Positions in Europe: EUR-USD (FXE); Italy (EWI); UK (EWU); European Financials (EUFN)

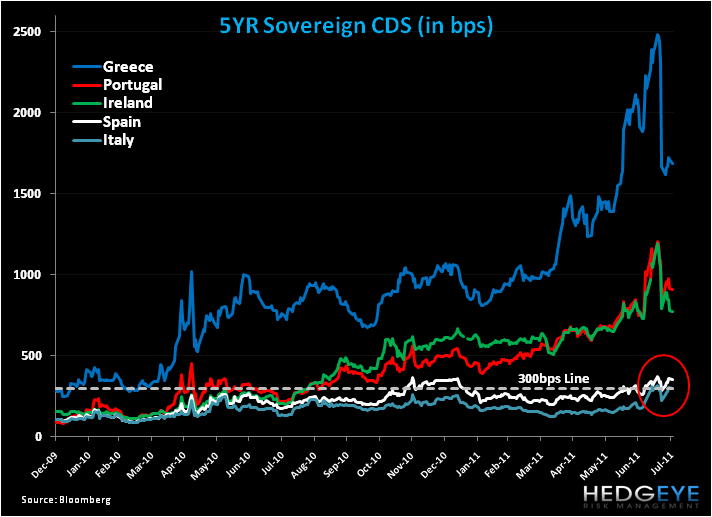

On the day following the July 21st announcement of Greece’s second bailout package risk across the European periphery (PIIGS) nose dived according to sovereign bond yields and cds spreads (see charts below). Yet in the days since both metrics have resumed higher and flirted with key breakout levels (6% on 10YR yields and 300bps on sovereign CDS), all of which gives us pause to monitor the developments of this long term sovereign debt soap opera. Currently we’re short the EUR-USD via the etf FXE; and short Italy (EWI), the UK (EWU), and the European Financials (EUFN) in the Hedgeye Portfolio to take advantage of the headwinds we see over the immediate and intermediate terms.

- Please note that CDS may not be the best indicator of risk because the International Swaps and Derivatives Association (ISDA), which governs CDS pricing, has ruled that the Greek restructuring does not constitute a credit event, which means that CDS will not be triggered.

Here are a few points to considering regarding the EFSF as we move forward in the calendar:

- While it’s true that the bonds issued from the EFSF are AAA rated, proposed at very favorable rates of 3.5% to borrowers, and the fiscally sober-minded Germans are posting the largest amount of collateral to back the facility, it’s apparent that at its current level of €750 Billion (€250 Billion of which is IMF contribution) the facility could not handled the default of Italy and Spain, two country that we think present significant risk in the larger puzzle of the region’s fiscal imbalances. Estimates already suggest the facility would need to be expanded 2-4x to meet the needs of Italy and Spain.

- The new structure of the existing EFSF needs to be unanimously voted on by all EU member states, which includes the individual terms of lending (maturity extension and interest rates commanded) as well as the total size of the facility. If the original issuance of the EFSF (being used for Ireland and Portugal) and the permanent ESM facility (beg. 2013) are any indicators of sentiment, we could well see indecision on the terms, especially on its overall size as individual countries (populaces) would rather not be on the hook for the peripheral countries debt. This vote isn’t scheduled until mid September when the EU parliament returns from summer recess.

- To this point, last week we heard from German Finance Minister Schaeuble who said the EFSF will not be given carte blanche to buy up bonds on the secondary market. This is a critical point for there’s been no indication that yields for the PIIGS are compressing. As a nod to higher yields, Italy sold €2.7 billion of 10-year government bonds late last week at an average yield of 5.77% vs 4.94% on June 28. The ECB (along with China) have unofficially/officially been critical buyers of sovereign issuance ytd. Should the EFSF be limited in any capacity to buy up sovereign issuance this could encourage yields higher (neg.) and/or require other funding solutions.

- As we’ve highlighted in our research, Italy and Spain face significant bonds coming due into year-end and in 2012. This means that the country will have to rely even more on successful future bond auctions (ie sufficient demand at yields not significantly over previous auctions) to fund its costs = more downside risk. Specifically, we continue to see political risk in Spain, both into and out of Prime Minister Zapatero’s announcement on Friday for early elections on November 20th. On the same day Moody’s warned that it may downgrade Spain.

- Finally, there’s also the unknown on how the voluntary bank swaps of Greek debt will go off. 90% of banks say they’ll participate, but there’s plenty of uncertainty around this. It's scheduled for late Aug/early Sept.

Growth Slowing

On the road to 40? European Manufacturing PMI figures for the month of July came in today and the numbers confirm a downward trend over the last 3-4 months. With the 50 line marking expansion (above the line) and contraction (below), Europe’s stalwarts were not immune to the trend: Germany fell to 52.0 and France declined to 50.5. July showed that four of the countries that reported measured below 50 (UK, Spain, Ireland, and Russia), with nine of the twelve countries reporting falling month-over-month, two expanding (Italy and Poland), and one flat (Turkey). In the case of Italy, July’s reading just got it over the 50 hump. With sticky stagflation in the UK, today’s data point gives us more conviction in our short EWU position. Suffice it to say, these PMI numbers don’t look good!

Levels on EUR-USD

As Keith mentioned this morning, the EUR/USD is the one strike price that should continue to whip around in the next 48 hours as we finally put the US debt ceiling debate to bed; watch $1.43 as your intermediate term TREND line that inflates/deflates everything else (across asset classes). The global market’s correlation risk moves off that. Our immediate term TRADE levels are $1.42 - $1.44.

European Financials CDS Monitor

Bank swaps in Europe were mostly wider last week. 36 of the 38 swaps were wider and 2 tightened, with Italian and Spanish spreads leading the charge higher.

Matthew Hedrick

Analyst