THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - August 1, 2011

Large bond fund managers who bet on US “credit risk” are either unwinding that theme or need to now – across the US Treasury curve bonds are breaking out to new YTD highs and the US Dollar is strengthening, making higher-all-time lows. As we look at today’s set up for the S&P 500, the range is 41 points or -0.93% downside to 1275 and 2.26% upside to 1316.

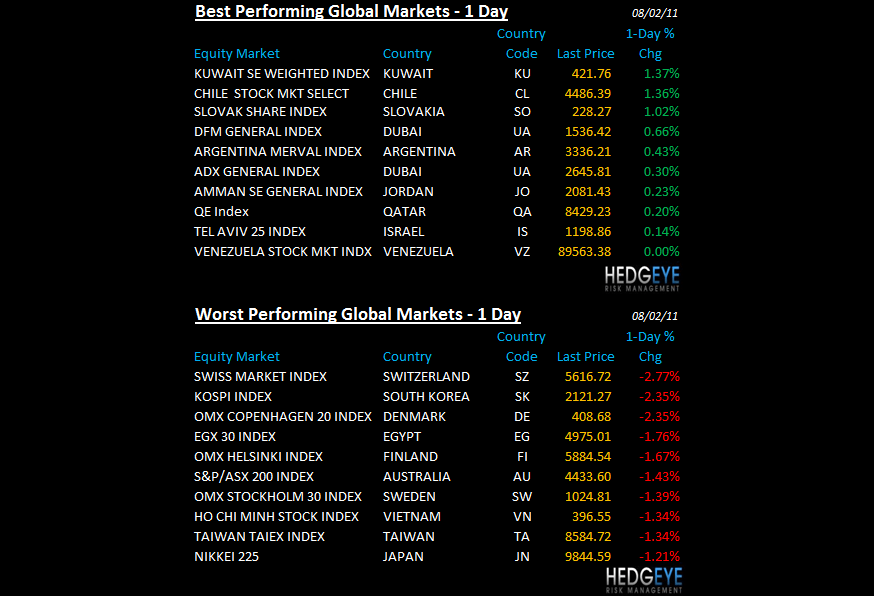

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +195 (+1223)

- VOLUME: NYSE 1110.41 (-8.19%)

- VIX: 25.25 +6.36% YTD PERFORMANCE: +42.25%

- SPX PUT/CALL RATIO: 2.41 from 2.30 (4.57%)

CREDIT/ECONOMIC MARKET LOOK:

YIELD SPREAD – one of the highest conviction long positions we’ve had in 2011 to express our Growth Slowing theme has been a US Treasury Flattener (FLAT); the Spread b/t 10s and 2s is making a new YTD low this morn as bond yields collapse alongside awful US GDP and ISM reports.

- TED SPREAD: 16.06

- 3-MONTH T-BILL YIELD: 0.10%

- 10-Year: 2.77 from 2.82

- YIELD CURVE: 2.39 from 2.46

MACRO DATA POINTS:

- 7:45 a.m./8:55 a.m.: Weekly ICSC/Redbook retail sales

- 8:30 a.m.: Personal income, est. 0.2%, prior 0.3%

- 8:30 a.m.: Persona spending, est. 0.1%, prior 0.0%

- 11:30 a.m.: U.S. to sell $23b 4-wk bills

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- McGraw-Hill reiterated it was reviewing its portfolio after holder Jana Partners said it had discussions with co.

- U.S. light-vehicle delivers in July, to be released later today, may have run at 11.8m seasonally adjusted annual rate, trailing the 12.5m rate in 1H, analysts’ estimate

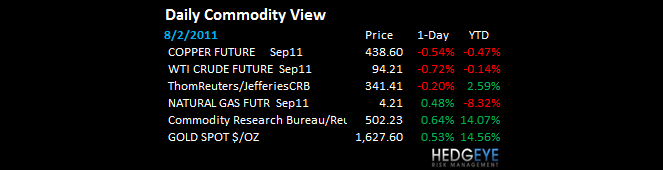

COMMODITY/GROWTH EXPECTATION

OIL – it may have been out of the headlines, but that doesn’t mean its daily price/volume/volatility signals cease to exist; with the USD strengthening, WTIC oil has broken its TRADE line of support ($96.21) this morning and that matters since Energy is literally the only S&P Sector left that’s bullish in US Equities on both TRADE and TREND durations

COMMODITY HEADLINES FROM BLOOMBERG:

- Gold Advances to Near Record as Slowing Growth Increases Demand

- Sugar Falls for Fifth Day on Brazilian Exports; Coffee Rises

- Copper May Climb as Strike Continues at World’s Biggest Mine

- Bank of Korea Boosts Gold Holdings to ‘Reduce Investment Risks’

- BHP Copper Miners ‘Optimistic’ on Agreement to End Chile Strike

- Wilmar Says to Raise Cooking Oil Prices in China by About 5%

- Coffee Seen Rising 10% in Two Months as Vietnam Delays Exports

- Mining Takeovers Heading for Record in 2011, Ernst & Young Says

- Rice May Sustain Rally as U.S. Acreage Declines, Ofon Says

- Japan Widens Cattle Shipment Ban as Tochigi Beef Contaminated

- BullionVault Lures Most Funds Since Lehman’s Collapse on Haven

- Barrick Says Gold to Remain High on China, India Inflation

CURRENCIES

EUR/USD – remains the currency pair that makes the world’s correlation risk go round and this morning we’ve seen another decisive break-down below our $1.43 TREND line; Europig Equities are getting slaughtered – we have no long exposure to anything European Equities; we are long USD and short EUR

EUROPEAN MARKETS

- EUROPE: a royal Europig mess continues with FTSE and DAX breaking both TRADE and TREND lines as Italy and Spain collapse (stocks and bonds)

- UK July construction PMI 53.5 vs consensus 53.0, prior 53.4

ASIAN MARKETS

- ASIA: finally breaking some critical TRADE lines of support; Nikkei and KOSPI in particular down hard through lines that matter last night.

- Australia June residential building approvals (3.5%) vs cons +2.5%.

- Japan June wages (0.8%) y/y.

- Japan June monetary base +15% y/y to ¥113.73T

MIDDLE EAST

Howard Penney

Managing Director