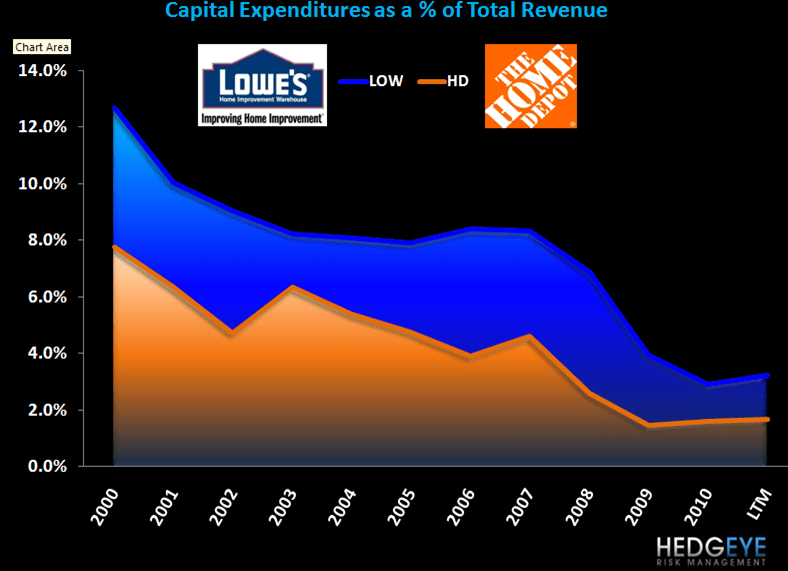

Yeah yeah…we all know the differences in the comp spread and relative operating performance. The market knows that too. But LOW will not roll over and play dead. There’s no doubt it is having execution issues and is losing share to Depot as HD focuses heavily on its core. But HD was a year early (2009/10) in reaccelerating both store level capex and SG&A per square foot. Now it is benefitting. LOW’s uptick in investment spending over the past 12 months during a time of weakness in its business (and botched execution) has been particularly painful. Bigger picture, we like this space given the catch-up in deferred maintenance as the housing market continues to suffer. Would we buy either today? No. But the relative trajectory in revenue and margins is likely to turn in LOW’s favor over the next six months. On weakness, that’s where we’d look first.

<