Keith shorted PNK in the Hedgeye Virtual Portfolio. In addition to a lousy quantitative setup, PNK looks to be in a difficult spot in a deteriorating macro environment.

Keith shorted PNK in the Hedgeye Virtual Portfolio at $12.49. According to his model, TRADE resistance is only 2% above where he shorted it and TRADE support is 18% below. While Keith is bearish on PNK from a technical perspective, the macro environment could cause some problems for PNK and investor sentiment surrounding the name. If the Hedgeye macro view comes to fruition - stagflation - domestic gaming will come under pressure. Gaming has proven to be an incredibly cyclical industry. Sentiment could turn worse for PNK as it is the only domestic gaming company that is not in a deleveraging mode and not generating free cash flow. That opens the stock up to a higher degree of multiple compression.

PNK has been a great story - we've been a big cheerleader - as management has done a terrific job with margin expansion. With success, however, comes higher expectations. Full year Street estimates are finally appearing reasonable rather than ridiculously low so the catalyst of continued quarterly blowouts may be behind the company (6 in a row). With consumers struggling and 2H regional gaming trends already disappointing here in July, we struggle to find a positive catalyst.

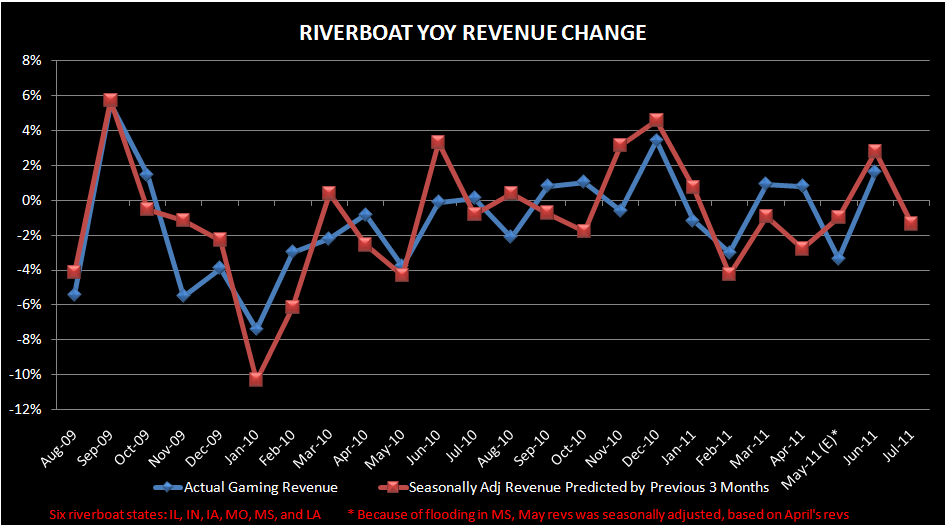

Now, PNK had a pretty good july due in part to high table hold but domestic gaming revenue trends overall have already been disappointing. As shown below, we estimate July gaming revenue in the mature regional gaming markets (aka riverboat markets) should decline slightly more than 1%. We look at monthly sequential revenue based on the previous 3 months, adjusted by a historical seasonality factor. Most of the riverboat states that have reported for July have posted same-store gaming revenues below our model, which would indicate sequential revenues have slowed.