“Memory is a process, albeit a faulty one.”

-Jane Leavy

That quote comes from the Preface of Jane Leavy’s recent Bestseller “The Last Boy – Mickey Mantle and The End of America’s Childhood.” I just started reading it last night and it helped me reconcile some of the conflicting thoughts in my head.

If you open your mind, you can always learn something from someone. Even if that’s learning what not to do. Mr. Macro Market teaches us something each and every market day. Yesterday it taught me that career risk management is as relevant as risk management itself.

At 2:45PM yesterday, the SP500 was testing the 1101 level, making a credible threat to move into what we call the crash zone (down -20% from its YTD peak of 1364 on April 29, 2011). Seventy five minutes later, the SP500 closed the day at 1172 – up 6.4% in 75 minutes of trading! La Bernank calls this le “price stability.”

That wasn’t a bounce. That wasn’t an intraday rally. That was career risk management buttons being pushed (BUY), in size, at the 1100 line – at the intraday and YTD low. Remember, the art of money management is having money to manage.

Market bottoms are processes, not points. And the entire construct of American finance (a large construct) is finally engaging, emotionally, in the process of jogging their 2008 Market Memory.

Many a perma-bull would have you believe yesterday’s intraday rally was based on the “yield differential between stocks and bonds.” Others continue to tell you that stocks went up because they are “cheap.” Right.

To borrow a much more reasonable explanation of what the market does and when, here’s Jane Leavy’s (using America’s treasured pastime as a metaphor for how Americans remember things they are supposed to love): “…like the sweater in my office, Mickey Mantle is a blend of memory and distortion, fact and fiction, repetition and exaggeration.”

Back to this morning’s Global Macro Grind…

As levered long hedge funds deal with their 2011 performance problems in America (they’re down more than mutual funds who don’t use leverage), the rest of the world, shockingly, didn’t cease to exist yesterday.

Across countries, currencies, and commodities, there’s a lot going on this morning:

1. ASIA – China’s most trusted economic advisor (Singapore) CUT its export forecast for 2011 last night. That’s a big deal as it’s a pseudo honest representation about what Asia really should be thinking when considering all of the money printing by Fiat Fools. Deficits, Debt, and Zero Percent Interest Rate Policies STRUCTURALLY DEPRESS ECONOMIC GROWTH (Princeton Economics Department, take notes).

Singapore’s stock market sold off on that “news” closing down a full -1.9% overnight and really put a large wet Kleenex on what the buy-and-hope crowd in America was looking for this morning - a follow through on yesterday’s bull charge, with a big overnight session in Asia, and big UP futures to story-tell about. Didn’t happen.

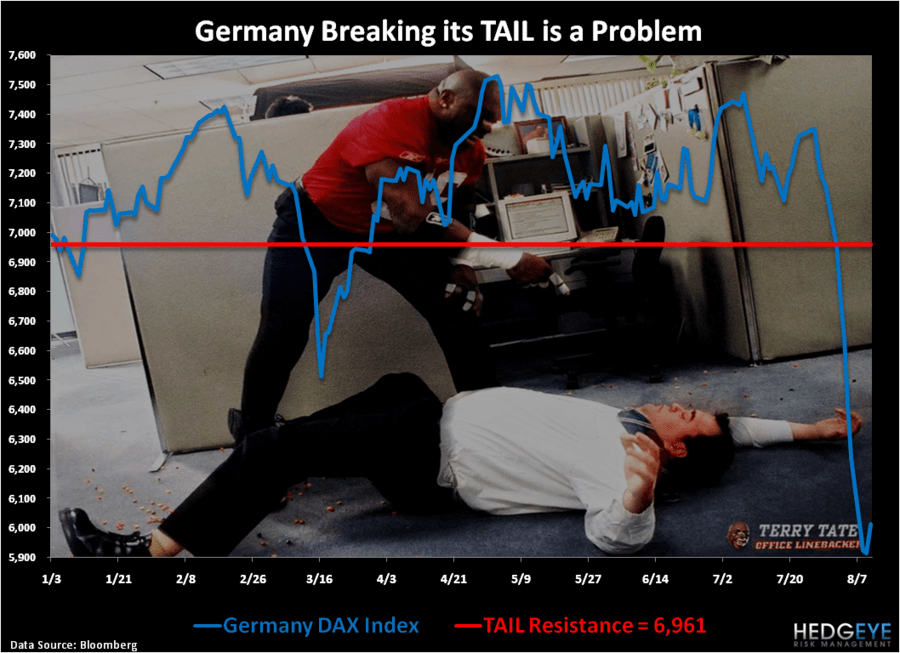

2. EUROPE – Evidently, arresting a US stock market crash into yesterday’s close didn’t stop gravity. Economic growth in Europe continues to slow and that’s why German stocks have crashed alongside all of the Europig nations. In bear markets (all of European Equities are in one, fyi), I learn a lot more from the complexion of the bounces than I do the selloffs.

Anyone with a calculator knows that Greece, Italy, and Spain have crashed. But do people realize that German stocks are crashing? Inclusive of this morning’s low-volume +1.6% “bounce” in Germany’s DAX Index, the market is still down -20% from its May 2011 peak. That’s a problem. Germany’s TAIL is broken.

3. USA – Our cerebral Director of Research, Daryl Jones, wrote an outstanding note yesterday titled “Is There Cheap Valuation Blood In The Water” (if you’d like the note email ) and without recapping the entire historical data series, here’s the bottom line on US stocks: they aren’t expensive anymore; they aren’t cheap either – they are perfectly priced for storytelling.

For the sake of a bear’s storytelling purposes, let’s assume the duration of the countless marketing machines out there who are still pitching Jeremy Siegel’s “Stocks For The Long Run” – and let’s use the longest of long-runs. At a closing price of 1172, the SP500 continues to make LOWER long-term LOWS, down -25.1% versus their long-term peak (2007) and down -14.0% from their LOWER-HIGHS established in April of 2011.

Now if we want to throw away our Market Memory for another second and assume the Keynesian Textbook position that ‘low bond yields means buy stocks’, we humbly submit that you still need to get the timing right.

With 2-year US Treasury Yields hitting all-time lows today at 0.17% (all-time is still a very long time) and 10-year yields collapsing toward their all-time lows established in 2008, again, we humbly submit that buying a stock because “it’s cheap” in 2008 should inspire bad memories about what’s left of your 401k. Fictionally “cheap” can get cheaper and repeating the same mistakes gets people run over.

My immediate-term ranges of support and resistance for Gold (bullish), Oil (bearish), and the SP500 (bearish) are now $1, $78.58-89.97, and 1114-1231, respectively. Our Global Macro team will host a conference call at 11AM EST to go through what to do next.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer