This note was originally published at 8am on August 09, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Empty your mind, be formless, shapeless – like water.”

-Bruce Lee

With stock and commodity markets around the world crashing, let’s review the two things that Fiat Fools who fundamentally believe that they can arrest economic gravity do to markets:

1. They shorten economic cycles

2. They amplify market volatility

So, let’s fire up La Bernank this morning and do some more of that!

C’mon. Really? Europe has its own issues to deal with, but is America that dumb? Americans didn’t stand for Fed Head Arthur Burns and President Jimmy Carter perpetuating economic stagflation in the mid 1970s, and I don’t think they will now.

Wall Street/Washington is not America.

Some asset managers may very well think that’s America. Some are already begging for Bernanke’s bazooka this morning. But they should remember a very important factor in the business of money management – they are managing other people’s money.

Like it did when they were begging for “shock and awe” rate cuts in 2008, other people’s money is crashing, again. So let’s review:

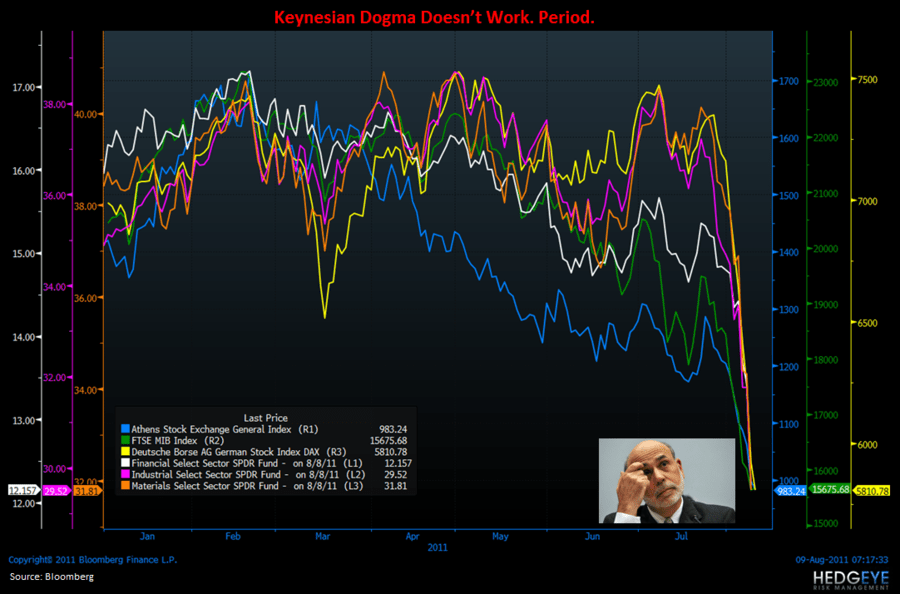

1. EUROPE:

A) Greece is gone – crashed (down -43.9% since FEB 2011)

B) Italy, crashing - MIB Index down -34.6% since FEB 2011

C) Germany, crashing – DAX down -25.6% since May 2nd(and that’s the healthiest European economy!)

2. USA:

A) Financials (XLF) – crashed (down 29.2% since FEB 2011)

B) Industrials (XLI) – crashed (down -23.7% since APR 2011)

C) Basic Materials (XLB) – crashed (down -22.2% since APR 2011)

Now what does the end of April and early May 2011 have in common with both German and most US stocks putting in lower long-term highs versus the 2007 bubble peaks?

Ah, oui, oui, mes amis – c’est La Bernank!

Let’s not forget that April 2011 was the date whereby Ben Bernanke one-upped his own record setting precedent pace, debauched the US Dollar to all-time lows (post Nixon 1971, post Gold Standard), and held the Fed’s 1stever Global Press Conference On Money Printing.

Nice Trade… until it blew everyone up who was chasing yield.

What about the long-term TAIL risk associated with the gargantuan Fiat Fool Experiment that Bernanke’s Princeton buddy Paul Krugman encouraged the Japanese to engage in before locking themselves in the Keynesian death grip of GROWTH SLOWING?

Since 1992, Japan’s average annual GDP Growth has been 0.85%. And while that’s actually better than what Bernanke produced in Q1 of 2011 (0.36% US GDP Growth), that’s still not good.

On top of its debt and deficit problems… America, now we have a GROWTH problem. And if we think we are going to solve it by printing moneys and begging for La Bernank, we deserve to keep crashing.

Back to the Global Macro Grind…

Whether we are going to thank them for making up their numbers like we do in this country or just thank them for not completely imploding their economy overnight, China – Thank you.

Last night’s Chinese economic data for July was as follows:

- INFLATION: CPI only up 10 bps in July to 6.5% y/y (vs. 6.4% in June)

- GROWTH: Industrial Production growth slowed sequentially in July to 14% y/y (vs. 15.1% in June)

- INVESTMENT: Fixed Assets Investment YTD growth slowed marginally in July to 25.4% y/y (vs. 25.6% in June)

I put inflation at the top of this 3-factor model because that’s really what China needs to solve for in Q3/Q4 of 2011. If they do (and we think they will), Chinese inflation growth should slow towards +5% year-over-year with GDP Growth running closer to 8%.

Chinese economic growth has been slowing for 15 months as inflation accelerated. Commodity inflation in China was perpetuated by the US Federal Reserve printing money (Global Commodities trade in US Dollars). Now we are seeing what Hedgeye has called for (a Deflating The Inflation) – and that’s a very good thing for China.

Deflating The Inflation is also a very good thing for you, The Consumer. And, in the end, instead of money printing I think 95% of Americans would take a 30% off sale at the pump than another call by Goldman to buy oil at $112/barrel (where Hedgeye said short oil – not that we keep a time stamp on these things or anything).

When it comes to calling this Globally Interconnected Market, “empty your mind, be formless, shapeless – like water.” Money printing may have very well flowed from the gushers of Academia’s Keynesian Dogma for the last few years but, as Bruce Lee reminds us: “Now water can flow or it can crash.”

“Be water, my friend.”

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1648-1761, $78.54-91.66, and 1070-1172, respectively. Our asset allocation in the Hedgeye Asset Allocation Model maintains a 0% position in US and European Equities and a 67% position in Cash. In the Hedgeye Portfolio, I covered shorts yesterday and will look to re-short strength today.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer