This note was originally published at 8am on August 11, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Weather forecast for tonight: dark.”

-George Carlin

When 2011 is all said and done, we’ll separate the winners in this Globally Interconnected Game from the whiners. Whoever had their growth estimates right will have had a lot of other things right.

In the meantime, we’ll have to deal with politicians, journalists, and bankers obfuscating this very simple fact – Global Growth Has Been Slowing Since The End of 2010.

That’s it. That’s what Wall Street, Washington, SocGen, and the Government of France all have in common this morning – their top-line estimates for GDP Growth are still way wrong. And, as a result, being long any of their conflicted promises that are associated with using the wrong GDP assumptions will continue to be wrong. Markets don’t lie; politicians do – and the market has this right.

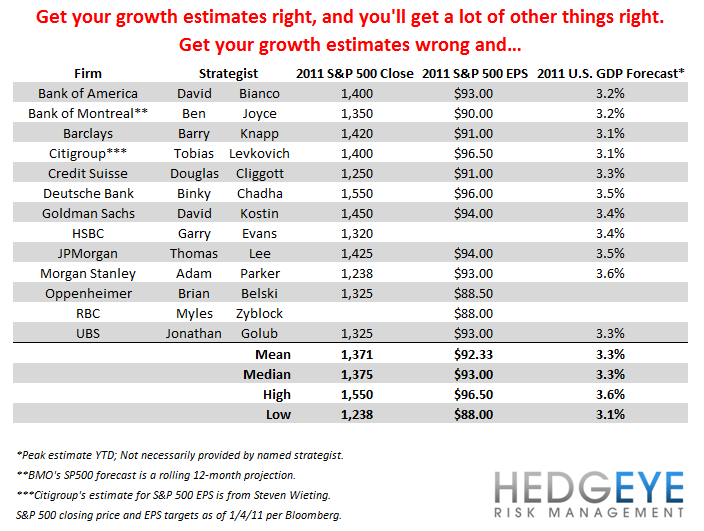

Markets don’t trade on politicians, journalists, and bankers using the wrong sources – they trade on expectations. To amplify this point about Growth Expectations, let’s take a step back and review where these “blue chip” forecasters were on these matters in Q1 of 2011:

Forecasts for 2011 US GDP Growth:

- Bank of America = 3.2%

- Barclays = 3.1%

- Citigroup = 3.1%

*Disclaimer: these estimates must have all been based on the exact same Keynesian model for garden variety “recovery”

Forecasts for 2011 SP500 Returns:

- Bank of America (David Bianco) = 1400 (up +11.4%)

- Barclays (Barry Knapp) = 1420 (up +13.0%)

- Citigroup (Tobias Levkovich) = 1400 (up +11.4%)

*Disclaimer: two of these forecasting czars opted for round numbers on the absolute; one opted for the rounded off % return

2011 Reported Numbers (Year-To-Date):

- US GDP Growth Q1 2011 = 0.36%

- US GDP Growth Q2 2011 = 1.29%

- SP500 YTD Return = DOWN -10.9%

3 investment banks with conflicted analysis + 3 train wrecks versus expectations = priceless.

Actually, that’s not fair – there is a price to pay for Wall Street/Washington groupthink. It’s being marked-to-market in every American’s 301k each and every day. While I’ll be the first to admit that this is not 2008 (it’s 2011), all it took to remind me how bad Wall Street’s forecasting models remain at calling growth slowdowns was another growth slowdown!

There isn’t really a trickle-down effect associated with getting growth estimates this wrong – it’s more like a waterfall. To borrow a frightening quote from Bank of America’s CEO, Brian Moynihan, on yesterday’s conference call, “think about it this way and you’ll have to trust us”:

- COUNTRIES – when they are wrong on GDP assumptions, they are wrong on their DEFICIT/GDP assumptions.

- RATINGS AGENCIES – when they see countries with DEFICIT/GDP assumptions rising, their ratings start falling (on a lag)

- BANKS – when their GDP assumptions are wrong, their assumptions for their net interest margins and cash flows are wrong

That last point is less clear to your average journalist attempting to “trust” Brian Moynihan on the numbers. What does it mean?

- Banks make money on a spread (the Yield Spread – that’s why La Bernank wants to keep rates of return on your savings low)

- When growth slows, the Yield Spread compresses (the 10s/2s spread has compressed by 28% in the last 6 months)

- When the Yield Spread compresses, Bank of America, Barclays, and Citigroups NIM (net interest margin) and cash flow declines

So… if you get that… and you’re still using Hedgeye’s GDP estimates for 2011 instead of a conflicted and compromised Street’s… you would have immediately recognized anything coming out of SocGen, the Government of France, or Bank of America’s mouths yesterday as irrelevant and/or wrong.

I continue to forecast that the sun will rise in the East today.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1684-1794, $77.20-88.29, and 1087-1137, respectively. We bought Goldman Sachs yesterday in the Hedgeye Portfolio and we remain short Citigroup.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer