This edition of the macro mixer echoes a theme that I laid out in this morning’s Early Look. I wrote, “If the similarities between 2011 and 2008 are bad, the differences are almost worse.” You might have better luck at guessing whether we are headed for another recession but several catalysts long highlighted by Hedgeye CEO Keith McCullough, including the debt ceiling debate, the US debt downgrade, and consensus expectations becoming overly bullish were certainly pointing to a potential market slowdown. The potential for Recession 2.0 now looms large and consumer confidence data out this morning (the worse University of Michigan reading since 1980!) is not encouraging.

Some of the differences between 2008 and today seem worse than the similarities: joblessness is higher, more people are reliant on food stamps for sustenance, and the financial crisis threatening to wreak havoc on our economy is not here in the USA and therefore less within our government’s control. The similarities, given that we are comparing the present situation to crisis of 2008, are inherently negative. Gas prices are elevated, the VIX is spiking, stocks have fallen off a cliff, and consumer confidence is depressed.

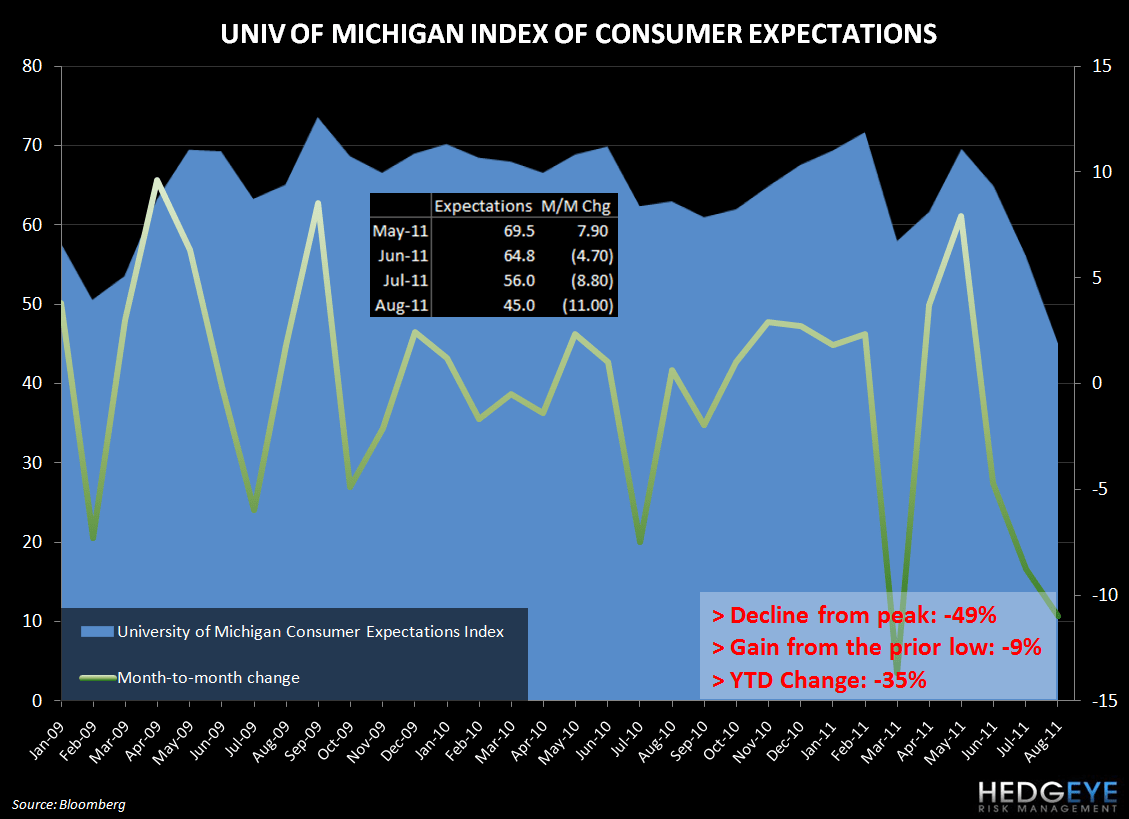

The last point on consumer sentiment being is the most relevant today, with the University of Michigan index plunging in early August. Today, confidence fell 8.8 points to 54.9 versus 63.7 in July. The index has fallen 19.4 since May 2011 and the magnitude of the decline has been exceeded only twice in the history of the index - fall of 1990 and 2005.

The expectations component led the decline, falling 10.3 points to 45.7 (this is its lowest level since 1980). Assessments of current conditions dropped 6.5 points to 69.3, the lowest level since November 2009.

While this does not bode well for consumer spending in August, today’s retail sales data suggested that sales held up well in the month of July. Retail sales rose 0.5% in July, the largest gain in four months; excluding those and auto dealers, core sales grew 0.3%, down from the upwardly revised 0.5% June figure. Growth was led by miscellaneous retailers, gasoline stations, and electronics and appliance retailers. Sporting goods and hobby stores, department stores, and building supply stores were the primary losers.

Confirming the sluggish consumer environment, total business inventories increased 0.3% in June after a downwardly revised 0.9% in May (previously 1%). The growth was smaller than expected and largely driven by wholesaler inventories, as retail inventories continue to contract. The weaker than expected month is an indication that businesses continue to manage inventories very closely as consumer spending trends are tenuous at best.

Howard Penney

Managing Director