This note was originally published at 8am on July 28, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We have many constraints as investors.”

-Seth Klarman

Baupost’s Seth Klarman is no stranger to going to cash. Neither is he shy about telling it like it is about how the game of Institutional Asset Management works. The aforementioned quote has nothing to do with the self-directed individual investor. It has everything to do with Institutional Constraints.

“Constraint”, per Wikipedia, “is an element factor or a subsystem that works as a bottleneck. It restricts an entity, project, or system from achieving its potential with reference to its goal.” Institutional Constraint isn’t what Klarman calls it, but I think he’d agree.

In Grant’s back in Q1, Klarman said “we want short-term performance, and are measured by this. There is enormous pressure from clients for short term performance. Mutual funds compete in a relative space. What’s important is absolute returns. The way people do this is forced mediocrity. To do absolute performance, you have to bet against the crowd sometimes.”

Sometimes betting against the crowd too early makes an investor wrong. Sometimes betting against your current positioning can make you less wrong. In a market like this, where Institutional performance chasing is one of the most misunderstood long-term TAIL risks we’re observing, price levels matter – big time. So does considering them on a multi-factor, multi-duration basis.

What does multi-factor mean?

First, let me tell you what it doesn’t mean:

- Point and click 1 factor models of simple moving averages (50 day, 200 day, etc)

- Being sucked into the Sentiment Vacuum of 1 topic (Debt Ceiling is the #1, #2, and #3 most read on Bloomberg this morning)

- Considering Global Macro risk from the vantage point of 1 country and/or 1 asset class (“what’s the Dow doing?”, c’mon)

Within the construct of Chaos/Complexity Theory (my modern day market practitioner’s answer to stale academic Keynesian Dogma), multi-factor is as multi-factor does. You need to build a risk management process that absorbs multiple price, volume, and volatility signals, across multiple asset classes, and across multiple durations.

If I had 10 Chinese Yuans for every person I’ve met in this business who says “well, the chart looks good”, I’d have a lot more money to fund Hedgeye’s growth. What, precisely, do charts mean? The answer to that is as simple as the deep simplicity Chaos Theory aspires to achieve. The chart looks as good as the math you have embedded in the picture!

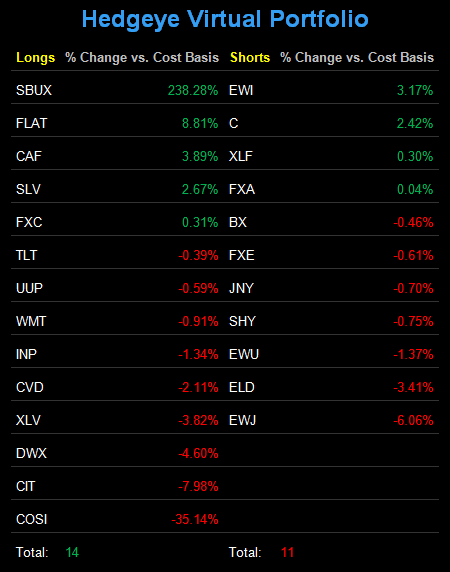

If bells weren’t going off in your Global Macro Risk Management Process yesterday, I suggest you get a new one. Here are some of the alarms going off in mine that had me take my Cash position back up to 46% from 37% (where I started the day):

- EUROPE – both European stocks and bonds are turning into a proactively predictable train wrecks. Our research catalysts remain crystal clear (accelerating debt maturities for the majors through September) but, more importantly, now all of our TRADE and TREND lines across every major European stock and bond market (ex-Russia) have been broken and confirmed by volume and volatility studies.

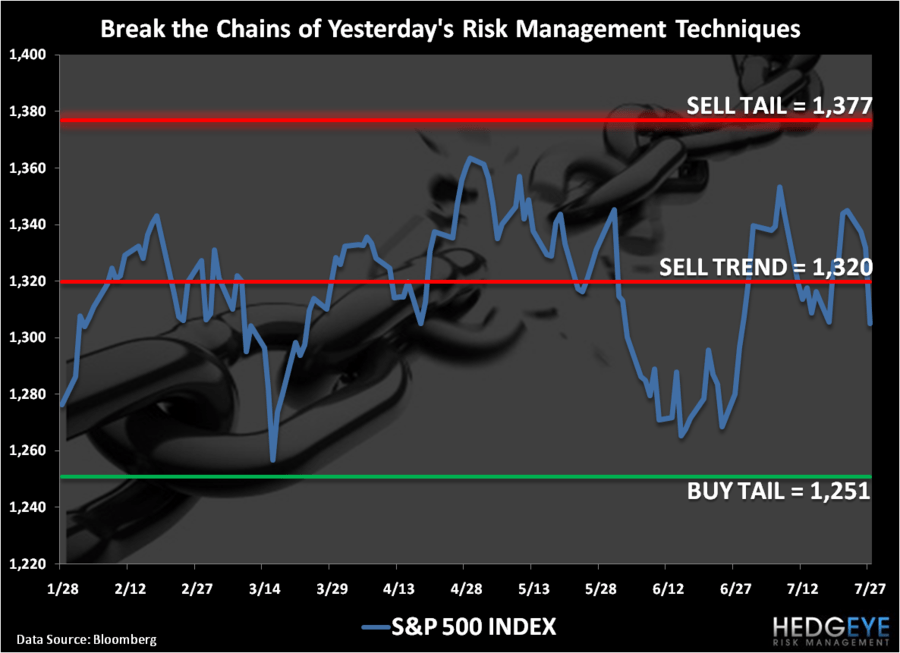

- USA – stocks broke their intermediate-term TREND line of support (1320 in the SP500) and short-term bond yields finally busted a move above my 2-year yield TRADE line of resistance (0.41%). Credit risk derived by market morons in Congress will be priced on the short-end of the curve (where Bernanke has tried to mark it to model for 2 years), so watch that 0.41% line like a hawk.

- GLOBALLY – China’s Shanghai COMP TREND line = 2831 (broken); India’s BSE Sensex TREND line = 18,578 (broken); German DAX TREND line = 7251 (broken); FTSE TREND line = 5985 (broken); SP500 TREND line = 1320 (broken); Russell2000 TREND line = 827 (broken); WTIC Oil TREND line = 103 (broken); EUR/USD TREND line = $1.43 (schizophrenic).

No one at Hedgeye has ever said 2011 Global Growth or 2H2011 Earnings Expectations were priced properly. If you close your eyes to all of my quantitative and research factoring across asset classes and just focus on those 2 - they are VERY large fundamental factors to consider having market impact above and beyond these yahoos in Congress.

Look, I’m not saying I got all of this right. What I am simply saying is that we, as a profession, can get a lot better at this if we just open our minds to re-thinking risk and re-working our asset allocations as the big factors are changing. The market doesn’t care about our respective investment styles, compensation mechanisms, or Institutional Constraints.

My immediate-term ranges for Gold, Oil, and the SP500 are now $1603-1624, $96.03-100.32, and 1298-1316, respectively. I cut my US Equity exposure to 3% (from 9%) in the Hedgeye Asset Allocation Model yesterday.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer