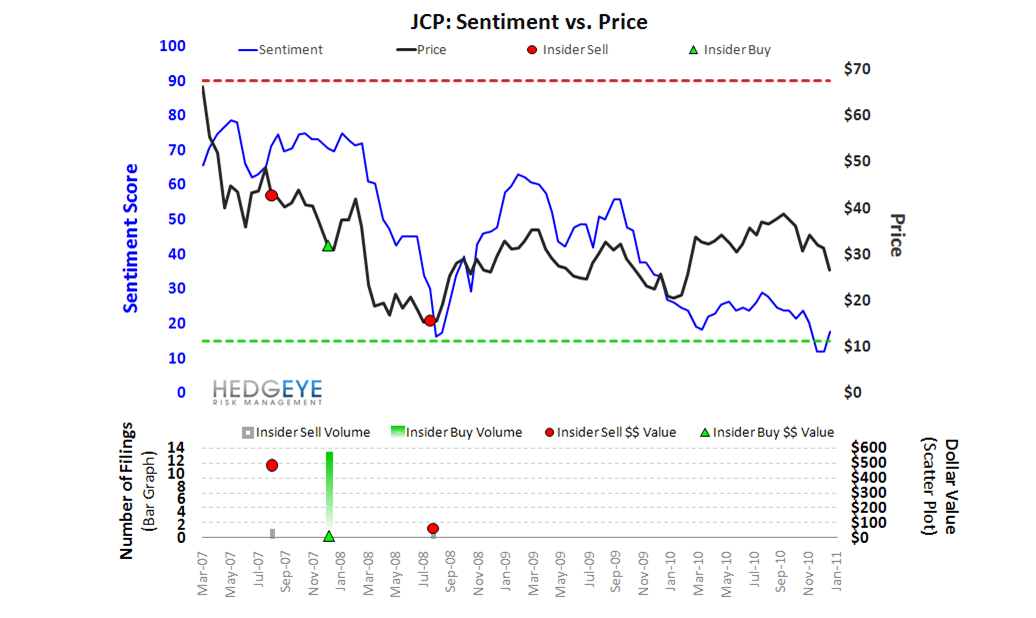

JCP’s Q2 earnings out Friday are going to come in well shy of the company’s guidance, no surprise there. The bigger issue at hand is the duration mismatch between the timing of investments needed to execute on Ron Johnson’s master plan and current earnings expectations, which are too high. We firmly believe both numbers and the stock are headed lower from here.

July same-store-sales came in up 3.3% last week capping off an unimpressive quarter in which comps are likely to come in at +1.5% compared to guidance of 3-4%. This shortfall is due in part to a materially underperforming e-commerce business, which is up only LSD and running well below full-year double-digit growth expectations. With limited room for upside in gross margins as a result of the company’s competitive pricing position and limited product differentiation, SG&A will be the key lever to manage for the balance of the year. We’re shaking out at $0.07 for the quarter vs. the Street at $0.10 and management’s initial Q2 guidance of $0.20-$0.24. Given our expectation for meaningfully lower earnings, we expect JCP to take down full-year guidance for revenue, gross margins, and EPS Friday. To be clear, our thesis goes far beyond this quarter’s results.

As we outlined in our recent JCP Black Book, here’s the setup heading into the quarter:

- Over the near-term (Trade = 3-weeks or less), JC Penney is one of the most poorly positioned companies in the industry as it relates to the margin compression we see ahead. We’re at $1.82 vs. the Street at $1.94 in F11.

- In the intermediate term (Trend = 3-months or more), we’re looking at much of the same. Numbers as the company looks today are too high in F12. Again, we’re at $1.33 vs. the Street at $2.40.

- Over what we consider long-term (Tail = 3-years or less) we’ll be seeing meaningful investment back into the model, as Ullman exits either by choice or force. Then we’ll see SG&A and CapEx both go up meaningfully. Mind you, Apple lost money in retail for the first 2+ years, and fell short of its publicly stated profit goals for 2 years because Johnson opted for the benefit of long-term shareholder value, not the inability to perform. We think that this is what will take earnings down – potentially below zero based on our analysis. In F13, we’re at $1.22.

- Then, and only then, can JCP rise from the ashes and emerge into whatever it is that Johnson is envisioning. Heck, it might prove to be the best stock in the S&P. But that might not be until years 5-7. Johnson’s warrants get him paid – keeping in mind that he probably doesn’t need the money to feed his family in the interim.

- In the interim, investors have to cope with 1) the real earnings power of this company, estimates for which are too high, while keeping the Ackman’s of the world spinning their tales of value creation.

See our recently released JCP Black Book for more detail on this and other factors that have us squarely in the bear camp on JC Penney. If you are interested in receiving a copy, please contact .

Casey Flavin

Director