TODAY’S S&P 500 SET-UP - August 9, 2011

Markets around the world are crashing now. We define crash as a 20% peak-to-trough decline in price, but people tend to internalize crashes versus their own expectations. Given what consensus expectations for 2011 were based on, we’re not surprised.

The list of 2011 “CRASHES” – from 2011 peak price: Greece = -43.9%, Italy -34.6%, Germany -25.6%, Financials (XLF) = -29.2%, Industrials (XLI) -23.7%... and now you are seeing daily emerging market moves of -8% (Brazil yesterday) to -12% (Romania this morning).

At Hedgeye we feel that waking up begging for Bernanke to arrest gravity is not a risk management process; away from cutting his US GDP growth estimates (again) today, what can he do? Buy bonds? They go up every day!

As we look at today’s set up for the S&P 500, the range is 102 points or -4.42% downside to 1070 and 4.69% upside to 1172.

The Hedgeye models have a 3 standard deviation level of support at 1070 SPX and since 2008, 3 standard deviation moves occur frequently. Covering shorts on the down move, not busting out the gross long guns. At 1070, maybe!

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -3608 (-1565)

- VOLUME: NYSE 2543.62 (+12.85%)

- VIX: 48.00 +50.00% YTD PERFORMANCE: +170.42%

- SPX PUT/CALL RATIO: 2.04 from 2.59 (-20.99%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.92

- 3-MONTH T-BILL YIELD: 0.05% +0.04%

- 10-Year: 2.40 from 2.58

- YIELD CURVE: 2.13 from 2.30

MACRO DATA POINTS:

- 7:30 a.m.: NFIB Small Business, est. 89.9, prior 90.8

- 7:45 a.m./8:55 a.m.: ICSC/Redbook weekly retail sales

- 8:30 a.m.: Non-farm productivity, est. (-0.9%), prior 1.8%

- 11:30 a.m. U.S. to sell $35b in 4-wk bills

- Noon: DoE short-term energy outlook

- 1 p.m.: U.S. to sell $32b in 3-yr notes

- 2:15 p.m.: FOMC Rate Decision

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- S&P cuts the AAA ratings of thousands of municipal bonds tied to the government, including housing securities and debt backed by leases

- U.S. home values had their smallest decline in more than 4 years in 2Q, as the share of borrowers with negative equity shrunk, Zillow says

- China’s inflation climbs 6.5% in July, the fastest pace in 3 years

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Gold Advances to Record as Equity Rout Stokes Investor Demand

