“Common sense is not so common.”

-Voltaire (quote used at the end of David Einhorn’s Q2 2011 letter)

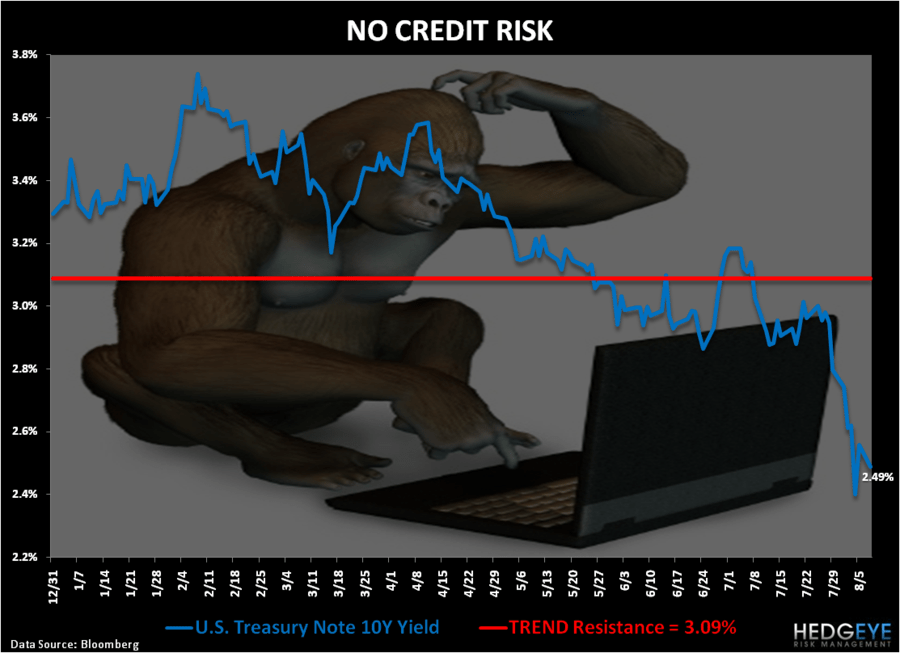

This morning has nothing to do with legitimate credit risk in America’s sovereign debt. US Treasuries would be collapsing if it did. Instead, stocks are as Treasuries are making new 2011 highs!

This morning has everything to do with analytical incompetence. If watching the analytically incompetent chastise the analytically incompetent yesterday didn’t remind you that both S&P and the US Government have issues, you need to replay the tapes. The People don’t trust either ratings agencies or governments’ risk management processes anymore. And they shouldn’t.

As outgoing Chairperson of President Obama’s “Council of Economic Advisers”, Austan Goolsbee, told Meet The Press yesterday that S&P had “Questionable Mathematics”, I literally started laughing out loud. This is AFTER the US government revised their Q1 2011 GDP estimate for the US by 81% to the downside to 0.36%!

With all due respect to my fellow Yalie (Goolsbee was Yale 1991), there is nothing to respect about the accuracy of either the US government’s economic forecasts in 2011 or what US Growth Slowing implies for any rating agency that has to impute a massive top line slowdown into its rating. AFTER the top line (revenues) slows, both the sell-side and ratings agencies downgrade – not before. They are THE lagging indicators.

Bloomberg Consensus (78 buy-side and sell-side institutions) forecasts for US GDP Growth in Q3 and Q4 of 2011 are still at +3.2% respectively. Our models continue to point to rates of U.S. economic growth that are HALF, or less, of those consensus estimates.

There is nothing questionable about this math: the US stock market has lost -12% of its value since the end of April for a lot of reasons – but one of the most obvious has been Growth Slowing.

Back to the Global Macro Grind…

Why are US Treasuries bid to new all-time highs (all-time is a long time) on the “news” of a rating agency downgrade this morning? That’s simple. This is old news to the analysts who provide Wall Street with leading indicators.

To review the time stamps:

- March 5, 2010: Jim Grant issued an effective downgrade of USA’s long-term bonds

- May 14, 2010: Hedgeye cites Grant’s work and reiterates the conclusion using Reinhart & Rogoff data to compliment our own

- August 3, 2010: Hedgeye holds a conference call titled “Should US Debt Be Rated Junk?”

As recently as July 7th, 2011 in his quarterly client letter, Greenlight Capital’s David Einhorn wrote (on page 3): “Earth to S&P, if you can foresee a near-term default scenario that is plausible enough for you to warn about it, AAA cannot be the correct current rating.”

Einhorn, like Jim Grant, is one of the world’s most competent financial analysts. He has been profiting from the incompetence of ratings agencies and the governments who pay them for years. Einhorn and his clients won’t be freaking out this morning or looking for Bill Miller and Timmy Geithner to throw them some completely conflicted and compromised view of S&P’s work. They’ll be profiting from it.

Tomorrow starts today – so what’s next? Well, let’s start with what AAA not being AAA means for everyone else’s ratings.

- It’s now politically palatable to downgrade other AAA rated Sovereigns (France)

- Big Bank Ratings that rode USA’s AAA Rating Uplift need to be downgraded

After we moved to ZERO percent US Equity exposure in the Hedgeye Asset Allocation Model last Monday, our Financials guru, Josh Steiner, wrote an important note titled “New Risks For Financials” where he dug into this obvious problem of Big Bank Rating Uplifts:

“There are 8 banks that benefit directly from the United States AAA credit rating through ratings uplifts. They include: BK, STT, BAC, C, WFC, JPM, GS and MS. If the US isn’t AAA, then the implicitly backed Too Big To Fail banks can’t rely on the US’s ratings to get AAA debt themselves.”

Now Steiner has been The Bear on the moneycenter banks and US Housing since this time last year (sorry Meredith Whitney). Hedgeye has shorted Banker of America (BAC) 10x since 2010 in the face of “smart” money buying it on “valuation.”

Well, sorry “smart” money, valuation is not a catalyst.

Neither is a pending downgrade of a bank’s credit rating. Citigroup (our top short idea above and beyond BAC right now, which is saying something!) could see a 2-notch downgrade with the end of these “ratings uplifts”. This will add notably to already existing NIM pressure on Citi’s earnings (NIM = Net Interest Margin).

And when S&P or Moody’s “downgrades” Citigroup, we’ll cover the short position on that “news” too. Timing matters.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $84.02-92.03, and 1165-1219, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer