TODAY’S S&P 500 SET-UP - August 5, 2011

From a research/risk management perspective yesterday was one of the best day’s we’ve had versus our sell-side competition since 08. It was also the biggest down day for stocks since 08, so that makes sense. Having 0% asset allocation to US/European Equities helps!

Every bear market gets immediate-term TRADE oversold, and that’s what I see this morning. That said, I want to be crystal clear on this, sell all rallies in Equities/Commodities because the Street is still too long and needs to take down gross and net exposures.

As we look at today’s set up for the S&P 500, the range is 91 points or -2.92% downside to 1165 and 4.66% upside to 1256.

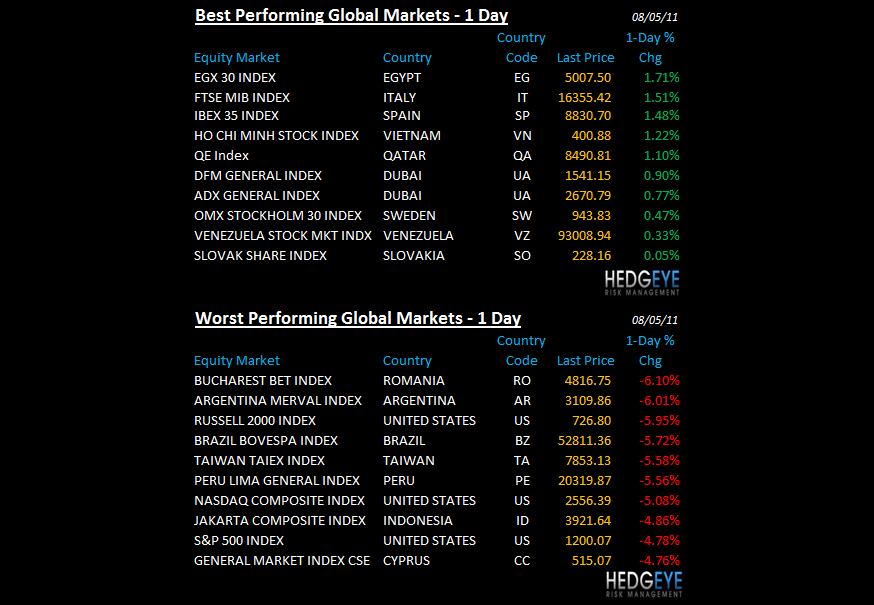

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2818 (-3263)

- VOLUME: NYSE 1821.32 (+34.71%)

- VIX: 31.66 +35.41% YTD PERFORMANCE: +78.37%

- SPX PUT/CALL RATIO: 2.24 from 1.51 (+47.70%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 26.94

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.47 from 2.64

- YIELD CURVE: 2.31 from 2.33

MACRO DATA POINTS:

- 8:30 a.m.: Change in Nonfarm Payrolls, Jul, est. 85k, prior 18k

- Change in Private Payrolls, Jul, est. 113k, prior 57k

- Change in Manu Payrolls, Jul, est. 10k, prior 6k

- Unemployment Rate, Jul, est. 9.2%, prior 9.2%

- 1 p.m.: Baker Hughes Rig Count

- 3 p.m.: Consumer Credit, Jun, est. $5.00b, prior $5.08b

WHAT TO WATCH:

- WSJ is lukewarm on Kraft Foods

- Payrolls probably climbed by 85k workers in July, failing to create enough jobs to reduce 9.2% unemployment rate, economists’ forecast ahead of today’s report

- Google+ may grow to claim 22% of online U.S. adults in a year, surpassing Twitter, LinkedIn to be 2nd-most-used social site after Facebook, survey from Bloomberg/YouGov found

- 2-yr note yield hits record low of 0.3039%

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Commodities Post Worst Run Since 2008, Erasing Gains for Year

- Copper Slumps to Five-Week Low on Concern Growth Will Falter

- Gold Gains in London as Financial Turmoil Boosts Investor Demand

- Oil Drops to Lowest in Eight Months Amid Global Rout on Economy

- China Said to Be Planning Soybean Sale to Rotate State Inventory

- Indonesia May Surpass Japan as Biggest Wheat Buyer in Asia

- Palm Oil Drops as Commodities Plunge on U.S. Recovery Concern

- Rubber Slumps Most in Almost Six Weeks as Economic Concern Grows

- AngloGold Plans Trial to Tap $118 Billion of 3-Mile Deep Ore

- Palm Oil Inventory in Malaysia Climbs to 19-Month High on Output

- Goldman Raises Corn, Wheat Targets on ‘Remarkably Hot’ Spell

- Escondida Workers Vote on Proposal to End Chile Mine Strike

- Wheat, Corn Decline as Economic Recovery Concern Dampens Demand

- Crude Oil May Fall on Slowing Economy Concern, Survey Shows

- Japan Considers Additional Steps to Contain Tainted Beef Crisis

- Copper Seen Above $4 a Pound on China Recovery, Codelco Says

- Zimbabwe Diamond Production Surges After Marange Sales Allowed

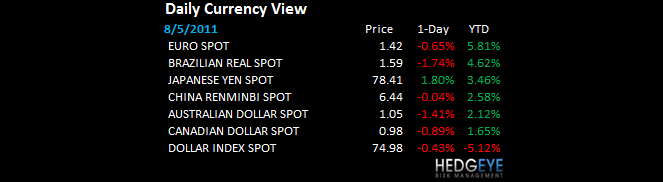

CURRENCIES

EUROPEAN MARKETS

- EUROPE: same scary divergences; all "rallies" trying to come out of the lowest quality markets while the pseudo safe get smoked (Germany)

ASIAN MARKETS

- ASIA: China down the least of the majors in the world this week (down -2.1% last night), and that’s about the only constructive thing I can say

MIDDLE EAST

Howard Penney

Managing Director