“They get to see all of my mistakes.”

-Ray Dalio (The New Yorker, July 25th, 2011)

Recent history is marked-to-market. That’s a good thing because it helps us rethink, rework, and learn faster. Modern day multi-media tools from YouTube to Twitter have revolutionized and expedited our quest to find the right sources of alpha. Old Wall Street’s “sources” are either wearing orange jump suits or dying on opacity’s vine.

Per the same New Yorker article that I cited yesterday (“The Machine – How Ray Dalio built the world’s richest and strangest hedge fund”, by John Cassidy at The New Yorker), Ray Dalio has a “rule of radical transparency” that has ultimately shaped the risk management culture at Bridgewater Associates.

Transparency: I like that word; particularly when someone is practicing it out loud.

As a practical matter, I do find it very interesting (but not ironic) to note that two of the most successful Global Macro Risk Managers of our generation (George Soros and Ray Dalio) both started their firms during the mid-1970s. Soros and Dalio hung up their own shingles in 1973 and 1974, respectfully.

What was very unique about the 1970s was that there was this economic reality called The Stagflation. It was man-made by central planners and, ultimately, it ran all of the Keynesians right over. Big Government Interventions that were focused on devaluing the US Dollar perpetuated rising inflation and slowing growth (stagflation).

I’m not sure how either Soros or Dalio’s macro models scored The Stagflation then, but this is how Hedgeye scores it now:

- Growth Slowing At An Accelerating Rate

- Inflation Rising (and remaining) Above The Real Growth Rate

- Monetary and Fiscal Policy that perpetuates 1 and 2

The Stagflation: In the US and across most of Western Europe, that’s basically what you have right here and now. In fact, if you take the US Government’s word for it and use the Q1 2011 US GDP number (revised down by 81% to 0.36%), and then “trust” that headline Consumer Price Inflation was 3.3% in Q1 - that’s a ratio of 10:1 of inflation over growth. That’s nasty.

Causality? What drives The Stagflation? That’s easy. Keynesian Politicians.

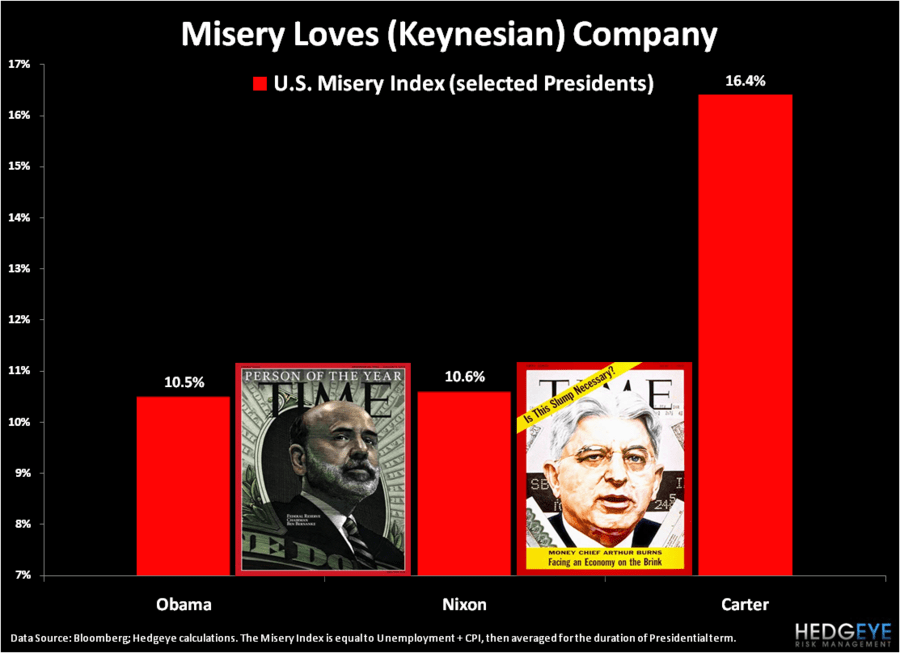

This is what Nixon, Carter, Bush II, and Obama all had/have in common. They and their economic “advisors” were/are all Keynesians. And all 4 of their Administrations oversaw horrible employment decades combined with horrifically low Presidential approval ratings.

Today, this country doesn’t like The Stagflation any more than it didn’t in the 1970s. Back then, they called it the Misery Index (unemployment + inflation). On this very common sense calculation, the Obama Administration ranks 3rd worst in American history to Nixon and Carter. Not surprisingly, Reagan, Clinton, and Kennedy are the Top 3.

Back to the Global Macro Grind…

Let’s take a ride around the world and take a gander at some stagflation callouts from this week’s Global Macro Economic Data:

- JAPAN – reports a down -1.3% GDP number for Q2 2011. Keynesians celebrated that as “better than expected due to the tsunami effects.” Non-Keynesians remind realists that Japan’s GDP was negative for the 6 months before the tsunami!

- UNITED KINGDOM – reports an awfully high Consumer Price Inflation (CPI) print for July of +4.4% (versus +4.2% in June); the British (homeland of the Keynesians) are now running 10:1 inflation over GDP growth like the Americans are.

- GERMANY – reports a huge sequential slowdown in economic growth for Q2 2011 of +2.8% (cut in half versus Q1 GDP growth of +5.2%). If you didn’t know why German stocks have crashed since May 2011 (down -22%), now you know.

Elsewhere in Global Macro, commodities, currencies, and bond markets continue to signal that Global Growth Slowing remains reality:

- CRB COMMODITIES INDEX – closed at 330 yesterday and remains well below Hedgeye’s intermediate-term TREND line of 348

- WTIC OIL – trading $86 this morning continues to be broken across all 3 of our risk management durations (TRADE/TREND/TAIL)

- DR. COPPER – leads to the downside this morning (down -1.3%) and has now broken its long-term TAIL line of support ($4.10/lb)

- EUR/USD – continues to hope and pray to hold above its intermediate-term TREND line of resistance = $1.44

- UST YIELDS – 10-year yields remain broken across all 3 of our risk management durations (downside support = 2.06%!)

- UST YIELD SPREAD – continues to compress (10s minus 2s = +209 basis points) and is down -25% since Q1 Growth Slowed

But, but…

There are no buts. Stocks aren’t “cheap” either. Our 2011 call on US Equities has not been that stocks will get as cheap as they did during The Stagflation of 1974 (7x earnings). But it has been that buying Equities as Growth Slows And Inflation Accelerates is Misery’s Mistake.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $79.10-91.79, and 1098-1256, respectively. Yesterday I bought Silver (SLV) and sold half of our long China (CAF) position in the Hedgeye Asset Allocation Model, taking my allocation to International Equities down to 6% and keeping my allocation to US and European Equities at 0%.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer