This note was originally published at 8am on August 05, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“He who will not economize will have to agonize.”

-Confucius

I lost over three hundred dollars of my net wealth yesterday. Happy Anniversary Laura.

Actually, if you back into the valuation of my largest holding (Hedgeye)… assume a 3-month Treasury discount rate of 0.00% (this morning you almost have to pay the government to hold your money)… and infer that our team’s analytical competence added some value to our clients’ risk management process this week… I think I made back my three hundred bucks.

Like a lot of things manic media and the Wall Street/Washington they cover, their concept of CASH can be amusing. I personally invested approximately 1/3 of my CASH in this company during the thralls of 2008. I considered that a relatively “high conviction” idea.

But when Wall Street talks about CASH, bankers and brokers are usually talking about your money. There is a gargantuan marketing machine that stands behind this basic compensation mechanism – they need other people’s money to make money.

People are always asking me “what’s your best long term idea”? Away from Hedgeye, I think CASH is the best weapon for self defense in the modern Fiat Fool world in which we live. CASH saves you on a day like yesterday (worst day for US Equities since 2008). CASH also provides you the opportunity to make long (or short-term) investments when your competition is not allowed to make them.

Back to the Global Macro Grind…

Before the price of Silver collapsed intraday, I raised another 12% CASH in the Hedgeye Asset Allocation Model. That takes my CASH position to 67%. I sold my 6% allocations to the US Dollar and Silver (total = 12%) at 10:27AM and 11:06AM, respectively. At the time, they were both up on the day. I was pleased.

Now a lot of people (and I mean a lot) told me I “couldn’t” go to 96% CASH in Q3 of 2008. Less people will tell me I can’t go to 67% CASH in 2011. Why? Most likely because I just did.

The idea here this morning isn’t to take a victory lap (although these things do occur for winning teams). The idea is the same idea I have been pounding on since 2008. Our industry needs new ideas, new risk management processes, and new blood. Re-think. Re-work. Evolve. Old Wall Street knows that. They are Too Big To Change as fast as Hedgeye has changed – Old Wall Street knows that too.

Today’s Hedgeye Asset Allocation is as follows:

- CASH = 67%

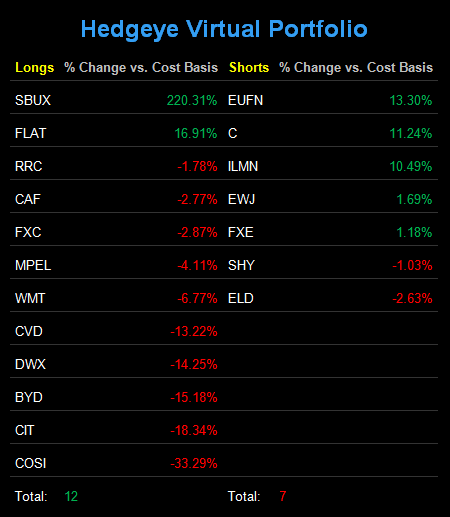

- Fixed Income = 18% (Long-term Treasuries and US Treasury Flattener – TLT and FLAT)

- International Equities = 9% (China and S&P International Dividend ETF – CAF and DWX)

- International Currencies = 6% (Canadian Dollar – FXC)

- Commodities = 0%

- US Equities = 0%

Again, this is an asset allocation product, not a hedge fund or a book of long/short ideas (that’s the Hedgeye Portfolio – different product). When I think about this product, I think about Laura, Jack, and Callie. That’s who I work for when preserving our assets.

I also work for them to grow our assets. But another funny thing about Wall Street is that some people think you should be in “growth” mode every day.

In some asset classes, some of the time, sure – great idea. Most of the time, in most asset classes, that’s a really bad idea. Markets that are being manipulated by central planners do not owe us anything.

Globally interconnected markets care about a lot of things at the same time. Right now, they are anchoring on the #1 risk that no one was talking about in mainstream media yesterday: Fiat Fools trying to convince the Institutional Investing Community to chase yield.

Chasing yield is all good and fine until the music stops. Remember what the buy-side bus tour operator, Citigroup’s, retired storyteller (the artist formerly known as Chuck Prince) told the Financial Times on July 10, 2007:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing…”

Today is August 5, 2011. It’s our 5thWedding Anniversary and I, for one, feel like the luckiest man in the world today. I married a beautiful, loving, and thoughtful woman. I have healthy children. I have a happy firm.

And I still have my cash.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1633-1671, $86.52-91.95, and 1165-1256, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer