PFCB is starting to show up as a long idea in some people’s models. Is now the time?

I’m getting a lot of questions about PFCB on the long side following the recent EPS miss and strong underperformance of the stock. I agree there is big money to be made catching these mid cap restaurant turnarounds but, like catching falling knives, timing is critical. The risk of sitting on the sidelines for now is that a PE firm or an activist investor may decide to make a run at PFCB. However, at this point, we think there could be some downside risks, but we lack the catalyst to see how the turn is going to unfold.

From a valuation standpoint, PFCB is trading at 5.47X EV/EBITDA or about one multiple points away from the low multiple of 4.52 set back on 11/21/08. Certainly, the stock is cheap but - in our view - it’s cheap for a reason.

In order to become more constructive on the stock, we need a catalyst and visibility that there is a clear path to financial recovery. While the company is addressing the needs of the core customer, it is very difficult to get a grip on how the company’s turnaround plans will impact the financial performance. Until that becomes clearer, we will remain cautious on this name.

First, the company will be making several changes to the menu. Enhanced Happy Hour offerings will likely drive traffic at the Bistro but judging the impact on margins from the new lunch menu will be difficult to do. The company is attempting to boost its lunch business. Management said that the change centers on a shift from serving dinner at lunch to serving lunch at lunch. A standalone lunch menu has been rolled out in test markets with lighter fare that is portioned and priced for lunch and provides a wider variety of items. At the same time, the new dinner menu will offer lower-priced entrées ($8-$12 range). These initiatives are in the testing phase and, in our view; do not serve as catalysts on the long or short side. We will be sitting and watching to see how these initiatives pan out.

Second, the guest service enhancements Bistro, through targeted staffing increases have not fully impacted the P&L yet. Most importantly, spending on the new restaurant look and feel has been accelerated but how the capital will be deployed and what the return on that capital will be is unclear.

I’m not ignoring the changes at Pei Wei but the issues are largely the same.

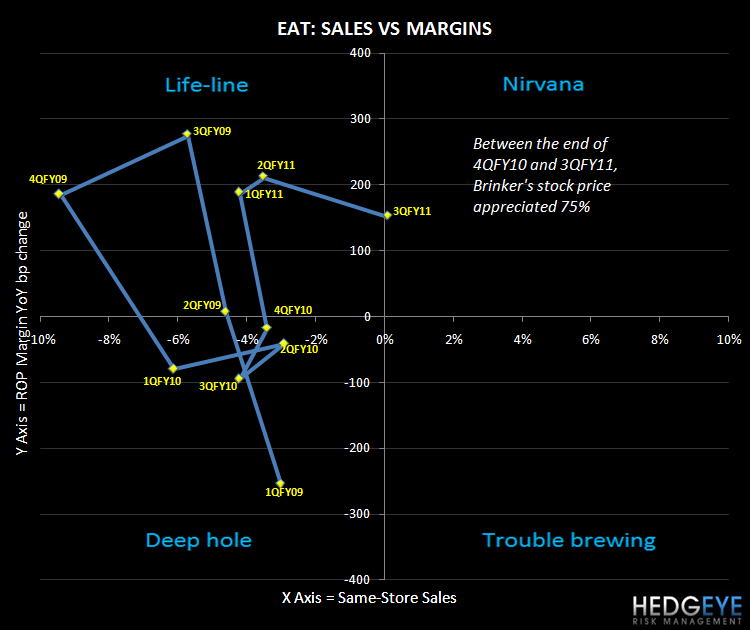

As you can see from the PFCB Hedgeye quadrant charts below, it will be another six months before investors will likely see improvement in the financial performance of the company. In contrast to Brinker, a casual dining company that had successfully turned around its sales and margin trends before the stock worked.

Howard Penney

Managing Director

Rory Green

Analyst