- Crude Falls to 10-Month Low in New York; Brent Dips Below $100

- Hay Sent to China Cheaper Roiling U.S. Dairies: Freight Markets

- Oil Supply Rises in Survey on Reserves, Imports: Energy Markets

- Copper, Aluminum, Lead Climb on Intervention Hope After Slump

- Commodities Slump to Eight-Month Low as Slowdown Erodes Demand

- Rice Futures in Tokyo Jump by Daily Maximum on Radiation Fears

- Aquila CEO Says ‘Dozens’ Are Studying Coal Acquisition

- Copper Output in China Advances to Record as Aluminum Drops

- Palm Oil Drops to 9-Month Low as Slowdown May Reduce Demand

- Gold Rises to Record as U.S. Rating Cut Spurs ‘Heavy’ Buying

- Texas Dust-Bowl Redux Spurs Record U.S. Cotton Loss, Farm Claims

- Corn Drops to One-Week Low as ‘Gloomy Economy’ May Lower Demand

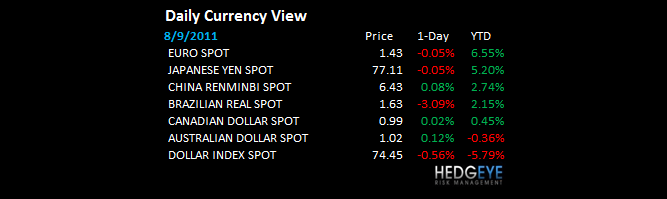

CURRENCIES

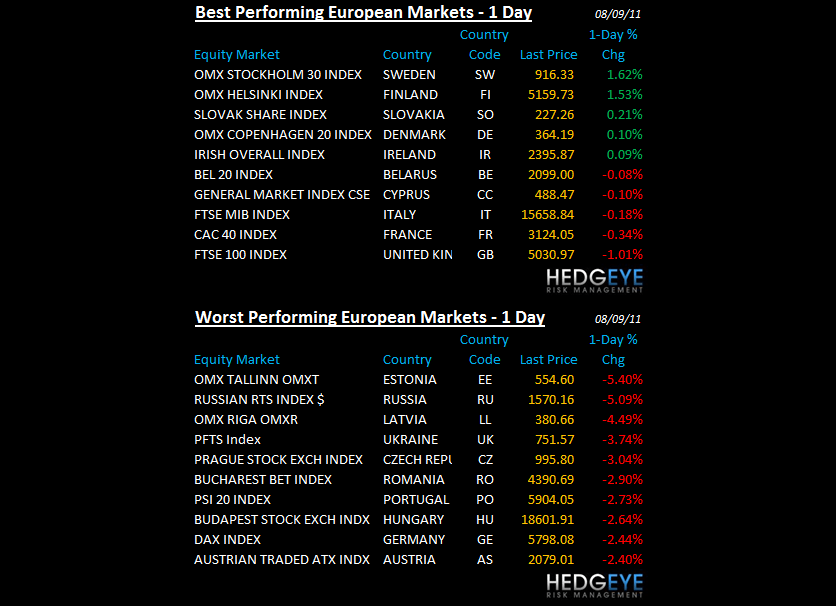

EUROPEAN MARKETS

- EUROPE: looking on the bright side, provided you aren't long Romania (down -12% this morning)

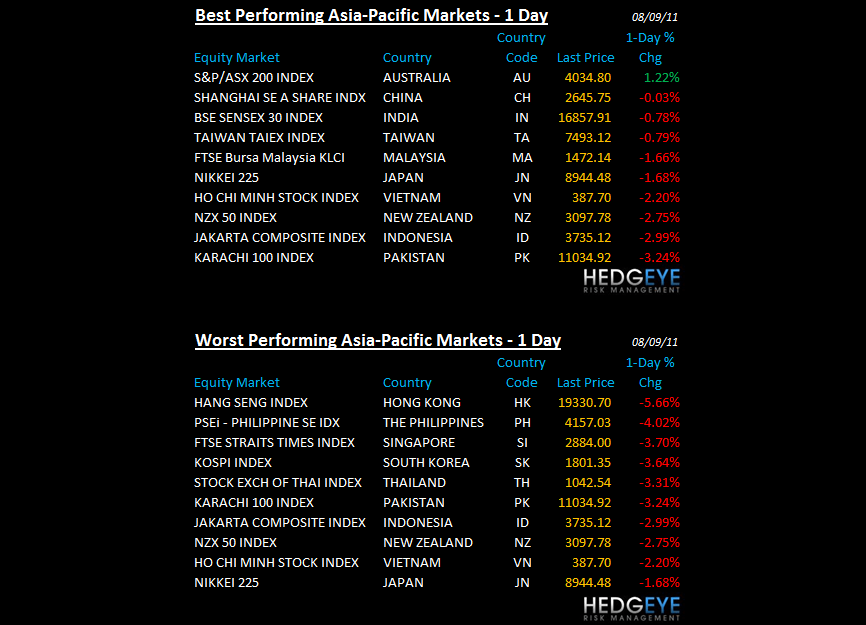

ASIAN MARKETS

- ASIA: KOSPI down the most of the majors (ex HK), down -3.6% and -19.2% since MAY, proving once again that governments should just get out of way

- China stopped going down last night - that’s as critical an indicator of support as there is in Asia; Australia stocks followed that higher

- CHINA – the data was fine with JULY inflation data (CPI) all but assured to be the high for 2011 YTD; Chinese stocks stopped going down last night on that news and that’s the 1stmarket we buy in global equities; not Germany or USA

MIDDLE EAST

Howard Penney

Managing Director