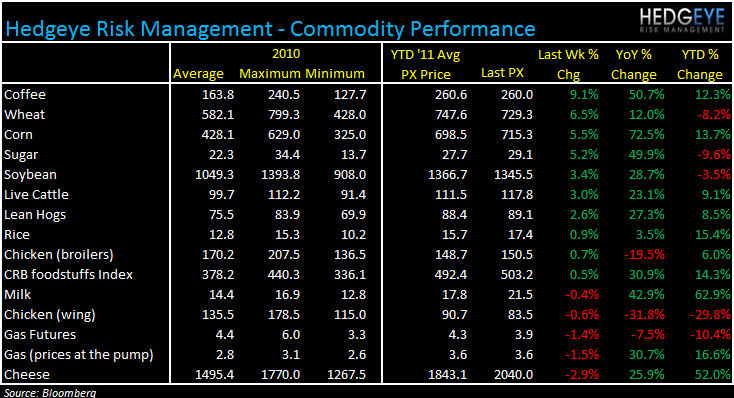

Commodities moved higher, week-over-week, supported by fundamentals and the decline in the dollar. Even dairy, which moved lower week-over-week, is near peak levels and likely concerning those companies with un-hedged exposure.

Summary

Commodity markets are certainly not showing much in the way of price stability recently. While coffee, Wheat, and corn prices gained 9.1%, 6.5%, and 5.5%, respectively, cheese prices fell 2.9%. The dollar declined over the week and commodities duly went higher. The inverse occurred last week, which is not surprising given the -0.88 inverse correlation between the CRB Foodstuffs Index and the USD (one year of data). Cheese prices have come down week-over-week but remain higher than the level reached during the spike in prices in 1Q11. We believe CAKE’s stance on dairy costs has not been cautious enough and the fundamentals and – most importantly – the price supports our view more as time passes.

Coffee

Coffee is hitting the headlines at the moment as J.M. Smucker is cutting prices by an average of 6% nationwide and other players in the space, including SBUX, are being questioned about a possible reduction in prices after a series of price hikes over the last year.

From a supply perspective, much of the news flow over the past week was bearish for prices given that Brazil’s frost season is coming to an end, India’s Minister for Commerce and Industry stated in parliament that coffee production in that country will increase 6.7% year-over-year in 2012, and longer-term supply dynamics are strong.

From a demand perspective, it seems that demand will continue to grow over the long term. According to a source, cited by Bloomberg, in the Uganda Coffee Development Authority, the increase in demand for coffee will come from Brazil, India, Indonesia, Mexico, and Costa Rica. However, the consensus seems to be that a “coffee surplus” will weigh on prices in the back half of 2011 and into 2012. As recent weeks and months have dictated, however, the dollar will continue to be a key driver of coffee prices.

Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls and/or media reports.

PEET (8/2/11): “As we indicated, in our first quarter call, we had to buy a small amount of our calendar 2011 coffee beans at significantly higher prices and this coffee will roll into our P&L during the third and fourth quarter.”

“Higher priced coffee resulted in gross margins this quarter being 290 basis points below prior year. In our first quarter conference call, we indicated that in addition to the overall higher price coffee market, we had to buy a small amount of coffee this year at significantly higher prices. And as a result, we expected our coffee cost to be 40% higher in fiscal 2011.”

HEDGEYE: Peet’s is a company with a very competent management team that manages coffee costs extremely well. Its higher-end, loyal customer base makes the price elasticity of demand more inelastic than for other coffee concepts’ products.

SBUX (7/28/11): “As I mentioned earlier, are absolutely a headwind for us in the full business and that's most acutely impactful on margins in CPG as it's a much more coffee intensive cost structure, as you know. I can tell you that the decline as I spoke about it earlier from about 30% operating margin in CPG this year down to the target 25% next year is really all explained by commodities. Absent commodity inflation we'd be at or improving our margin in the coming year.”

“As we had anticipated, in recent weeks, coffee prices have retreated significantly from a high of more than $3 per pound just a couple of months ago to levels now near $2.40 per pound. As prices have been falling we continue locking up our needs for fiscal '12 and now have virtually the full year price protected.”

HEDGEYE: Starbucks is aligning itself with the right partners to gain more control of its coffee costs to provide investors with more certainty going forward and to protect its margins as global coffee demand continues to rise.

GMCR (7/27/2011): “However, what we've said is that should coffee prices or other material costs spike, we will certainly consider price increases as necessary. We certainly hope that we do not have to cover one again next year. But our objective long-term is attempting to maintain our gross margin as we would see input costs come along.”

HEDGEYE: GMCR hedges out 6-9 months in advance. Without a rising dollar and some stronger supply growth to counteract growing global demand, we expect sustained elevated prices.

Jones Coffee Roasters – a local producer that sells to retailers like WFM (8/17/11): “We’re thinking about not doing the last [of three prior planned] increase because the market’s going back down”.

HEDGEYE: Coffee consumers have certainly noticed price increases over the last year, such as SBUX raising prices in its packaged coffee by 17% in May, and there will be pressure on retailers in stores and in the aisle to adjust prices if input costs do continue to come down. Yesterday, SBUX CEO Howard Schultz said that he is looking at ways of lowering prices.

Corn/Wheat

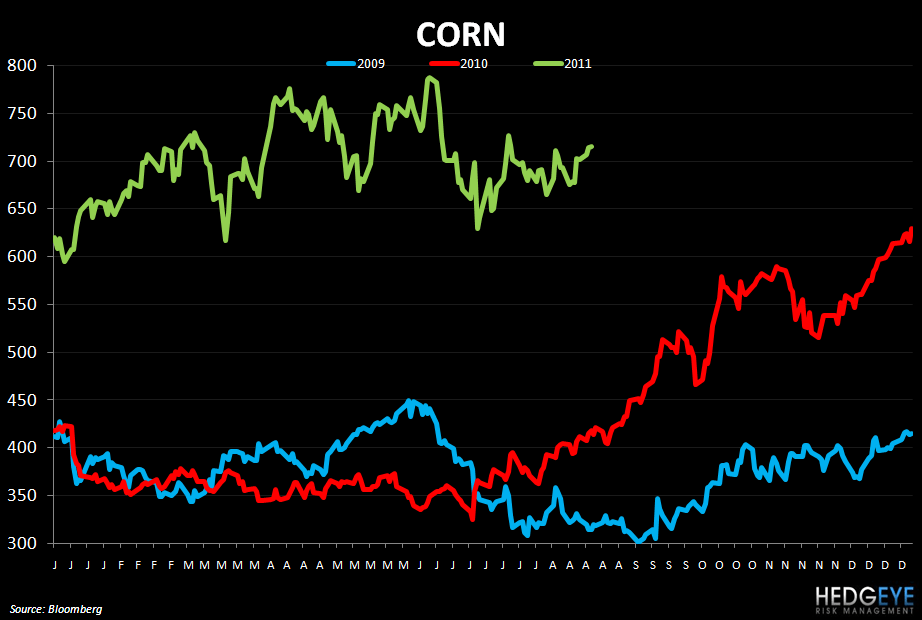

Corn and wheat prices gained 5.5% and 6.5%, respectively, over the last week as the dollar moved higher. From a supply and demand perspective, the vast majority of the data points seem to be supportive of elevated prices. After poor yields during the growing season, the poor prospects for planting now seem to be compounding the problem. In the US, the severe drought in Texas, Oklahoma, and southern Kansas will possibly cut acreage of winter crops set to be planted next month. Specific to wheat, the USDA said today that the output of hard, red-winter wheat, grown primarily in the Great Plains, may drop 22% to 794.4 million bushels from last year due to the persistence of dry weather since late 2010.

Going forward, we will be watching corn yields in August closely as TSN management said on the 8thof this month that “the month of August, as we saw last year, is very important in the crop’s yield”. How the standing crop of corn shakes out will be a significant factor in determining the fundamentals for protein costs into 2012.

Wheat has increased less on a year-over-year basis than corn as we lap weather events and the impact of Russia lifting its grain export ban, enacted in the wake of drought and fire depleting crops in the country in 2010.

Below is a selection of comments from management teams pertaining to grain prices from recent earnings calls.

AFCE (5/26/11): “On a full year basis, we now expect the Popeye’s system will experience an increase of 4% to 5% in food costs. This is up from our previous guidance of a 2% to 3% increase, primarily due to higher commodity costs in corn and soy, which impacts our bone-in chicken, as well as increases in the cost of flour and cooking oil.”

HEDGEYE: Corn costs going higher are going to squeeze margins for food processors and, in turn, their clients. The food processor space as been depressed for some time, on a relative price performance basis, and any improvement in their margin outlook could bring strong stock performance in that space. For now, though, the input cost outlook is not positive.

PNRA (7/27/11): “Just to note on the cost of wheat, in 2011 overall, the per-bushel cost will be about the same as 2010 due to our laddering purchasing strategy.”

“We are going to take price in the fourth quarter. This price will offset dollar for dollar the per-bushel inflation of wheat of approximately $3 a quarter that we're going to see in the fourth quarter of this year and then across next year”

“We do continue to expect significant inflationary pressures in 2012, 4% to 5% food inflation, $10 million of unfavorability on wheat costs, which means that we don't expect operating margin much better than flat to full-year 2011 in 2012.”

HEDGEYE: It seems probable that wheat costs are going to remain elevated and PNRA’s earnings will not be helped by any decline in wheat prices.

DPZ (7/26/11): “We're fairly locked in on our chicken, locked in on our wheat into – partway into next year.”

PZZA (8/4/11): “We're actually covered through Q1 from a contract standpoint. So from a supply chain disruption or even significant price impact we don't anticipate anything between now and the end of the year.”

Cheese

Cheese prices are extremely elevated at the moment. This caused DPZ to raise guidance for its full year 2011 food basket inflation to 4.5%-6% from 3%-5%. CAKE has not followed suit, despite that target previously being predicated on softening dairy costs – which the company does not have hedged – in the fourth quarter. Looking at the chart below, the company’s stance on inflation is becoming more and more tenuous.

Increasing demand from emerging markets (like China’s growing penchant for pizza, apparently) and shrinking herd sizes are providing tailwinds for dairy prices.

Below is a selection of comments from management teams pertaining to cheese prices from recent earnings calls.

CAKE: (7/20/11): “We continue to believe that food costs will moderate on a comparative basis in the fourth quarter, and expect total cost of sales to be 35 basis points to 55 basis points lower in the fourth quarter of 2011 versus the prior-year period.”

HEDGEYE: We think that management is being aggressive in assuming inflation this benign given the trajectory of dairy prices. The company is taking price this summer and also planning on increasing efficiencies through $3-5 million in planned cost savings to offset the inflation it is seeing but we still believe that the food cost forecast assumption is aggressive.

JACK (8/11/11): “Cheese accounts for about 6% of our spend and we continue to expect a 13% increase for the year. We have 100% coverage on cheese through the remainder of the fiscal year. Additionally, we have more than 50% of our spend for cheese covered for fiscal year 2012.”

DPZ (7.26.11): “Given higher than originally anticipated cheese prices, we currently expect our overall market basket for 2011 will increase by 4.5% to 6% over 2010 levels. This was up from our previously communicated range of 3% to 5%.”

HEDGEYE: Last week we highlighted the fact that DPZ’s last earnings call took place during a trough in cheese prices and we expected a change in tone from the commentary in early May. CAKE is likely, in our view, to make the same transition in tone at some point this year.

Howard Penney

Managing Director

Rory Green

Analyst