THE HEDGEYE BREAKFAST MENU

MACRO

Unemployment

Initial jobless claims came in at 395k versus expectations at 405k consensus for the week ended August 6th. For the week ended July 28th, the number was revised to 402k versus 400k.

Commodities

Gasoline prices are coming down on an absolute basis and this is providing relief to consumers. On a year-over-year basis, however, prices at the pump remain elevated (as the chart below illustrates).

Subsectors

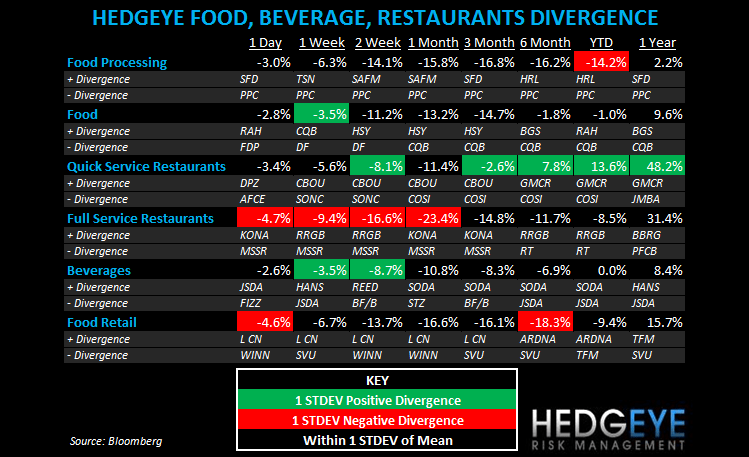

QSR stocks underperformed yesterday along with Food Retail. The broader market dragged all categories lower.

QUICK SERVICE

- WEN reported 2Q EPS of $0.05 versus consensus $0.05 this morning. Comps exceeded expectations at +2.3% for company-owned restaurants versus consensus at 1.5%. Margins were heavily impacted by commodity costs (180 basis points) and incremental advertising to support the new Wendy’s breakfast in additional markets (60 basis points).

- JACK reported results for Q3FY11 last night. Margins dragged down EPS to $0.25 ex-items versus $0.40 expectations. Comps continue to trend higher (Jack company comps +4.7% versus +3.3% consensus and Qdoba system +5.1% versus consensus 5.0%) and the company raised the low end of FY11 comp guidance for Jack and Qdoba.

FULL SERVICE

- EAT reported a strong quarter this morning, beating consensus EPS by a penny with $0.48 in Q4FY11. Comps came in at +2.8% blended versus 1% consensus and Chili’s comps were +2.6% versus 3.3% expectations. Restaurant margins were 18.3% versus 17.1% expectations. Tellingly, management raised FY12 EPS guidance to $1.80 to $1.95 versus current expectations of $1.76. EAT remains one of our favorite names in the space and has been for some time.

- CHUX reported 2Q EPS of ($0.08) versus consensus ($0.05) and O’Charley’s comps of +2.9% versus consensus 1.1%. O’Charley’s management says that beef, dairy, and seafood costs are up during 3Q. This is bearish for CAKE, given what we believe is the government’s overly conservative commodity guidance for 4Q.

- CAKE raised to “Buy” from “Neutral” at Lazard Capital.

Howard Penney

Managing Director

Rory Green

Analyst