Global growth is slowing, commodity prices are coming down, and this should bring some relief to restaurant margins, all else held equal.

Summary

The dollar gained, week-over-week, and commodities generally declined over the same period. Beef prices gained 1.3% week-over-week as demand, globally, continues to be strong. The United Nations’ meat price index has gained 18% in the past year, according to a Food and Agriculture Organization report in July. Increasing demand in China and other emerging markets is constraining supply and supporting global beef prices. Coffee, Corn, Cheese, Chicken, Soybeans, and Hogs all declined meaningfully week-over-week. Importantly for U.S.-centric restaurant companies, gas prices came down -1.8% in the last week which is a positive for consumers.

Commodities

Live Cattle

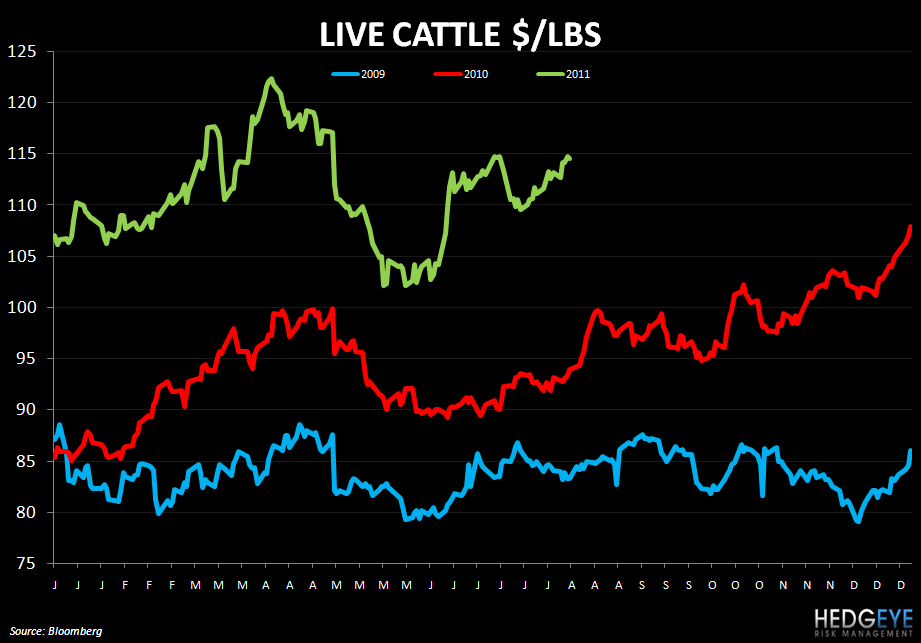

Beef prices were up 1.3% over the last week as most other commodities declined. Demand for beef, within the US and in international markets is strong; consumption of hamburgers in the U.S., for instance, is significantly higher in 2011 than in 2009. 48% of consumers surveyed by Technomic say they eat a burger at least once per week versus 38% in 2009. In terms of international demand, we expect inflation in China and concerns about radioactivity in Japan to keep meat exports from the US strong.

Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls.

RRGB (5/20/11): “Ground beef could be higher by as much as 20% year-over-year, which has a meaningful negative impact to our margins.”

HEDGEYE: Live cattle prices are up +22.7% y/y. See the price chart above.

JACK (5/19/11): Beef accounts for more than 20% of our spend and is the biggest factor driving the change in our guidance. For the full year, we are now anticipating beef cost to be up nearly 14% versus our previous expectation of 9% inflation. We expect beef cost to be up approximately 14% to 15% in the third quarter.

HEDGEYE: Live cattle prices are up +22.7% y/y. See the price chart above.

WEN (5/10/11): We communicated to you back in March that we expected beef cost to rise approximately 10% to 15% and that we expected our total commodity costs to rise 2% to 3% in 2011. We are now forecasting that our beef cost will rise 20%.

HEDGEYE: There is moderate upside risk to beef price guidance for WEN.

EAT (4/27/11): Well, consistent with what we've talked about in the last month or so as we visited many of you, beef continues to present the most significant inflationary pressure in our commodity basket.

MRT (5/4/11): Q: I wanted to revisit the overall expectations for your commodities basket, and I missed the part about beef, just wanted to verify that it was up in the 20% range. A: no, no, no. I said in the low double-digits.

HEDGEYE: This is possible, even probable, for the year looking at average 2010 versus average YTD 2011 prices, and given the easier compares in the fourth quarter, but will require no sustained upturns from here.

Corn

Corn declined week-over-week as concern about the weakening of the U.S. recovery eroding demand impacted demand. Nevertheless, conditions in the U.S., the world’s largest producer of corn, continue to deteriorate and food processor companies are concerned. The possibility of crop yield estimates coming down due to continuing hot and dry conditions throughout much of the corn-growing regions of North America is driving prices higher over the past couple of days. We see the tightening supply of corn as bullish for protein prices and negative for food processor margins.

Below is a comment from AFCE pertaining to corn prices from a recent earnings call.

AFCE (5/26/11): On a full year basis, we now expect the Popeye’s system will experience an increase of 4% to 5% in food costs. This is up from our previous guidance of a 2% to 3% increase, primarily due to higher commodity costs in corn and soy, which impacts our bone-in chicken, as well as increases in the cost of flour and cooking oil.

HEDGEYE: Corn costs going higher are going to squeeze margins for food processors and, in turn, their clients.

Coffee

Coffee prices have been trending lower since early in the second quarter as supply concerns have eased and global growth slowing crept into consensus expectations. Concerns about weather conditions in Brazil have boosted prices today but, overall, the trend has been lower as the chart below illustrates.

Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls.

PEET (8/2/11): “As we indicated, in our first quarter call, we had to buy a small amount of our calendar 2011 coffee beans at significantly higher prices and this coffee will roll into our P&L during the third and fourth quarter.”

“Higher priced coffee resulted in gross margins this quarter being 290 basis points below prior year. In our first quarter conference call, we indicated that in addition to the overall higher price coffee market, we had to buy a small amount of coffee this year at significantly higher prices. And as a result, we expected our coffee cost to be 40% higher in fiscal 2011.”

HEDGEYE: Peet’s is a company with a very competent management team that manages coffee costs extremely well. Its higher-end, loyal customer base makes the price elasticity of demand more inelastic than for other coffee concepts’ products.

SBUX (7/28/11): “As I mentioned earlier, are absolutely a headwind for us in the full business and that's most acutely impactful on margins in CPG as it's a much more coffee intensive cost structure, as you know. I can tell you that the decline as I spoke about it earlier from about 30% operating margin in CPG this year down to the target 25% next year is really all explained by commodities. Absent commodity inflation we'd be at or improving our margin in the coming year.”

“As we had anticipated, in recent weeks, coffee prices have retreated significantly from a high of more than $3 per pound just a couple of months ago to levels now near $2.40 per pound. As prices have been falling we continue locking up our needs for fiscal '12 and now have virtually the full year price protected.”

HEDGEYE: Starbucks is aligning itself with the right partners to gain more control of its coffee costs to provide investors with more certainty going forward and to protect its margins as global coffee demand continues to rise.

GMCR (7/27/2011): “However, what we've said is that should coffee prices or other material costs spike, we will certainly consider price increases as necessary. We certainly hope that we do not have to cover one again next year. But our objective long-term is attempting to maintain our gross margin as we would see input costs come along.”

HEDGEYE: GMCR hedges out 6-9 months in advance. Without a rising dollar and some stronger supply growth to counteract growing global demand, we expect sustained elevated prices.

Howard Penney

Managing Director

Rory Green

Analyst