TODAY’S S&P 500 SET-UP - August 11, 2011

As we look at today’s set up for the S&P 500, the range is 93 points or -7.28% downside to 1093 and 0.61% upside to 1186.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 850 (-1752)

- VOLUME: NYSE 1256.14 (-33.25%)

- VIX: 36.36 -6.77% YTD PERFORMANCE: +104.85%

- SPX PUT/CALL RATIO: 1.79 from 1.38 (+29.50%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 28.50

- 3-MONTH T-BILL YIELD: 0.02% -0.01%

- 10-Year: 2.24 from 2.34

- YIELD CURVE: 2.04 from 2.15

MACRO DATA POINTS:

- 8:30 a.m.: NOPA oil, soybean data

- 8:30 a.m.: Empire Manufacturing, est. 0, prior -3.76

- 9 a.m.: Net Long-term TIC Flows, est. $30.1b, prior $23.6b

- 10 a.m.: NAHB Housing Market Index, est. 15, prior 15

- 11 a.m.: Corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $29b 3-mo., $27b 6-mo. bills

- 1:25 p.m.: Fed’s Lockhart speaks in Alabama

- 4 p.m.: Crop conditions: corn, cotton, soybeans, winter wheat

WHAT TO WATCH:

- Transocean offered to buy Norway’s Aker Drilling for $1.4b

- Paulson & Co., Berkshire Hathaway, Pershing Square among those scheduled to release holdings as of June 30 by end of day today

- ConAgra Foods said that Ralcorp Holdings rejected a $5.18b takeover offer within 24 hours and without discussion

- Apple, Google and rival handset and software makers are competing for top patent lawyers as litigation floods courtrooms worldwide.

- Rise of the Planet of the Apes” remained top movie in U.S. and Canadian theaters for second weekend as predicted, totaling $27.5m in ticket sales for News Corp.’s Twentieth Century Fox.

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Hedge Fund Oil Bets Tumble to Eight-Month Low: Energy Markets

- Rice Set to Climb as Thailand Plans Curbs, U.S. Crop Drops

- Funds Slash Commodity Bets by Most in 18 Months on Economy

- Mushrooms Join List of Radiation Threats to Japan’s Food Chain

- Gold Drops for Third Day as Equities Rebound Trims Haven Demand

- Oil Stems Three-Week Decline as Japan Counters Growth Concern

- Ditching Nuclear Risks Third Lost Decade in Japan on Oil

- Sugar to Stay High as China, Indonesia Buy More, ISO Says

- Copper Advances as U.S., Japanese Data Boost Outlook for Demand

- Aluminum Demand in China Set to Double Over Decade, XinRen Says

- Recent Commodities Volatility ‘Unsustainable:’ Citigroup’s Morse

- ConAgra Says Ralcorp Took Less Than a Day to Reject Revised Bid

- Newcrest Has Record Full-Year Profit, Pays Special Dividend

- Crude Climbs as Japanese Economy Contracts Less Than Forecast

- Thai Sugar Production May Fall From a Record in 2011-2012

- Gold May Fall a Third Day in London on Reduced Investor Demand

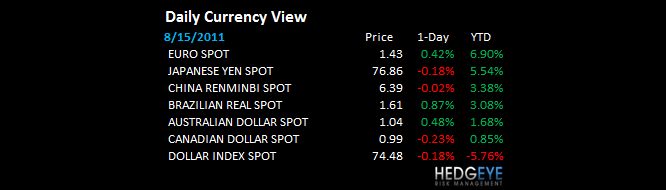

CURRENCIES

EUROPEAN MARKETS

- Low quality rally in Europe with the important markets like Germany are underperforming.

- UK Aug house price index (2.1%) m/m, (0.3%) y/y the first annual fall since Sep 2009 -- Rightmove

ASIAN MARKETS

- ASIA: India and Korea are closed - generally rally was on low volume to lower highs; China +1.3%; Japan +1.4%; Singapore +0.82%

MIDDLE EAST

Howard Penney

Managing Director