Notable price action and news items from the restaurant space as well as macro callouts pertaining to the space.

MACRO

Consumer

Initial jobless claims came in at 400k for the week ended July 30. The number was below the Bloomberg survey estimate but remains higher than needed to reduce the unemployment rate. The Bloomberg Consumer Comfort Index will be released later this morning.

Subsectors

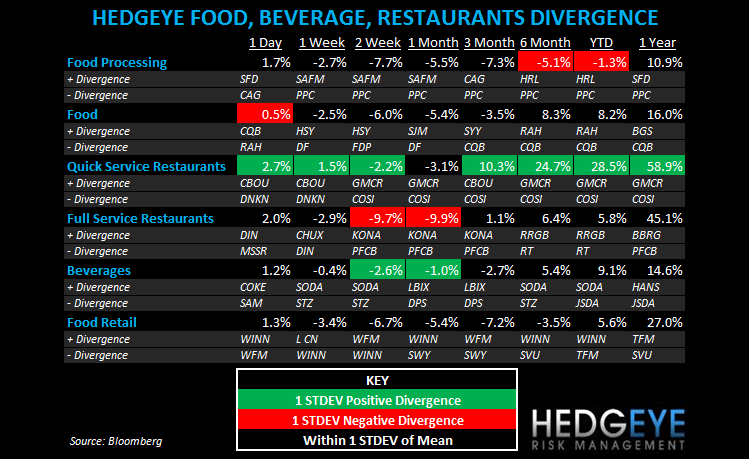

Quick Service outperformed the other food, beverage, and restaurant categories on the back of a strong pre-earnings move from CBOU and a bounce in COSI which has been getting run into the ground recently. The only down stop was DNKN, which declined -4.2%.

QUICK SERVICE

- CBOU coffee announced 2Q earnings of $0.13 ex-items versus $0.09 expectations. The stock was up almost 10% yesterday. Who knew what when?

- MCD was upgraded to Overweight from Neutral at Piper Jaffray.

- DNKN declined yesterday after an earnings release which, to us, left more questions than answers.

CASUAL DINING

- MSSR declined -1.7% on accelerating volume ahead of its earnings call today. DIN bounced back, up 7.2%, after a sharp sell off on Monday and Tuesday.

Howard Penney

Managing Director

Rory Green

Analyst