“Pain + Reflection = Progress.”

-Ray Dalio

That’s a quote from what I thought was one of the best asset management articles of the year – “Mastering The Machine – How Ray Dalio built the world’s richest and strangest hedge fund”, by John Cassidy at The New Yorker.

What was fascinating to me about Dalio’s Global Macro Risk Mangement Process is that there was nothing that was strange to me about it at all. It made perfect sense. Maybe that’s why he’s been one of the few major Hedge Fund managers who has been able to navigate the Big Water of both 2008 and 2011, generating positive absolute returns. Evidently, his process is repeatable.

Ray Dalio’s Bridgewater and Big Water are two very different things. Big Water is what some of my closest friends and I just spent the last 3 days conquering in Hells Canyon – America’s deepest river gorge.

No roads cross Hells Canyon. There are no government people on the shores to bail you out. You are either listening very carefully to your guide or you aren’t coming out.

“Who Is John Gault?” Maybe a better question for me over the course of the weekend was, “Who Is Jeff Smith?” The man who called it “River Time”, was constantly reminding us that “safety is no accident.” Evidently, he was right.

I’ll be flying home, safely, from Boise, Idaho this morning.

Back to the Global Macro Grind…

Learning from mistakes (PAIN) and rethinking those mistakes (REFLECTION) = PROGRESS.

With all of the lessons learned about Growth Slowing in 2008 and how politicians and central planners are infused into your said “free” markets to arrest gravity (“shock and awe” interest rate cuts demanded then; Quantitative Easing begged for now), we are reminded of the 2 things that Big Government Interventions do to our markets and economies:

- They shorten economic cycles

- They amplify market volatility

Whoever didn’t pick up on that second point last week obviously wasn’t in the water. There was amplified volatility in The Price Volatility itself. From leftist French ideas about banning short selling to the whatever we have coming down river this week, all of this is reminding investors that markets that can’t see their rules change in the middle of the game are not markets they should trust.

Like staring down the belly of a Class IV white water rapid, when people see this kind of volatility in their retirement accounts they typically opt to get out. While that may be an inconvenient truth for those of us who are brave (or dumb) enough to try our luck trading Big Water volatility, history has proven that markets that lose people’s trust lose fund flows.

When the flows stop, bigger rocks appear…

With our own money at least, we don’t like volunteering to be “fully invested” when GDP Growth is heading towards big rocks (PAIN). History (REFLECTION) may not be precise in helping you navigate the price volatility associated with economic slowdowns – and sometimes the biggest rocks are the last ones you’ll ever see – but the rhythm of this globally interconnected marketplace is a constant reminder.

Going under water can be avoided. Accepting uncertainty = PROGRESS.

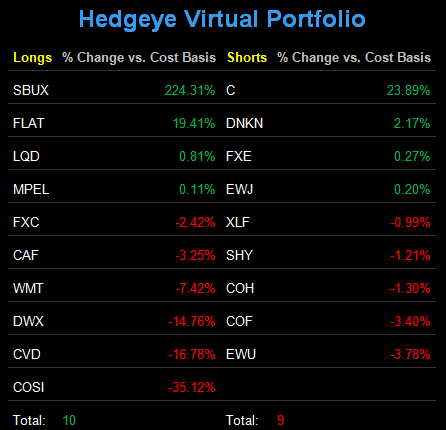

I’ve expressed my acceptance of uncertainty in 2011 by getting out of the water. Last Monday I had a 67% Cash position in the Hedgeye Asset Allocation Model. This morning that Cash position is sitting at 64% and here’s where the rest of my Cash has been allocated:

- Cash = 64%

- Fixed Income = 21% (Long-term Treasuries, Treasury Flattener, Corporate Bonds – TLT, FLAT, LQD)

- International Equities = 9% (China and S&P International Dividend ETF – CAF and DWX)

- International Currencies = 6% (Canadian Dollar – FXC)

- Commodities = 0%

- US Equities = 0%

The only move I made last week was allocating 3% of assets in the model to Corporate Bonds (LQD). They were down hard on the week when I bought them - and I like to buy things when they are red.

The biggest mistake I’ve made in the last few weeks is not being long Gold (GLD). That’s why I have Commodities listed ahead of US Equities this morning. I’d like to buy Gold and/or Silver back on a pullback. Immediate-term TRADE support lines for Gold and Silver are now $1713 and $38.15, respectively. I have intermediate-term TREND upside for Gold and Silver at $1817 and $41.69, respectively.

US stocks were immediate-term TRADE oversold into the close last Monday (see my intraday note from last Monday titled “Short Covering Opportunity”, April 8, 2011), but they are far from oversold this morning. I have immediate-term downside support at a lower-low of 1093 and less than 1% of immediate-term upside from Friday’s closing price, making the risk-reward highly skewed to the downside.

According to Cassidy’s article, Ray Dalio likes to ask his analysts for opinions – but those opinions better be well thought out. “Are you going to answer me knowledgeably or are you going to give me a guess?” he said to his analyst in a meeting.

When at Hedgeye or in The Big Water, we like to be specific on levels – we don’t guess.

My immediate-term support and resistance ranges for the Gold, Oil, and the SP500 are now $1, $78.09-86.06, and 1093-1186, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer